Anda mungkin juga menyukai

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- 0455-Cambridge IGCSE Economics SyllabusDokumen12 halaman0455-Cambridge IGCSE Economics SyllabusNiaz MahmudBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Answers 1220618085860270 8Dokumen11 halamanAnswers 1220618085860270 8monalishas_171% (7)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- A Economics Gr. 12 Monopoly PresentationDokumen22 halamanA Economics Gr. 12 Monopoly PresentationHari prakarsh NimiBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Microeconomics, Module 11: "Monopoly" (Chapter 10) Homework Assignment (The AttachedDokumen3 halamanMicroeconomics, Module 11: "Monopoly" (Chapter 10) Homework Assignment (The Attached03137622424Belum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- English Competition For Fun 1Dokumen6 halamanEnglish Competition For Fun 1Linh Nguyễn Thị ThùyBelum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Cvru New Guide Book 2012-13 Arts - Selected 08-01-2013Dokumen164 halamanCvru New Guide Book 2012-13 Arts - Selected 08-01-2013Jignesh PatelBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Prospects and Challenges of Women Entrepreneurs in Ethiopia (Case Study Adama Town)Dokumen43 halamanProspects and Challenges of Women Entrepreneurs in Ethiopia (Case Study Adama Town)Emebet Tesema100% (3)

- Syllabus MBA 1ST SemDokumen11 halamanSyllabus MBA 1ST SemAayush AgrawalBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Ratio Analysis On Renuka Sugars Ltd.Dokumen77 halamanRatio Analysis On Renuka Sugars Ltd.Punardatt Bhat100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- West Bengal State Council of Technical & Vocational Education and Skill Development (Technical Education Division)Dokumen20 halamanWest Bengal State Council of Technical & Vocational Education and Skill Development (Technical Education Division)DebeshBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Economics PDFDokumen44 halamanEconomics PDFyesuBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- UT Dallas Syllabus For Meco6303.5u1.08u Taught by Peter Lewin (Plewin)Dokumen11 halamanUT Dallas Syllabus For Meco6303.5u1.08u Taught by Peter Lewin (Plewin)UT Dallas Provost's Technology GroupBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- University of Calicut: General and Academic Branch - I E' SectionDokumen86 halamanUniversity of Calicut: General and Academic Branch - I E' SectionFarash MuhamedBelum ada peringkat

- Distilleria Vs La TondeniaDokumen13 halamanDistilleria Vs La TondeniaJohnRouenTorresMarzoBelum ada peringkat

- Welfare Effects of Perfect CompetitionDokumen7 halamanWelfare Effects of Perfect CompetitionBoi NonoBelum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Analysis of Management Code 17 - Jun 2019 - Human PeritusDokumen7 halamanAnalysis of Management Code 17 - Jun 2019 - Human PeritusnitishBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Group 6 ResearchDokumen83 halamanGroup 6 ResearchJanine MalinaoBelum ada peringkat

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Characteristics of MicroeconomicsDokumen11 halamanCharacteristics of MicroeconomicsMaria JessaBelum ada peringkat

- Tips and Samples CH 10, MICRODokumen12 halamanTips and Samples CH 10, MICROtariku1234Belum ada peringkat

- Darshini 1207182007 Case Study 2Dokumen8 halamanDarshini 1207182007 Case Study 2MSubra Maniam100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

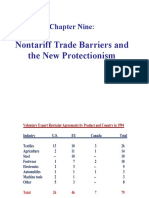

- Chapter Nine:: Nontariff Trade Barriers and The New ProtectionismDokumen26 halamanChapter Nine:: Nontariff Trade Barriers and The New ProtectionismAhmad RonyBelum ada peringkat

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Materi PAT (B. Inggris)Dokumen12 halamanMateri PAT (B. Inggris)ramona anaBelum ada peringkat

- Chapter 2: Evaluating A Firm's External EnvironmentDokumen20 halamanChapter 2: Evaluating A Firm's External Environmentqwerty1111112Belum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Bilateral & Multiplant MonopolyDokumen4 halamanBilateral & Multiplant MonopolyMuhammad UmairBelum ada peringkat

- Microecomomics Syllabus 2021Dokumen5 halamanMicroecomomics Syllabus 2021YEN NGO HAIBelum ada peringkat

- Purchasing Must Become Supply Management - Kraljic ModelDokumen3 halamanPurchasing Must Become Supply Management - Kraljic Modelkshf_azamBelum ada peringkat

- 2023 Econ Grade 11 p2 Nov MGDokumen21 halaman2023 Econ Grade 11 p2 Nov MGnhlesekaneneBelum ada peringkat

- The Politics of Antitrust and Merger Review in The European Union: Institutional Change and Decisions From Messina To 2004 Tim Büthe Gabriel T. SwankDokumen52 halamanThe Politics of Antitrust and Merger Review in The European Union: Institutional Change and Decisions From Messina To 2004 Tim Büthe Gabriel T. SwankMinda de Gunzburg Center for European Studies at Harvard UniversityBelum ada peringkat

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- 5 Steps To A 5 Ap Microeconomics 2024 Eric R Dodge Full ChapterDokumen67 halaman5 Steps To A 5 Ap Microeconomics 2024 Eric R Dodge Full Chapterthomas.kubica256100% (8)

- The Dark Enlightenment, Part 1 (Nick Land)Dokumen6 halamanThe Dark Enlightenment, Part 1 (Nick Land)Francisco VillarBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)