Anda mungkin juga menyukai

- Surrender Discharge Voucher of LIC Form No. 5074Dokumen5 halamanSurrender Discharge Voucher of LIC Form No. 5074Arindam Samanta100% (3)

- A Guide to Trade Credit InsuranceDari EverandA Guide to Trade Credit InsurancePenilaian: 4.5 dari 5 bintang4.5/5 (4)

- Snapdeal 170329070435Dokumen24 halamanSnapdeal 170329070435Sumon BeraBelum ada peringkat

- INSURANCE INNOVATION REFORMSDokumen63 halamanINSURANCE INNOVATION REFORMSShaheen ShaikhBelum ada peringkat

- Insurance in Bangladesh: A Growing IndustryDokumen17 halamanInsurance in Bangladesh: A Growing IndustryShuvro RahmanBelum ada peringkat

- Insurance - A Brief Overview: Chapter-1Dokumen58 halamanInsurance - A Brief Overview: Chapter-1Sreeja Sahadevan75% (4)

- Key Principle and Characteristics of Micro FinanceDokumen18 halamanKey Principle and Characteristics of Micro Financedeepakbrt85% (40)

- Accounting Prodigy BasicAcc1 Instructors Manual PDFDokumen5 halamanAccounting Prodigy BasicAcc1 Instructors Manual PDFPrecious Vercaza Del RosarioBelum ada peringkat

- Project Report FinalDokumen57 halamanProject Report FinalvytlaBelum ada peringkat

- Impact of Liberalisation of The Insurance Sector On The Life Insurance Corporation of IndiaDokumen10 halamanImpact of Liberalisation of The Insurance Sector On The Life Insurance Corporation of IndiaBrijbhushan ChavanBelum ada peringkat

- A Project ReportDokumen8 halamanA Project Reportmistryjinal546790% (10)

- Malhotra CommitteeDokumen5 halamanMalhotra CommitteeBibhash RoyBelum ada peringkat

- Aviva Life InsuranceDokumen85 halamanAviva Life InsuranceArpan SinghalBelum ada peringkat

- Summer Training Report-Max New York LifeDokumen40 halamanSummer Training Report-Max New York LifeAbhishek LaghateBelum ada peringkat

- Company ProfileDokumen90 halamanCompany ProfileJatan YagnikBelum ada peringkat

- Datta Sai AssisgnDokumen11 halamanDatta Sai Assisgnm_dattaiasBelum ada peringkat

- Managing insurance claims efficientlyDokumen69 halamanManaging insurance claims efficientlyAnand ChavanBelum ada peringkat

- Summer InternDokumen36 halamanSummer InternnehaBelum ada peringkat

- Sip PDFDokumen81 halamanSip PDF41APayoshni ChaudhariBelum ada peringkat

- Insurance Marketing in Indian EnvironmentDokumen6 halamanInsurance Marketing in Indian EnvironmentPurab MehtaBelum ada peringkat

- Claims Mangement in Life InsuranceDokumen68 halamanClaims Mangement in Life InsurancePraveen Rautela100% (1)

- HDFC Summer Training ProjectDokumen86 halamanHDFC Summer Training ProjectDeepak SinghalBelum ada peringkat

- Emerging InsuDokumen15 halamanEmerging InsuSneha JadhavBelum ada peringkat

- CHAPTER - 1 GENERAL INTRODUCTIONDokumen86 halamanCHAPTER - 1 GENERAL INTRODUCTIONVenkat GVBelum ada peringkat

- A Project Report OnDokumen54 halamanA Project Report OnMahesh ChennurBelum ada peringkat

- Indian insurance industry history and changing faceDokumen21 halamanIndian insurance industry history and changing facePradeep KumarBelum ada peringkat

- Financial Services: Jyothish P 4 SemesterDokumen57 halamanFinancial Services: Jyothish P 4 SemesterJyothish Punathil PBelum ada peringkat

- Swot AnalysisDokumen40 halamanSwot AnalysisMohmmedKhayyumBelum ada peringkat

- 1.1 Introduction of The Insurance Industry: First Life Insurance CompanyDokumen16 halaman1.1 Introduction of The Insurance Industry: First Life Insurance CompanyNANDUROCKSBelum ada peringkat

- History of Indian Insurance MarketDokumen10 halamanHistory of Indian Insurance MarketSneh MishraBelum ada peringkat

- Insurance Awareness in India MainDokumen39 halamanInsurance Awareness in India Maintejaskamble4575% (4)

- Tara Baap Ni GandDokumen60 halamanTara Baap Ni GandChiragPanchalBelum ada peringkat

- General Insurance Black Book ProjectDokumen45 halamanGeneral Insurance Black Book Projectprasad pawle50% (10)

- Symbiosis Institute of Management Studies: Submitted By: NAME: Shilpa Parmar Section: E Roll No: 49Dokumen7 halamanSymbiosis Institute of Management Studies: Submitted By: NAME: Shilpa Parmar Section: E Roll No: 49Shilpa ParmarBelum ada peringkat

- 1.1 General Introduction About The Sector: 1.2 Industry ProfileDokumen55 halaman1.1 General Introduction About The Sector: 1.2 Industry ProfileOmkar ChavanBelum ada peringkat

- Insurance Awareness in India MainDokumen34 halamanInsurance Awareness in India Maintejaskamble45Belum ada peringkat

- Liberalisation of Insurance Services RefinedDokumen22 halamanLiberalisation of Insurance Services RefinedJojin JoseBelum ada peringkat

- Project on Life Insurance CorporationDokumen34 halamanProject on Life Insurance CorporationVirendra JhaBelum ada peringkat

- Growth of Insurance IndustryDokumen5 halamanGrowth of Insurance IndustryGeetha RaniBelum ada peringkat

- Claims Management in Life InsuranceDokumen53 halamanClaims Management in Life InsuranceJitesh100% (3)

- Insurance SectorDokumen7 halamanInsurance Sectormamita1827Belum ada peringkat

- Review of LiteratureDokumen6 halamanReview of LiteraturePraveen SehgalBelum ada peringkat

- Bajaj Allianz Life InsuranceDokumen100 halamanBajaj Allianz Life InsuranceShiv GowdaBelum ada peringkat

- Should Insurer Compensate Loss from RiotsDokumen33 halamanShould Insurer Compensate Loss from RiotsKanchan GuptaBelum ada peringkat

- Role of Private Life Insurance Companies in IndiaDokumen19 halamanRole of Private Life Insurance Companies in IndiaRohit BundelaBelum ada peringkat

- Trends and developments in the Indian general insurance sectorDokumen26 halamanTrends and developments in the Indian general insurance sectorrajBelum ada peringkat

- Indian Insurance SectorDokumen32 halamanIndian Insurance Sectorbanirumi100% (2)

- Banking, Insurance Sector Guide for IndiaDokumen7 halamanBanking, Insurance Sector Guide for IndiaTSBelum ada peringkat

- Impact of Foreign Direct Investment in Life Insurance IndustryDokumen22 halamanImpact of Foreign Direct Investment in Life Insurance Industryvajaajay100% (1)

- Basics of InsuranceDokumen20 halamanBasics of InsuranceSunny RajBelum ada peringkat

- Insurance Claims Management ProcessDokumen7 halamanInsurance Claims Management ProcessJia GuptaBelum ada peringkat

- Accidental InsuranceDokumen33 halamanAccidental InsuranceHarinarayan PrajapatiBelum ada peringkat

- Executive SummaryDokumen44 halamanExecutive SummaryAvinash LoveBelum ada peringkat

- History and Development of Insurance in IndiaDokumen16 halamanHistory and Development of Insurance in IndiaAayush KaulBelum ada peringkat

- The SolutionDokumen7 halamanThe SolutionAnonymous y3E7iaBelum ada peringkat

- Re Insurance PaperDokumen10 halamanRe Insurance PaperkissishaBelum ada peringkat

- 1.1 Overview of The Insurance Industry 1.2 Profile of The Organization 1.3 Problems of HDFC SLICDokumen54 halaman1.1 Overview of The Insurance Industry 1.2 Profile of The Organization 1.3 Problems of HDFC SLICTejas GaubaBelum ada peringkat

- InsuranceDokumen19 halamanInsuranceVAR FINANCIAL SERVICESBelum ada peringkat

- 2 PDFDokumen11 halaman2 PDFAkshay PawarBelum ada peringkat

- Insurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5Dari EverandInsurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5Belum ada peringkat

- Development of Insurance in Angola: Case Study of a Key African Frontier Insurance MarketDari EverandDevelopment of Insurance in Angola: Case Study of a Key African Frontier Insurance MarketBelum ada peringkat

- Algo TradingDokumen4 halamanAlgo TradingKetan BariaBelum ada peringkat

- Rupee Depreciation - Probable Causes and OutlookDokumen10 halamanRupee Depreciation - Probable Causes and OutlookAshok ChakravarthyBelum ada peringkat

- Dekell, 2008Dokumen2 halamanDekell, 2008Nadirah KamilBelum ada peringkat

- Presentation 1Dokumen2 halamanPresentation 1Ketan BariaBelum ada peringkat

- Pay course fee at HBL by Mar 3Dokumen1 halamanPay course fee at HBL by Mar 3Abdul SalamBelum ada peringkat

- Service ContractsDokumen35 halamanService Contractsnsrinivas0850% (2)

- Master Circular on customer service guidelinesDokumen49 halamanMaster Circular on customer service guidelinesAnirudh SinghaBelum ada peringkat

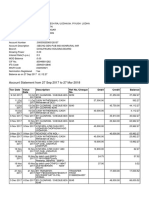

- Mr. Potlacheru Naveen Kumar bank account statementDokumen14 halamanMr. Potlacheru Naveen Kumar bank account statementP NAVEEN KUMARBelum ada peringkat

- Why Hayek Was Wrong On Concurrent CurrenciesDokumen12 halamanWhy Hayek Was Wrong On Concurrent CurrenciesKrzysiek RembiaszBelum ada peringkat

- 5 - (S2) Aa MP PDFDokumen3 halaman5 - (S2) Aa MP PDFFlow RiyaBelum ada peringkat

- Marie Curie Presentation Financial ReportingDokumen28 halamanMarie Curie Presentation Financial ReportingArmantoCepongBelum ada peringkat

- Fmutm Mock 05Dokumen8 halamanFmutm Mock 05api-2686327667% (3)

- Rich Text Editor FileDokumen5 halamanRich Text Editor FileA B M MoshiuddullahBelum ada peringkat

- Orden de Venta - 372 - 20181123 - 123904Dokumen2 halamanOrden de Venta - 372 - 20181123 - 123904l2oNnYBelum ada peringkat

- Costco Platinum Mastercard BenefitsDokumen15 halamanCostco Platinum Mastercard BenefitsJaskaran balBelum ada peringkat

- An Extraordinary Company-HDFCDokumen35 halamanAn Extraordinary Company-HDFCPrachi JainBelum ada peringkat

- Account statement details for Mr. Chandresh Raj LodhaDokumen3 halamanAccount statement details for Mr. Chandresh Raj LodhaHemlata LodhaBelum ada peringkat

- 634420393Dokumen3 halaman634420393Lucas De Paula CarneiroBelum ada peringkat

- Vidhyaashram First Grade College Corporate Accounting III II AssignmentDokumen4 halamanVidhyaashram First Grade College Corporate Accounting III II AssignmentveenaBelum ada peringkat

- 1990 2014 Merc Law Bar Exam Q and ADokumen260 halaman1990 2014 Merc Law Bar Exam Q and ADahlia Claudine May Perral0% (1)

- Vai Final Excel Cashbook With Links 2010Dokumen24 halamanVai Final Excel Cashbook With Links 2010sreekanthBelum ada peringkat

- When Does A Letter of Comfort Becomes A Contract of GuaranteeDokumen11 halamanWhen Does A Letter of Comfort Becomes A Contract of GuaranteeJ Imam100% (3)

- Dela Cruz Vs Capital Insurance & Surety CoDokumen1 halamanDela Cruz Vs Capital Insurance & Surety CoKelsey Olivar MendozaBelum ada peringkat

- Kode BankDokumen4 halamanKode BankMaha D NugrohoBelum ada peringkat

- SbiDokumen157 halamanSbijai2607Belum ada peringkat

- A Study On Customer Prefernces Towards Credit Cards in HDFC BankDokumen40 halamanA Study On Customer Prefernces Towards Credit Cards in HDFC BankSharathBelum ada peringkat

- Digital Adoption in The Insurance Sector: From Ambition To Reality?Dokumen12 halamanDigital Adoption in The Insurance Sector: From Ambition To Reality?Ivan GrgićBelum ada peringkat

- ToR Audit TenderDokumen9 halamanToR Audit TenderIslamicRelief AlbaniaBelum ada peringkat

- 310 Supreme Court Reports AnnotatedDokumen10 halaman310 Supreme Court Reports AnnotatedNinaBelum ada peringkat

- Gurvinder Brar - Text MiningDokumen28 halamanGurvinder Brar - Text Miningxy053333Belum ada peringkat