Anda mungkin juga menyukai

- Forecasting Mainstream School Funding: School Financial Success Guides, #5Dari EverandForecasting Mainstream School Funding: School Financial Success Guides, #5Belum ada peringkat

- TRC News and Notes 3-15-12Dokumen2 halamanTRC News and Notes 3-15-12James Van BruggenBelum ada peringkat

- EdSource: Proposition 30 - Proposition 38 ComparisonsDokumen8 halamanEdSource: Proposition 30 - Proposition 38 Comparisonsk12newsnetworkBelum ada peringkat

- CCPA - Eliminating Tuition and Compulsory Fees For Post-Secondary EducationDokumen7 halamanCCPA - Eliminating Tuition and Compulsory Fees For Post-Secondary EducationRBeaudryCCLEBelum ada peringkat

- K-12 Education SpendingDokumen38 halamanK-12 Education SpendingBrooke ValentineBelum ada peringkat

- Top 10 Reasons For MA To Invest in Public Higher EDDokumen11 halamanTop 10 Reasons For MA To Invest in Public Higher EDMatt VachonBelum ada peringkat

- Top 10 Higher Education State Policy Issues For 2012: American Association of State Colleges and UniversitiesDokumen6 halamanTop 10 Higher Education State Policy Issues For 2012: American Association of State Colleges and Universitiesapi-143403667Belum ada peringkat

- 2015 - The Year of Pension Reckoning? (January 2015)Dokumen2 halaman2015 - The Year of Pension Reckoning? (January 2015)Jim PawelczykBelum ada peringkat

- Issues and Answers: 2016 Session of The General AssemblyDokumen4 halamanIssues and Answers: 2016 Session of The General Assemblyapi-320886833Belum ada peringkat

- TTR Illinoisfunding SchwartzcordesDokumen12 halamanTTR Illinoisfunding SchwartzcordesNational Education Policy CenterBelum ada peringkat

- Education Issues Brief 2010-2011Dokumen30 halamanEducation Issues Brief 2010-2011Valori OliverBelum ada peringkat

- Scale," See Table From LAO Jan 27, 12 Report Notes Possible Discrepancy Between PDFDokumen4 halamanScale," See Table From LAO Jan 27, 12 Report Notes Possible Discrepancy Between PDFk12newsnetworkBelum ada peringkat

- Blog Budget PresentationDokumen22 halamanBlog Budget Presentationapi-282246902Belum ada peringkat

- Policy Report: South Carolina Policy CouncilDokumen9 halamanPolicy Report: South Carolina Policy CouncilSteve CouncilBelum ada peringkat

- Position Paper On School Finance Reform in Michigan Revised June 2015Dokumen9 halamanPosition Paper On School Finance Reform in Michigan Revised June 2015api-241862212Belum ada peringkat

- Financing Public EducationDokumen11 halamanFinancing Public EducationSan Eustacio Elementary SchoolBelum ada peringkat

- Where Is All The Money Going - An Analysis of Inside and Outside The Classroom Education SpendingDokumen6 halamanWhere Is All The Money Going - An Analysis of Inside and Outside The Classroom Education Spendingthe kingfishBelum ada peringkat

- State Budget Cuts To Education Hurt Kentucky's Classrooms and KidsDokumen28 halamanState Budget Cuts To Education Hurt Kentucky's Classrooms and KidsBecca SchimmelBelum ada peringkat

- UpInTheAir BudgetBrief-1Dokumen28 halamanUpInTheAir BudgetBrief-1Aly ProutyBelum ada peringkat

- How Much Ivory Does This Tower Need? What We Spend On, and Get From, Higher Education, Cato Policy Analysis No. 686Dokumen24 halamanHow Much Ivory Does This Tower Need? What We Spend On, and Get From, Higher Education, Cato Policy Analysis No. 686Cato InstituteBelum ada peringkat

- Unit 6 PaperDokumen7 halamanUnit 6 Paperapi-310891073Belum ada peringkat

- Final Assignment - Part 1 J VilorioDokumen7 halamanFinal Assignment - Part 1 J Vilorioapi-245709325Belum ada peringkat

- The Truth About Education FundingDokumen2 halamanThe Truth About Education FundingKim SchmidtnerBelum ada peringkat

- 11.20.2013 AQE 2014 Legislative Priorites EmbargoedDokumen6 halaman11.20.2013 AQE 2014 Legislative Priorites EmbargoedJon CampbellBelum ada peringkat

- 2022-24 Executive Budget Executive Summary EducationDokumen6 halaman2022-24 Executive Budget Executive Summary EducationShannon StowersBelum ada peringkat

- Innovative Options For Parents of Children in The Lowest Performing SchoolsDokumen7 halamanInnovative Options For Parents of Children in The Lowest Performing SchoolsCREWBelum ada peringkat

- Financing Educational SystemsDokumen2 halamanFinancing Educational SystemsRochelle EstebanBelum ada peringkat

- Equitable Funding For School Infrastructure Projects Shruti Lakshmanan Harshita Jalluri Eshaan Kawlra and Una JakupovicDokumen5 halamanEquitable Funding For School Infrastructure Projects Shruti Lakshmanan Harshita Jalluri Eshaan Kawlra and Una Jakupovicapi-523746438Belum ada peringkat

- Rendell Tax Justification Memo 072409Dokumen3 halamanRendell Tax Justification Memo 072409jmicek100% (2)

- Benefits of Budget CuttingDokumen19 halamanBenefits of Budget CuttinghaslinaBelum ada peringkat

- Anthony Brown 2013 MSEA Survey ResponsesDokumen29 halamanAnthony Brown 2013 MSEA Survey ResponsesDavid MoonBelum ada peringkat

- Why Students Should Oppose Tuition Hikes and Ask For Free EducationDokumen4 halamanWhy Students Should Oppose Tuition Hikes and Ask For Free EducationsylogluBelum ada peringkat

- Donating The Voucher: An Alternative Tax Treatment of Private School EnrollmentDokumen2 halamanDonating The Voucher: An Alternative Tax Treatment of Private School EnrollmentCato InstituteBelum ada peringkat

- Educ 612 Case Digest On Budgeting and DisbursementDokumen10 halamanEduc 612 Case Digest On Budgeting and DisbursementCristobal RabuyaBelum ada peringkat

- Olicy Eport: School Finance and The 2019-20 Executive BudgetDokumen8 halamanOlicy Eport: School Finance and The 2019-20 Executive BudgetThe Capitol PressroomBelum ada peringkat

- NJ DYFS DCF Response To Office of Legislative Services Budget Q&A FY 2011-12Dokumen11 halamanNJ DYFS DCF Response To Office of Legislative Services Budget Q&A FY 2011-12Rick ThomaBelum ada peringkat

- Fiscal Analysis of A $500 Federal Education Tax Credit To Help Millions, Save Billions, Cato Policy Analysis No. 398Dokumen16 halamanFiscal Analysis of A $500 Federal Education Tax Credit To Help Millions, Save Billions, Cato Policy Analysis No. 398Cato InstituteBelum ada peringkat

- U.S. Public Schools Experience More Competition For FundingDokumen6 halamanU.S. Public Schools Experience More Competition For Fundingapi-227433089Belum ada peringkat

- 2016 Finance Survey Report FINALDokumen24 halaman2016 Finance Survey Report FINALrkarlinBelum ada peringkat

- Child Care FactsDokumen29 halamanChild Care FactsBri WhiteBelum ada peringkat

- Assessments Standards by Lonnie Tucker, CHE, CSW & Ms. Donna Wells, BS, PCWSDokumen38 halamanAssessments Standards by Lonnie Tucker, CHE, CSW & Ms. Donna Wells, BS, PCWSLakotaAdvocatesBelum ada peringkat

- Superintendent Hicks: Letter To Governor CuomoDokumen2 halamanSuperintendent Hicks: Letter To Governor CuomoAlan BedenkoBelum ada peringkat

- We Are One Illinois Studies and SummaryDokumen30 halamanWe Are One Illinois Studies and SummaryWeAreOneILBelum ada peringkat

- 2017 Ohio AAUP Higher Education ReportDokumen22 halaman2017 Ohio AAUP Higher Education ReportCincinnatiEnquirerBelum ada peringkat

- School Funding Gap EssayDokumen14 halamanSchool Funding Gap Essayapi-466376923Belum ada peringkat

- Expanded Eitc SummaryDokumen1 halamanExpanded Eitc SummaryjmicekBelum ada peringkat

- Description: Tags: IntroductionDokumen10 halamanDescription: Tags: Introductionanon-764178Belum ada peringkat

- Proposal A PaperDokumen10 halamanProposal A Paperapi-410748670Belum ada peringkat

- Description: Tags: ProposalDokumen31 halamanDescription: Tags: Proposalanon-694361Belum ada peringkat

- The Future of Education (Jan 2011) PaperDokumen5 halamanThe Future of Education (Jan 2011) PaperjuliepwrightBelum ada peringkat

- Financing Schools: Analysis and RecommendationsDokumen20 halamanFinancing Schools: Analysis and RecommendationsAmjad IbrahimBelum ada peringkat

- 1927 Laura Freeman Policy Brief 402583 17131388Dokumen2 halaman1927 Laura Freeman Policy Brief 402583 17131388api-309957654Belum ada peringkat

- Texto Fuente para El Examen Final Returning EducationDokumen2 halamanTexto Fuente para El Examen Final Returning EducationManuela Di PaoloBelum ada peringkat

- No Child Left Behind PolicyDokumen19 halamanNo Child Left Behind PolicyDeuterBelum ada peringkat

- Position Paper HB4277Dokumen4 halamanPosition Paper HB4277Valerie F. LeonardBelum ada peringkat

- Pros and Cons of Budgets CutDokumen10 halamanPros and Cons of Budgets Cutclaroscuro17Belum ada peringkat

- The Hidden Bill: Chicago Taxpayers and The Looming CrisisDokumen32 halamanThe Hidden Bill: Chicago Taxpayers and The Looming CrisisIllinois Policy100% (1)

- An Open Letter To The General Assembly On The Progressive Income Tax From Illinois Local GovernmentsDokumen2 halamanAn Open Letter To The General Assembly On The Progressive Income Tax From Illinois Local GovernmentsIllinois PolicyBelum ada peringkat

- Annual Cost of Illinois LawmakersDokumen24 halamanAnnual Cost of Illinois LawmakersIllinois PolicyBelum ada peringkat

- Amendment of Chapter 4-64 of Municipal Code by Adding New Section 4-64-098 Regarding Flavored Tobacco Products and Amending Section 4-64-180Dokumen7 halamanAmendment of Chapter 4-64 of Municipal Code by Adding New Section 4-64-098 Regarding Flavored Tobacco Products and Amending Section 4-64-180Illinois PolicyBelum ada peringkat

- Illinois Senate Bill 1Dokumen482 halamanIllinois Senate Bill 1Illinois PolicyBelum ada peringkat

- Compass (Summer 2013) Power of School ChoiceDokumen28 halamanCompass (Summer 2013) Power of School ChoiceIllinois PolicyBelum ada peringkat

- Ready For The Snow? Gauging Illinois's Performance On A Critical Core ServiceinalDokumen5 halamanReady For The Snow? Gauging Illinois's Performance On A Critical Core ServiceinalIllinois PolicyBelum ada peringkat

- ForthePeopleFinal-2Getting Less For More: A Report Card On Illinois State Higher EducationDokumen66 halamanForthePeopleFinal-2Getting Less For More: A Report Card On Illinois State Higher EducationIllinois PolicyBelum ada peringkat

- Letter From Sen. Richard DurbinDokumen2 halamanLetter From Sen. Richard DurbinIllinois PolicyBelum ada peringkat

- John Tillman's Response To U.S. Sen. Richard DurbinDokumen1 halamanJohn Tillman's Response To U.S. Sen. Richard DurbinIllinois PolicyBelum ada peringkat

- Madigan Letter To Michael Carrigan Regarding Union Pension SummitDokumen2 halamanMadigan Letter To Michael Carrigan Regarding Union Pension SummitIllinois PolicyBelum ada peringkat

- Contracting For Success: An Introduction To School Service PrivatizationDokumen81 halamanContracting For Success: An Introduction To School Service PrivatizationIllinois PolicyBelum ada peringkat

- Obstructed Views: Illinois' 102 County Online Transparency AuditDokumen21 halamanObstructed Views: Illinois' 102 County Online Transparency AuditIllinois Policy100% (1)

- Budget Solutions 2014: Pension Reform and Responsible Spending For State and Local GovernmentsDokumen29 halamanBudget Solutions 2014: Pension Reform and Responsible Spending For State and Local GovernmentsIllinois PolicyBelum ada peringkat

- The Pension Funding Guarantee: An Irresponsible PlanDokumen4 halamanThe Pension Funding Guarantee: An Irresponsible PlanIllinois PolicyBelum ada peringkat

- The Cost Shift: Why School Districts Would Benefit From A 401 (K) - Style Retirement PlanDokumen24 halamanThe Cost Shift: Why School Districts Would Benefit From A 401 (K) - Style Retirement PlanIllinois PolicyBelum ada peringkat

- Fiscal NotesDokumen9 halamanFiscal NotesIllinois PolicyBelum ada peringkat

- HB 3411 Makes Illinois' Already-Broken Pension System WorseDokumen1 halamanHB 3411 Makes Illinois' Already-Broken Pension System WorseIllinois PolicyBelum ada peringkat

- Compass (Spring 2013) Betting On IllinoisDokumen28 halamanCompass (Spring 2013) Betting On IllinoisIllinois PolicyBelum ada peringkat

- AFSCME February Bargaining BulletinDokumen2 halamanAFSCME February Bargaining BulletinIllinois PolicyBelum ada peringkat

- AFSCME Strike MemoDokumen2 halamanAFSCME Strike MemoIllinois PolicyBelum ada peringkat

- Gov. Quinn State of The State Address 2013Dokumen13 halamanGov. Quinn State of The State Address 2013Illinois PolicyBelum ada peringkat

- Lessons From The Edgar Plan: Why Defined Benefits Can't WorkDokumen7 halamanLessons From The Edgar Plan: Why Defined Benefits Can't WorkIllinois PolicyBelum ada peringkat

- Medicaid SolutionsDokumen14 halamanMedicaid SolutionsIllinois PolicyBelum ada peringkat

- Illinois Is A High-Tax StateDokumen6 halamanIllinois Is A High-Tax StateIllinois PolicyBelum ada peringkat

- Compass (WINTER 2012) Illinois Labor Law Created Union MonsterDokumen28 halamanCompass (WINTER 2012) Illinois Labor Law Created Union MonsterIllinois PolicyBelum ada peringkat

- 2012 Illinois Piglet DigitalDokumen37 halaman2012 Illinois Piglet DigitalIllinois PolicyBelum ada peringkat

- Policy Point: Illinois' High-Tax ProblemDokumen1 halamanPolicy Point: Illinois' High-Tax ProblemIllinois PolicyBelum ada peringkat

- Key States On The Front Line of Stopping ObamaCareDokumen5 halamanKey States On The Front Line of Stopping ObamaCareIllinois PolicyBelum ada peringkat

- The Financial Sector in Papua New Guinea - A Good Case of ReformDokumen22 halamanThe Financial Sector in Papua New Guinea - A Good Case of ReformZebedee TaltalBelum ada peringkat

- Roots Millennium Schools Salary Slip For The Month of September 2019Dokumen1 halamanRoots Millennium Schools Salary Slip For The Month of September 2019Samia AroojBelum ada peringkat

- Guidance On Fees and Day Rates For Visual Artists 2017Dokumen2 halamanGuidance On Fees and Day Rates For Visual Artists 2017Ruth ElliotBelum ada peringkat

- United States v. Davis, 397 U.S. 301 (1970)Dokumen10 halamanUnited States v. Davis, 397 U.S. 301 (1970)Scribd Government DocsBelum ada peringkat

- Statutory Liquidity Ratio (SLR) : What Is SLR? Approved Securities by Rbi For SLR Objective For Maintaining SLRDokumen3 halamanStatutory Liquidity Ratio (SLR) : What Is SLR? Approved Securities by Rbi For SLR Objective For Maintaining SLRDhaval224Belum ada peringkat

- Hoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89Dokumen72 halamanHoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89E Frank CorneliusBelum ada peringkat

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap015 PDFDokumen54 halamanSolution Manual Advanced Financial Accounting 8th Edition Baker Chap015 PDFYopie ChandraBelum ada peringkat

- 1 - Priority - Sector - LendingDokumen24 halaman1 - Priority - Sector - LendingMantu Kumar100% (1)

- Partnership LiquidationDokumen11 halamanPartnership LiquidationBimboy Romano100% (1)

- Nursing Home ComplaintDokumen55 halamanNursing Home ComplaintLaura NahmiasBelum ada peringkat

- FNCE 623 Formulae For Mid Term ExamDokumen3 halamanFNCE 623 Formulae For Mid Term Examleili fallahBelum ada peringkat

- Gale Force SurfingDokumen18 halamanGale Force SurfingKhris Keleher50% (4)

- GST/HST New Housing Rebate Application For Houses Purchased From A BuilderDokumen4 halamanGST/HST New Housing Rebate Application For Houses Purchased From A BuilderEffel PradoBelum ada peringkat

- Chap 006Dokumen51 halamanChap 006kel458100% (1)

- Debt Instruments Bank LoansDokumen42 halamanDebt Instruments Bank Loansprakhar singh100% (4)

- Tax Rebate Calculator of Salaried Class Indviduals 2013-14Dokumen4 halamanTax Rebate Calculator of Salaried Class Indviduals 2013-14waheedBelum ada peringkat

- The Theory of Interest (Stephen G. Kellison)Dokumen167 halamanThe Theory of Interest (Stephen G. Kellison)Farhan89% (62)

- Temporal Rate Method Balance Sheet AssetsDokumen3 halamanTemporal Rate Method Balance Sheet Assetslinda daibesBelum ada peringkat

- Accounting Assumptions: Introduction To Basic AccountingDokumen6 halamanAccounting Assumptions: Introduction To Basic AccountingJon Nell Laguador Bernardo100% (1)

- Topic OneDokumen43 halamanTopic OneMerediths KrisKringleBelum ada peringkat

- Theory - Part 2 PDFDokumen21 halamanTheory - Part 2 PDFBettina OsterfasticsBelum ada peringkat

- Adoracion Paguyo VS. Charlie Gatbunton 523 SCRA 156 FactsDokumen2 halamanAdoracion Paguyo VS. Charlie Gatbunton 523 SCRA 156 Factsps johnBelum ada peringkat

- SYAT Bookkeeping TutorialDokumen35 halamanSYAT Bookkeeping TutorialJanelle MendozaBelum ada peringkat

- Cost of Captial MCQDokumen5 halamanCost of Captial MCQAbhishek Sinha50% (4)

- Subway Bankrupcy 1Dokumen34 halamanSubway Bankrupcy 1Kate TaylorBelum ada peringkat

- Budget Planner - Overview / Help: InstructionsDokumen7 halamanBudget Planner - Overview / Help: InstructionsDarwin Dionisio ClementeBelum ada peringkat

- Beginning CosmeticDokumen3 halamanBeginning CosmeticPloy Sayamol20% (5)

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 646328380190719 Assessment Year: 2019-20Dokumen6 halamanItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 646328380190719 Assessment Year: 2019-20Mukesh kumar DewraBelum ada peringkat

- Press Note 3 - FDIDokumen2 halamanPress Note 3 - FDIjimit0810Belum ada peringkat

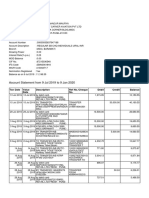

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen4 halamanAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeBelum ada peringkat