Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Benefits AccountingDokumen4 halamanBenefits AccountingJulian Christopher Torcuator50% (2)

- Human Resource Management Practices at The National Thermal Power Corporation (NTPC) in IndiaDokumen34 halamanHuman Resource Management Practices at The National Thermal Power Corporation (NTPC) in Indiagramana10Belum ada peringkat

- WJEC Economics AS Unit 2 QP S19Dokumen7 halamanWJEC Economics AS Unit 2 QP S19angeleschang99Belum ada peringkat

- Case Study Analysis: Ch. Sai Varun 191146 Sec-CDokumen2 halamanCase Study Analysis: Ch. Sai Varun 191146 Sec-CVarun NandaBelum ada peringkat

- Far 250Dokumen18 halamanFar 250Aisyah SaaraniBelum ada peringkat

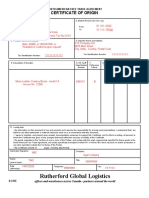

- Rutherford Global Logistics: Certificate of OriginDokumen1 halamanRutherford Global Logistics: Certificate of OriginAnkita SinhaBelum ada peringkat

- MonopolyDokumen19 halamanMonopolyJames BondBelum ada peringkat

- Chapter-1 2Dokumen12 halamanChapter-1 2Claire Cadungog HernanBelum ada peringkat

- Lesson Chapter 5Dokumen52 halamanLesson Chapter 5Melessa PescadorBelum ada peringkat

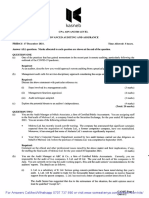

- PST AAA 2015 2022Dokumen45 halamanPST AAA 2015 2022mulika99Belum ada peringkat

- TUTORIAL 3 (Questions) Q1: UKAT3033/UBAT3033 Taxation IIDokumen2 halamanTUTORIAL 3 (Questions) Q1: UKAT3033/UBAT3033 Taxation IIIzaac PovanesBelum ada peringkat

- Chapter 7 - Compound Financial Instrument (FAR6)Dokumen5 halamanChapter 7 - Compound Financial Instrument (FAR6)Honeylet SigesmundoBelum ada peringkat

- Cips Fees - February 2019Dokumen2 halamanCips Fees - February 2019edd bazBelum ada peringkat

- Chap4 TheoryDokumen2 halamanChap4 TheoryAnonymous LC5kFdtcBelum ada peringkat

- WEBINAR-LAPENKOP@2021 - Ustadz Mursalin Maggangka, P.HDDokumen33 halamanWEBINAR-LAPENKOP@2021 - Ustadz Mursalin Maggangka, P.HDcooperative inovatorsBelum ada peringkat

- The History of The Philippine Currency: Republic Central CollegesDokumen8 halamanThe History of The Philippine Currency: Republic Central CollegesDaishin Kingsley SeseBelum ada peringkat

- 1 - Working Capital Management (Aditi)Dokumen50 halaman1 - Working Capital Management (Aditi)Preet PreetBelum ada peringkat

- Assignment 1 (HRM)Dokumen4 halamanAssignment 1 (HRM)Atul PrakashBelum ada peringkat

- MC SP Module 06 - Supply Planning Process DesignDokumen44 halamanMC SP Module 06 - Supply Planning Process Designsamah sBelum ada peringkat

- Impact of Fee Based and Fund Based Services On Profitability of BanksDokumen55 halamanImpact of Fee Based and Fund Based Services On Profitability of BanksNeeluSuthar100% (7)

- Brown Label & White Label ATMsDokumen2 halamanBrown Label & White Label ATMsSwastik Nandy100% (1)

- Interviews Value InvestingDokumen87 halamanInterviews Value Investinghkm_gmat4849100% (1)

- The Textile and Apparel Industry in India PDFDokumen11 halamanThe Textile and Apparel Industry in India PDFhoshmaBelum ada peringkat

- 6 Operations ImprovementDokumen30 halaman6 Operations ImprovementAnushaBalasubramanya100% (1)

- Economics Chap1Dokumen68 halamanEconomics Chap1samuelBelum ada peringkat

- Tesla FSAPDokumen20 halamanTesla FSAPSihongYanBelum ada peringkat

- Detailed Unit Price Analysis (DUPA) FORM POW-2015-01D-00Dokumen1 halamanDetailed Unit Price Analysis (DUPA) FORM POW-2015-01D-00Engineer ZaldyBelum ada peringkat

- Hospital Project 1Dokumen49 halamanHospital Project 1Rutvi Shah RathiBelum ada peringkat

- Ganzgraphy Photography & Cinematograph: QuotationDokumen1 halamanGanzgraphy Photography & Cinematograph: Quotationgana aruBelum ada peringkat

- Bnmit ConferenceDokumen4 halamanBnmit ConferenceBhavani B S PoojaBelum ada peringkat