Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Mohammed Musa Mohammed Karama: 2581132: 0033025811320001: Saving Account:: 03-10-2021Dokumen3 halamanMohammed Musa Mohammed Karama: 2581132: 0033025811320001: Saving Account:: 03-10-2021mohmaamed karamaBelum ada peringkat

- Janthakan SuksompuechDokumen4 halamanJanthakan SuksompuechIT100% (2)

- E Business & E Commerce (Modul 14)Dokumen36 halamanE Business & E Commerce (Modul 14)z god luckBelum ada peringkat

- BRAC Bank Limited - Cards P@y Flex ProgramDokumen3 halamanBRAC Bank Limited - Cards P@y Flex Programaliva78100% (2)

- Booking Confirmation On IRC TC, Train: 02622, 20-Oct-2021, 3A, NGP - Main: 02622, 20-Oct-2021, 3A, NGP - MASDokumen1 halamanBooking Confirmation On IRC TC, Train: 02622, 20-Oct-2021, 3A, NGP - Main: 02622, 20-Oct-2021, 3A, NGP - MASRahul VermaBelum ada peringkat

- Pembayaran PoltekkesDokumen12 halamanPembayaran PoltekkesteffiBelum ada peringkat

- PDFDokumen14 halamanPDFKamal RajBelum ada peringkat

- Domestic: Soumitra Roy & Tusi RoyDokumen2 halamanDomestic: Soumitra Roy & Tusi RoyAnonymous t5MrKaXDBelum ada peringkat

- Netsuite Electronic Payments: Securely Automate EFT Payments and Collections With A Single Global SolutionDokumen5 halamanNetsuite Electronic Payments: Securely Automate EFT Payments and Collections With A Single Global SolutionJawad HaiderBelum ada peringkat

- ATM Management SystemDokumen2 halamanATM Management SystemKanu Priya100% (1)

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokumen33 halamanDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceRahul RaoBelum ada peringkat

- SOC Branchless Banking April June 2023 PDFDokumen2 halamanSOC Branchless Banking April June 2023 PDFVijay VijdanBelum ada peringkat

- What Is Pesonet and Instapay?Dokumen4 halamanWhat Is Pesonet and Instapay?Shie MinimoBelum ada peringkat

- Payment Gateway TestingDokumen15 halamanPayment Gateway TestingavinashrocksBelum ada peringkat

- Cash Transaction Charges For Savings Account HoldersDokumen6 halamanCash Transaction Charges For Savings Account HoldersMaheshkumar AmulaBelum ada peringkat

- Final PayPal ReportDokumen5 halamanFinal PayPal ReportRajiv LamichhaneBelum ada peringkat

- Most Important Terms & Conditions: Schedule of ChargesDokumen12 halamanMost Important Terms & Conditions: Schedule of ChargesAmreshAmanBelum ada peringkat

- 1500XFree Paypal AccountDokumen42 halaman1500XFree Paypal AccountAnonymous 9JPEvlBelum ada peringkat

- UPIDokumen11 halamanUPIzxcvbnm1230Belum ada peringkat

- Csi Modes of PaymentDokumen1 halamanCsi Modes of PaymentLope Nam-iBelum ada peringkat

- DBBL StatementDokumen1 halamanDBBL StatementKazi Foyez Ahmed75% (16)

- Statement 41872409 NZD 2023-02-16 2023-03-18Dokumen2 halamanStatement 41872409 NZD 2023-02-16 2023-03-18Antonio MouraBelum ada peringkat

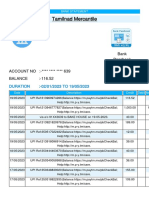

- Tamilnad Mercantile1684550531048Dokumen25 halamanTamilnad Mercantile1684550531048Miracle KhordsBelum ada peringkat

- Module 1. The Concept and Development of Money (Fina 221)Dokumen6 halamanModule 1. The Concept and Development of Money (Fina 221)MARITONI MEDALLABelum ada peringkat

- HDFC Credit Card Charge DetailsDokumen11 halamanHDFC Credit Card Charge DetailsVarun G ShenoyBelum ada peringkat

- BTC Staking LitepaperDokumen15 halamanBTC Staking LitepaperzoricadesousaBelum ada peringkat

- Bank Accounts: What You Should KnowDokumen36 halamanBank Accounts: What You Should Knowrohit7853Belum ada peringkat

- Account Name BSB Account Number Account Type Date OpenedDokumen6 halamanAccount Name BSB Account Number Account Type Date OpenedSandeep TuladharBelum ada peringkat

- Bellone 11 Day Pre GeneralDokumen17 halamanBellone 11 Day Pre GeneralRiverheadLOCALBelum ada peringkat

- Cash Cheque Deposit Slip V1Dokumen1 halamanCash Cheque Deposit Slip V1THUNDER GAMINGBelum ada peringkat