Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Genco Shipping & Trading Limited: Q2 2013 Earnings Call August 1, 2013Dokumen25 halamanGenco Shipping & Trading Limited: Q2 2013 Earnings Call August 1, 2013Arizar777Belum ada peringkat

- Best Practices vs. Misuse of PCA in The Analysis of Climate VariabilityDokumen25 halamanBest Practices vs. Misuse of PCA in The Analysis of Climate VariabilityArizar777Belum ada peringkat

- (Ebook) - The Mathematics of Financial Derivatives (Wilmott, Howison, Dewynne - Cambridge, SDokumen338 halaman(Ebook) - The Mathematics of Financial Derivatives (Wilmott, Howison, Dewynne - Cambridge, SArizar777Belum ada peringkat

- GARCH Parameter Estimation Using High-Frequency DataDokumen31 halamanGARCH Parameter Estimation Using High-Frequency DataArizar777Belum ada peringkat

- 2 - Trading Guides - OptionsCourse-301 - Volatility - TradingDokumen96 halaman2 - Trading Guides - OptionsCourse-301 - Volatility - TradingArizar777100% (1)

- An Analysis of Onion Options and Double-no-Touch Digitals: Stefan Ebenfeld, Matthias R. Mayr and Ju Rgen TopperDokumen10 halamanAn Analysis of Onion Options and Double-no-Touch Digitals: Stefan Ebenfeld, Matthias R. Mayr and Ju Rgen TopperArizar777Belum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

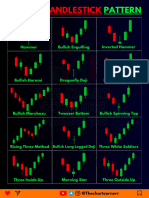

- Can Price Anomalies Been Obtained by Using Candlestick Patterns?Dokumen27 halamanCan Price Anomalies Been Obtained by Using Candlestick Patterns?Adnan WasimBelum ada peringkat

- Facility LocationDokumen30 halamanFacility Locationtush_chiefBelum ada peringkat

- Chart Pattern Cheat Sheet-1Dokumen18 halamanChart Pattern Cheat Sheet-1YASHANK VISHWAKARMABelum ada peringkat

- Pricing-Good NightDokumen17 halamanPricing-Good NightSanjeev ThadaniBelum ada peringkat

- Acc 309Dokumen5 halamanAcc 309Ampy SasutonaBelum ada peringkat

- Managerial Economics - Chapter 3-Empirical Methods For Demand Analysis Session 2Dokumen44 halamanManagerial Economics - Chapter 3-Empirical Methods For Demand Analysis Session 2Aabraham Samraj PonmaniBelum ada peringkat

- Idea Submission TemplateDokumen9 halamanIdea Submission TemplateDarkartsBelum ada peringkat

- SEBI Portfolio - Feb 2020Dokumen347 halamanSEBI Portfolio - Feb 2020Tapan LahaBelum ada peringkat

- Long-Run Cost: The Production FunctionDokumen11 halamanLong-Run Cost: The Production FunctionPUBG LOVERSBelum ada peringkat

- Ap-5901 SheDokumen7 halamanAp-5901 SheLizette Oliva80% (5)

- Advertising Proposal: Ad Agency XYZDokumen13 halamanAdvertising Proposal: Ad Agency XYZanneBelum ada peringkat

- Customer Delivery - Stock in Transit (EHP5 - LOG - MM - SIT Functionality)Dokumen43 halamanCustomer Delivery - Stock in Transit (EHP5 - LOG - MM - SIT Functionality)Dmitry Popov100% (1)

- FinMan Unit 5 Lecture-Bond Valuation-2021 S1Dokumen42 halamanFinMan Unit 5 Lecture-Bond Valuation-2021 S1Debbie DebzBelum ada peringkat

- Kardex - Job Description - Territory Sales SouthDokumen2 halamanKardex - Job Description - Territory Sales SouthMayank RawatBelum ada peringkat

- Interest Rate Hedging-Examples: Arshad HassanDokumen32 halamanInterest Rate Hedging-Examples: Arshad HassanirfanhaidersewagBelum ada peringkat

- Applied Economics Final ExamDokumen3 halamanApplied Economics Final ExamDaisy Orbon67% (3)

- 2000 Economics (AL) Paper 1 ADokumen9 halaman2000 Economics (AL) Paper 1 ABen ChanBelum ada peringkat

- Competing On ResourcesDokumen3 halamanCompeting On ResourcesrajeshwariBelum ada peringkat

- Public Procurement & Bid Rigging - An IntroductionDokumen15 halamanPublic Procurement & Bid Rigging - An IntroductionIndianAntitrustBelum ada peringkat

- A Project Study Report "A Study On Customer Awareness and Perception About Roadside Assistance" OFDokumen51 halamanA Project Study Report "A Study On Customer Awareness and Perception About Roadside Assistance" OFAnkur mittalBelum ada peringkat

- L Oreal Global Brand, Local Knowledge.Dokumen22 halamanL Oreal Global Brand, Local Knowledge.arbabBelum ada peringkat

- Theo Chocolate Case Study AnalysisDokumen21 halamanTheo Chocolate Case Study AnalysisRahisya MentariBelum ada peringkat

- A Price Action Traders Guide To Supply and DemandDokumen17 halamanA Price Action Traders Guide To Supply and Demandmohamed100% (2)

- NirmaDokumen18 halamanNirmaAnisa_RaoBelum ada peringkat

- This Study Resource Was: Accounting For BondsDokumen4 halamanThis Study Resource Was: Accounting For BondsSeunghyun ParkBelum ada peringkat

- Planet MicroCap Review Q3 2022Dokumen120 halamanPlanet MicroCap Review Q3 2022Planet MicroCap Review MagazineBelum ada peringkat

- NBP Nafa Funds PDFDokumen23 halamanNBP Nafa Funds PDFHamid AliBelum ada peringkat

- Xerox Equipment HandbookDokumen586 halamanXerox Equipment HandbookdarwinabadBelum ada peringkat

- 1576847379CDM - Introduction To Digital Marketing Module 1 - Sessions 2Dokumen84 halaman1576847379CDM - Introduction To Digital Marketing Module 1 - Sessions 2withanage gayashaniBelum ada peringkat

- FORM Presentation Nov 13thDokumen10 halamanFORM Presentation Nov 13thMohamad WafiyBelum ada peringkat