Anda mungkin juga menyukai

- Tool Kit for Tax Administration Management Information SystemDari EverandTool Kit for Tax Administration Management Information SystemPenilaian: 1 dari 5 bintang1/5 (1)

- ASEAN+3 Bond Market Guide 2017 Brunei DarussalamDari EverandASEAN+3 Bond Market Guide 2017 Brunei DarussalamBelum ada peringkat

- BAS Template PDFDokumen2 halamanBAS Template PDFrajkrishna03Belum ada peringkat

- Tax Payment Under GSTDokumen7 halamanTax Payment Under GSTAbhay GroverBelum ada peringkat

- Goods and Services Tax (GST) KnowledgeDokumen8 halamanGoods and Services Tax (GST) KnowledgeJaspreetSinghBelum ada peringkat

- GST Registration ProcessDokumen11 halamanGST Registration ProcessSalil BoranaBelum ada peringkat

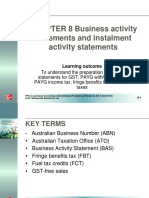

- CHAPTER 8 Business Activity Statements and Instalment Activity StatementsDokumen25 halamanCHAPTER 8 Business Activity Statements and Instalment Activity StatementsCJBelum ada peringkat

- Ingenico 5100 Paymark Merchant Quick Guide (Standard)Dokumen2 halamanIngenico 5100 Paymark Merchant Quick Guide (Standard)Synjon ElderBelum ada peringkat

- Workshop Case Study: Business Activity StatementDokumen21 halamanWorkshop Case Study: Business Activity StatementcollingwoodBelum ada peringkat

- Understanding and Using Quick Books Tax CodesDokumen6 halamanUnderstanding and Using Quick Books Tax CodesColin GoudieBelum ada peringkat

- A Reference Guide On VAT and GSTDokumen425 halamanA Reference Guide On VAT and GSTNalin kumarBelum ada peringkat

- The Script Guitar ChordDokumen5 halamanThe Script Guitar ChordIzack AnthonyBelum ada peringkat

- Topic 5 GST Tute SolutionsDokumen4 halamanTopic 5 GST Tute SolutionsHA Research ConsultancyBelum ada peringkat

- Pay As You Go (Payg) WithholdingDokumen70 halamanPay As You Go (Payg) WithholdingliamBelum ada peringkat

- Personality PortfolioDokumen28 halamanPersonality Portfolioapi-299171828Belum ada peringkat

- NFIU Suspicious Transaction ReportsDokumen30 halamanNFIU Suspicious Transaction ReportsDJNiyiBelum ada peringkat

- BOQ of Construction of TrellisDokumen1 halamanBOQ of Construction of Trellismichael jan de celisBelum ada peringkat

- AAT Willis CH02Dokumen15 halamanAAT Willis CH02CJ0% (1)

- BitLocker Drive Encryption Configuration Guide Backing Up BitLocker and TPM Recovery Information To Active DirectoryDokumen13 halamanBitLocker Drive Encryption Configuration Guide Backing Up BitLocker and TPM Recovery Information To Active DirectorynoBelum ada peringkat

- GST Accounting PDFDokumen17 halamanGST Accounting PDFBOO KIANG MINGBelum ada peringkat

- Account Opening Form For Resident Individuals Sole Proprietorship Firms PDFDokumen12 halamanAccount Opening Form For Resident Individuals Sole Proprietorship Firms PDFShashank YadavBelum ada peringkat

- Charge BackDokumen4 halamanCharge Backapi-3713147Belum ada peringkat

- TemplatesDokumen10 halamanTemplatesKayla BurnettBelum ada peringkat

- Buyer Registration FormDokumen3 halamanBuyer Registration FormPiyush ChaturvediBelum ada peringkat

- GST & BAS Detailed HandbookDokumen60 halamanGST & BAS Detailed Handbooktestnation100% (1)

- BUPA Intl Claim Form PDFDokumen4 halamanBUPA Intl Claim Form PDFisabellashBelum ada peringkat

- Case Study Atm-Se1Dokumen39 halamanCase Study Atm-Se1Hashim NaveedBelum ada peringkat

- Viral Collection Contract v2.5Dokumen3 halamanViral Collection Contract v2.5Desmond Tiongquico100% (1)

- Payroll Check ExplainedDokumen3 halamanPayroll Check Explainedfriendresh1708Belum ada peringkat

- ICICI Transaction SlipDokumen1 halamanICICI Transaction Sliparwa_mukadam03Belum ada peringkat

- TaxWorks Manual 2012Dokumen256 halamanTaxWorks Manual 2012chintankumar_patelBelum ada peringkat

- National Australia Bank LTD Code of ConductDokumen15 halamanNational Australia Bank LTD Code of ConductLogical UrbanBelum ada peringkat

- Tax AdministrationDokumen93 halamanTax AdministrationRobin LiuBelum ada peringkat

- Third Quarter 2007 Financial Review: Comerica IncorporatedDokumen34 halamanThird Quarter 2007 Financial Review: Comerica Incorporatedmdv31500Belum ada peringkat

- Property Occupations Form 6Dokumen6 halamanProperty Occupations Form 6Cara ElliottBelum ada peringkat

- Essentra BrochureDokumen68 halamanEssentra BrochureLp SaiBelum ada peringkat

- For Amo WebinarsDokumen79 halamanFor Amo WebinarsLiezl Tizon ColumnasBelum ada peringkat

- Guidelines Branchless Banking PDFDokumen34 halamanGuidelines Branchless Banking PDFTyrone HolmanBelum ada peringkat

- Increase Credit Limit PDFDokumen1 halamanIncrease Credit Limit PDFemc2_mcvBelum ada peringkat

- Mobey Forum Whitepaper - The MPOS Impact PDFDokumen32 halamanMobey Forum Whitepaper - The MPOS Impact PDFDeo ValenstinoBelum ada peringkat

- TWI Appilication FormDokumen3 halamanTWI Appilication FormVerdah SabihBelum ada peringkat

- Ohio LLC ApplicationDokumen6 halamanOhio LLC ApplicationamaddgeeBelum ada peringkat

- New SIM Reg SIM Swap Form With Consent Version 5Dokumen1 halamanNew SIM Reg SIM Swap Form With Consent Version 5ikperha jomafuvweBelum ada peringkat

- T Codes SapDokumen53 halamanT Codes Sapabhi2244inBelum ada peringkat

- 2018-Income-Statement Copy-2Dokumen9 halaman2018-Income-Statement Copy-2api-464285260Belum ada peringkat

- Mortgage Alliance - Policy ManualDokumen11 halamanMortgage Alliance - Policy ManualDanielBelum ada peringkat

- Chargeback Card InternetDokumen16 halamanChargeback Card InternetFlaviub23Belum ada peringkat

- Long For Success - Event Planning - Account ListDokumen119 halamanLong For Success - Event Planning - Account ListnnauthooBelum ada peringkat

- Fraud InvestigationDokumen6 halamanFraud InvestigationAvianah LindaBelum ada peringkat

- BSB40215 Certificate IV in Business BSBFIA402 Report On Financial ActivityDokumen12 halamanBSB40215 Certificate IV in Business BSBFIA402 Report On Financial Activity______.________Belum ada peringkat

- GST - Hospitality IndustryDokumen68 halamanGST - Hospitality IndustrySOPHIA POLYTECHNIC LIBRARYBelum ada peringkat

- Meghna Petroleum Limited: Chart of AccountsDokumen21 halamanMeghna Petroleum Limited: Chart of AccountsAbu Shahadat Muhammad SayeemBelum ada peringkat

- Hours and ProceduresDokumen4 halamanHours and ProceduresttawniaBelum ada peringkat

- US Internal Revenue Service: p4 - 1994Dokumen16 halamanUS Internal Revenue Service: p4 - 1994IRSBelum ada peringkat

- Sbi Home Loan Application FormDokumen5 halamanSbi Home Loan Application FormDhawan SandeepBelum ada peringkat

- Visa Form NigeriaDokumen3 halamanVisa Form NigeriaAvinash Kumar100% (1)

- 15 Tax Deductions You Should Know - E-Filing GuidanceDokumen32 halaman15 Tax Deductions You Should Know - E-Filing GuidanceErin LamBelum ada peringkat

- Practical Tips On Attracting DonationsDokumen4 halamanPractical Tips On Attracting DonationsBarpute ConsultancyBelum ada peringkat

- Cyber Laundering FinalDokumen70 halamanCyber Laundering Finalsalman jamali100% (2)

- Tax 2 Prefi Transcript Reduced FontDokumen81 halamanTax 2 Prefi Transcript Reduced FontPhil JaramilloBelum ada peringkat

- Sharad Vijayvargiya@PepsicoDokumen75 halamanSharad Vijayvargiya@PepsicoSharad VijayBelum ada peringkat

- 3 Assignment Cost Allocation, Customer Profitability Analysis and Sales VarianceDokumen4 halaman3 Assignment Cost Allocation, Customer Profitability Analysis and Sales VarianceRohan TrivediBelum ada peringkat

- Point of Sale PoSDokumen21 halamanPoint of Sale PoSBenhur LeoBelum ada peringkat

- 4P's of Berger Paints Bangladesh LimitedDokumen24 halaman4P's of Berger Paints Bangladesh Limitedনিশীথিনী কুহুরানীBelum ada peringkat

- Fitting OfferDokumen3 halamanFitting OfferMohit TyagiBelum ada peringkat

- Z and Y T.code Atun DivDokumen6 halamanZ and Y T.code Atun DivDINESH SINGH BHATIBelum ada peringkat

- Business Simulation Group 2 Section B - Assessee (10th Nov)Dokumen7 halamanBusiness Simulation Group 2 Section B - Assessee (10th Nov)mahapatrarajeshranjanBelum ada peringkat

- Boise Automation Canada Ltd. - Case SolutionDokumen2 halamanBoise Automation Canada Ltd. - Case SolutionVanshGupta100% (1)

- Proforma Invoice For Roma ServicesDokumen1 halamanProforma Invoice For Roma ServicesAhimbisibwe BakerBelum ada peringkat

- Sps Aggabao Vs Parulan Jr.Dokumen18 halamanSps Aggabao Vs Parulan Jr.8111 aaa 1118Belum ada peringkat

- Larsen Chapter 4 SummaryDokumen2 halamanLarsen Chapter 4 SummaryMarina LaurenBelum ada peringkat

- Accounts Receivable and Inventory ManagementDokumen14 halamanAccounts Receivable and Inventory Managementmuhammad sami ullah khanBelum ada peringkat

- Winter Jam Coffee ShopDokumen20 halamanWinter Jam Coffee ShopAndra MantaBelum ada peringkat

- Selling and Sales Management: GroupDokumen49 halamanSelling and Sales Management: GroupMalik Yousaf AkramBelum ada peringkat

- Ex - Scenario and Sensitifity AnalysisDokumen3 halamanEx - Scenario and Sensitifity AnalysisSakura Rosella100% (1)

- Case Federal ExpressDokumen18 halamanCase Federal ExpressRizky RahmanBelum ada peringkat

- Cost ConceptsDokumen19 halamanCost ConceptsPrabha Karan100% (1)

- Reshawn Ullah Resume PDFDokumen1 halamanReshawn Ullah Resume PDFReshawn UllahBelum ada peringkat

- What Is Capital Gains Tax On Real EstateDokumen51 halamanWhat Is Capital Gains Tax On Real EstatePrateik RyukiBelum ada peringkat

- A Study On Market Survey On The Brand Equity of Pondicherry Co Operative Spinning Mills LTDDokumen42 halamanA Study On Market Survey On The Brand Equity of Pondicherry Co Operative Spinning Mills LTDessakiappanBelum ada peringkat

- Ty Bms Project On SebiDokumen36 halamanTy Bms Project On Sebilaxmi10120980% (5)

- Customer Relationship Management (CRM) : Dr. Saba FatmaDokumen104 halamanCustomer Relationship Management (CRM) : Dr. Saba FatmaAtharva DangeBelum ada peringkat

- Annex A - Application FormDokumen6 halamanAnnex A - Application FormDragan ŽivkovićBelum ada peringkat

- 13.1 Case StudyDokumen2 halaman13.1 Case StudyPac Kotcharag100% (1)

- AnirudhDokumen81 halamanAnirudhbalki123Belum ada peringkat

- Contact Center NG BayanDokumen7 halamanContact Center NG BayanSulong Pinas JRBelum ada peringkat

- A Project Report On E-Commerce Sales and Operations Through MarketplaceDokumen38 halamanA Project Report On E-Commerce Sales and Operations Through MarketplaceAmit JaiswatBelum ada peringkat

- Pricing: Understanding and Capturing Customer ValueDokumen31 halamanPricing: Understanding and Capturing Customer ValueAlrifai Ziad Ahmed100% (2)

- Think & Sell Like A CEO (Tony Parinello) PDFDokumen166 halamanThink & Sell Like A CEO (Tony Parinello) PDFrjcantwell100% (1)