Anda mungkin juga menyukai

- Crossing of ChequesDokumen29 halamanCrossing of ChequesQurrat AneesBelum ada peringkat

- Crossing of ChequesDokumen14 halamanCrossing of ChequesRanvids100% (1)

- Cheques: Features of A ChequeDokumen12 halamanCheques: Features of A ChequebushrajaleelBelum ada peringkat

- Dishonour of ChequesDokumen17 halamanDishonour of Chequeschirag78775% (4)

- Cheque Paying and Collecting BankDokumen5 halamanCheque Paying and Collecting BankSyed RedwanBelum ada peringkat

- Presentation On Cheques: by Subrahmanya GSDokumen12 halamanPresentation On Cheques: by Subrahmanya GSChaitra GsBelum ada peringkat

- Banker Customer RelationshipDokumen7 halamanBanker Customer RelationshipPadmasree HarishBelum ada peringkat

- Banker Customer RelationshipDokumen7 halamanBanker Customer RelationshipJitendra VirahyasBelum ada peringkat

- Negotiable Instruments ActDokumen22 halamanNegotiable Instruments Actshivam007Belum ada peringkat

- Dishonour of NIDokumen36 halamanDishonour of NISugato C MukherjiBelum ada peringkat

- Bankruptcy ActDokumen15 halamanBankruptcy Actaparajita promaBelum ada peringkat

- Business and Environment Laws: Negotiable Instrument Act 1881 MBA Sem:3Dokumen41 halamanBusiness and Environment Laws: Negotiable Instrument Act 1881 MBA Sem:3UtsavBelum ada peringkat

- Consumer Credit CardsDokumen32 halamanConsumer Credit CardsMuhammad Mazhar YounusBelum ada peringkat

- The Declaration of Independence: A Play for Many ReadersDari EverandThe Declaration of Independence: A Play for Many ReadersBelum ada peringkat

- CHAPTER VII - Bank GuaranteesDokumen12 halamanCHAPTER VII - Bank Guaranteespriya guptaBelum ada peringkat

- Demand DraftDokumen5 halamanDemand DraftSmartKevalBelum ada peringkat

- Was Frankenstein Really Uncle Sam? Vol Ix: Notes on the State of the Declaration of IndependenceDari EverandWas Frankenstein Really Uncle Sam? Vol Ix: Notes on the State of the Declaration of IndependenceBelum ada peringkat

- Deposit and Borrowing OperationsDokumen5 halamanDeposit and Borrowing OperationsCinBelum ada peringkat

- Meaning of Banker and Customer Meaning of Banker and CustomerDokumen14 halamanMeaning of Banker and Customer Meaning of Banker and CustomerSaiful IslamBelum ada peringkat

- Bank Is An Agent, Trustee, Executor, Administrator For CustomersDokumen5 halamanBank Is An Agent, Trustee, Executor, Administrator For Customersgazi faisalBelum ada peringkat

- Negotiable InstrumentsDokumen22 halamanNegotiable InstrumentsPrince Mittal100% (1)

- International Settlement Letter of CreditDokumen80 halamanInternational Settlement Letter of CreditveroBelum ada peringkat

- Banking LawDokumen18 halamanBanking LawUdisha SinghBelum ada peringkat

- Banking Terms: SR - No. Terms Definition/MeaningDokumen6 halamanBanking Terms: SR - No. Terms Definition/Meaninghoney30389100% (1)

- Security and Advances PPT by SurbhiDokumen12 halamanSecurity and Advances PPT by SurbhiSV100% (1)

- Garnishee OrderDokumen3 halamanGarnishee OrderPrasad DurgeBelum ada peringkat

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDokumen3 halamanInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingS100% (2)

- Module 2 - Negotiable Instrument ActDokumen62 halamanModule 2 - Negotiable Instrument ActVK GamerBelum ada peringkat

- Banking Instruments: Indira Selvam. RDokumen10 halamanBanking Instruments: Indira Selvam. RSriramBelum ada peringkat

- Law and Practice of BankingDokumen106 halamanLaw and Practice of BankingArvind RaviBelum ada peringkat

- Collecting BankerDokumen15 halamanCollecting Bankeranusaya1988100% (2)

- Definition of The Maxim: Where There Is A Right There Is A RemedyDokumen2 halamanDefinition of The Maxim: Where There Is A Right There Is A RemedyAnonymous 3zoxlTjxvBelum ada peringkat

- Banker and CustomerDokumen23 halamanBanker and CustomerAnkan Pattanayak100% (1)

- Protecting Your Credit Score ActDokumen4 halamanProtecting Your Credit Score ActLashon SpearsBelum ada peringkat

- CHAPTER 5 Determination of Banker Customer ContractDokumen12 halamanCHAPTER 5 Determination of Banker Customer ContractCarl AbruquahBelum ada peringkat

- Letter of CreditDokumen3 halamanLetter of CreditRakesh_Kumar_A_8181Belum ada peringkat

- The Balance SheetDokumen7 halamanThe Balance Sheetsevirous valeriaBelum ada peringkat

- U.S. Bank Online Banking Terms and Conditions: Effective July 6, 2012Dokumen28 halamanU.S. Bank Online Banking Terms and Conditions: Effective July 6, 2012Monkees LabsBelum ada peringkat

- Knowledge Bank - Advances Against DepositsDokumen4 halamanKnowledge Bank - Advances Against DepositsKajeev KumarBelum ada peringkat

- Titles Webinar HandoutsDokumen26 halamanTitles Webinar HandoutsbigwupBelum ada peringkat

- Types of Cheque PDFDokumen5 halamanTypes of Cheque PDFRicha Nandy0% (1)

- Mortage PDFDokumen83 halamanMortage PDFnilofer shallyBelum ada peringkat

- Right of Lien by BankersDokumen13 halamanRight of Lien by Bankersgeegostral chhabraBelum ada peringkat

- Privacy ActDokumen62 halamanPrivacy ActMarkMemmottBelum ada peringkat

- The Banker-Customer RelationshipDokumen31 halamanThe Banker-Customer RelationshipStefan Adrian VanceaBelum ada peringkat

- Banker Customer RelationshipDokumen45 halamanBanker Customer RelationshipRajat SharmaBelum ada peringkat

- The Missing Assignment DilemmaDokumen5 halamanThe Missing Assignment Dilemmarhouse_1100% (1)

- Marking of ChecksDokumen11 halamanMarking of ChecksPavel LahaBelum ada peringkat

- Bankers' ObligationsDokumen9 halamanBankers' ObligationsAnmoldeep DhillonBelum ada peringkat

- CLearing HouseDokumen23 halamanCLearing HouseNitin KapoorBelum ada peringkat

- Commercial BanksDokumen5 halamanCommercial BankssnehaBelum ada peringkat

- Banking Awareness ImportantDokumen30 halamanBanking Awareness ImportantThirrunavukkarasu R RBelum ada peringkat

- Relationship of Debtor and CreditorDokumen15 halamanRelationship of Debtor and CreditorAndualem GetuBelum ada peringkat

- My Banking Law NotesDokumen14 halamanMy Banking Law NotesarmsarivuBelum ada peringkat

- Law 307 - Topic 2D - Subrogation and ContributionDokumen20 halamanLaw 307 - Topic 2D - Subrogation and ContributionMoshiul TanjilBelum ada peringkat

- Explanation.-For The Purposes of The Sub-Clause (I), "Commercial Purpose" Does Not Include UseDokumen21 halamanExplanation.-For The Purposes of The Sub-Clause (I), "Commercial Purpose" Does Not Include UsePrajwal KottawarBelum ada peringkat

- Banker Customer RelationshipDokumen7 halamanBanker Customer RelationshipJitendra VirahyasBelum ada peringkat

- Persons of Indian OriginDokumen2 halamanPersons of Indian OriginJitendra VirahyasBelum ada peringkat

- Who Is A BankerDokumen1 halamanWho Is A BankerJitendra VirahyasBelum ada peringkat

- Banking System in IndiaDokumen4 halamanBanking System in IndiaJitendra VirahyasBelum ada peringkat

- History of BankingDokumen2 halamanHistory of BankingJitendra VirahyasBelum ada peringkat

- 0303 Micr ChequeDokumen1 halaman0303 Micr ChequeJitendra VirahyasBelum ada peringkat

- Certificates of DepositDokumen3 halamanCertificates of DepositJitendra VirahyasBelum ada peringkat

- 0306 Collection of ChequesDokumen17 halaman0306 Collection of ChequesJitendra Virahyas100% (1)

- Account OpeningDokumen3 halamanAccount OpeningJitendra VirahyasBelum ada peringkat

- History's Greatest Financial FallDokumen8 halamanHistory's Greatest Financial FallJitendra VirahyasBelum ada peringkat

- Customer AccountsDokumen32 halamanCustomer AccountsJitendra VirahyasBelum ada peringkat

- Annexure To KycDokumen5 halamanAnnexure To KycJitendra VirahyasBelum ada peringkat

- Pepsico Performance Appraisal and Induction PolicyDokumen114 halamanPepsico Performance Appraisal and Induction PolicyJitendra Virahyas100% (5)

- J.K.cemeNT LTD Manufacturing Process and Financial ActivitiesDokumen102 halamanJ.K.cemeNT LTD Manufacturing Process and Financial ActivitiesJitendra VirahyasBelum ada peringkat

- Motilal Oswal Securities Limited Analysis of Derivative and Stock MarketDokumen104 halamanMotilal Oswal Securities Limited Analysis of Derivative and Stock MarketJitendra Virahyas100% (3)

- Birla Corporation Limited Promotional SchemeDokumen101 halamanBirla Corporation Limited Promotional SchemeJitendra VirahyasBelum ada peringkat

- PEPSICO Selection and Salary Wages PolicyDokumen129 halamanPEPSICO Selection and Salary Wages PolicyJitendra Virahyas67% (3)

- Saras Recruitment ProcedureDokumen99 halamanSaras Recruitment ProcedureJitendra Virahyas0% (1)

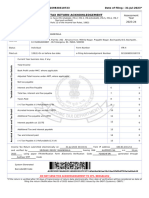

- Fee Circular 2023 24Dokumen1 halamanFee Circular 2023 24Archana SinghBelum ada peringkat

- Account Summary Payment Information: New Balance: $261.55Dokumen6 halamanAccount Summary Payment Information: New Balance: $261.55AriadnaUrsachi100% (2)

- Transfer PricingDokumen98 halamanTransfer PricingMAHESH JAINBelum ada peringkat

- Isla Lipana & Co., ITAD BIR Ruling No. 041-21 Dated September 29, 2021Dokumen8 halamanIsla Lipana & Co., ITAD BIR Ruling No. 041-21 Dated September 29, 2021Carlota VillaromanBelum ada peringkat

- BoB MITC A4 Booklet Ver-6.0 01AUG23Dokumen4 halamanBoB MITC A4 Booklet Ver-6.0 01AUG23rjlover24Belum ada peringkat

- No Name T1 2022Dokumen42 halamanNo Name T1 2022Indo -CanadianBelum ada peringkat

- Payroll Accounting PowerpointDokumen13 halamanPayroll Accounting PowerpointMr. CrustBelum ada peringkat

- Centrifuge Machine - InvoiceDokumen1 halamanCentrifuge Machine - InvoiceArindam HaldarBelum ada peringkat

- SAP FI NotesDokumen2 halamanSAP FI NotesvinodnagarajuBelum ada peringkat

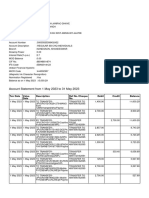

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen10 halamanAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Belum ada peringkat

- Atm QuestionnaireDokumen3 halamanAtm Questionnaireyuvashankar100% (3)

- Daily Sales Recapitulation Report - 20230518093914Dokumen6 halamanDaily Sales Recapitulation Report - 20230518093914muhammad imamBelum ada peringkat

- Module2 AE26 ITDokumen7 halamanModule2 AE26 ITJemalyn PiliBelum ada peringkat

- Taxation - Ins 3010: Group 2Dokumen10 halamanTaxation - Ins 3010: Group 2nguyễnthùy dươngBelum ada peringkat

- STFCS 2022-11-05 1667702284229Dokumen7 halamanSTFCS 2022-11-05 1667702284229Charles GoodwinBelum ada peringkat

- Account Statement: Msatools N No 12 O No 18 Sowrastra Nagar 1St Street Choolaimedu Ambattur ChennaiDokumen2 halamanAccount Statement: Msatools N No 12 O No 18 Sowrastra Nagar 1St Street Choolaimedu Ambattur ChennaiChandru ChristurajBelum ada peringkat

- Tax Management SyllabusDokumen2 halamanTax Management Syllabusbs_sharathBelum ada peringkat

- Solutions To Chapter 13 Problems 1Dokumen3 halamanSolutions To Chapter 13 Problems 1Hira ParachaBelum ada peringkat

- Income Tax - Sridhar Reddy MannemalaDokumen34 halamanIncome Tax - Sridhar Reddy MannemalaSrilakshmi MBelum ada peringkat

- Azure InvoiceDokumen2 halamanAzure InvoiceAnkit SambhareBelum ada peringkat

- Manila Mandarin Hotels Vs CommissionerDokumen2 halamanManila Mandarin Hotels Vs CommissionerEryl Yu100% (1)

- GST Compensation CessDokumen2 halamanGST Compensation CessPalak JioBelum ada peringkat

- Taxguru - in-TaxGuru Consultancy Amp Online Publication LLPDokumen7 halamanTaxguru - in-TaxGuru Consultancy Amp Online Publication LLPsamratsom1947Belum ada peringkat

- P1 1.3CashBasisAccrualBasisSingleEntryZETADokumen3 halamanP1 1.3CashBasisAccrualBasisSingleEntryZETASophia AprilBelum ada peringkat

- Invoice - 1Dokumen1 halamanInvoice - 1Toney KurianBelum ada peringkat

- Sales Quotation: Jl. Nias 3 No. 33 Lingk. Tegalboto Kidul, Kel. Sumbersari, Kec. Sumbersari Kab. Jember, Jawa TimurDokumen1 halamanSales Quotation: Jl. Nias 3 No. 33 Lingk. Tegalboto Kidul, Kel. Sumbersari, Kec. Sumbersari Kab. Jember, Jawa TimurAde HerdiansyahBelum ada peringkat

- Article 1 - Taxation and Its Negative Impact On Business Investment ActivitiesDokumen6 halamanArticle 1 - Taxation and Its Negative Impact On Business Investment ActivitiesceistBelum ada peringkat

- Forwarding Data DictionaryDokumen214 halamanForwarding Data DictionaryRohit JainBelum ada peringkat

- User Id 012439461813 - DSL Telephonenumber 01244823150Dokumen6 halamanUser Id 012439461813 - DSL Telephonenumber 01244823150NAVEEN SLBelum ada peringkat

- Income Tax StatementDokumen2 halamanIncome Tax StatementgdBelum ada peringkat