Anda mungkin juga menyukai

- Final Accounts PPT APTDokumen36 halamanFinal Accounts PPT APTGaurav gusai100% (1)

- Accounting Records and Final AccountsDokumen8 halamanAccounting Records and Final AccountsAjit Golchha0% (1)

- Accounting For LIPSADokumen20 halamanAccounting For LIPSAAjay Sahoo100% (1)

- Viva On Project and CfsDokumen7 halamanViva On Project and CfsCrazy GamerBelum ada peringkat

- Take It From NT:-Cash Book Plays Role of Both Journal As Well As LedgerDokumen17 halamanTake It From NT:-Cash Book Plays Role of Both Journal As Well As LedgerAnonymous b4qyneBelum ada peringkat

- Final AccountDokumen47 halamanFinal Accountsakshi tomarBelum ada peringkat

- Bank Reconciliation Statement Class 11 NotesDokumen10 halamanBank Reconciliation Statement Class 11 NotesAshna vargheseBelum ada peringkat

- Accounting Final AccountsDokumen20 halamanAccounting Final AccountsAjay SahooBelum ada peringkat

- Ascertainment of ProfitDokumen18 halamanAscertainment of ProfitsureshBelum ada peringkat

- Journal, Ledger, Trial BalanceDokumen24 halamanJournal, Ledger, Trial Balancesuneetcool00761% (28)

- Voucher Entry in Tally.ERP 9 (less than 40 charsDokumen57 halamanVoucher Entry in Tally.ERP 9 (less than 40 charsPraveen CoolBelum ada peringkat

- 2 Final Accounts - Sole Proprietor - Format - AdjustmentsDokumen14 halaman2 Final Accounts - Sole Proprietor - Format - AdjustmentsSudha Agarwal100% (1)

- Final Accounts ProblemDokumen21 halamanFinal Accounts Problemkramit1680% (10)

- Departmental AccountingDokumen6 halamanDepartmental AccountingAmit KumarBelum ada peringkat

- TdsDokumen22 halamanTdsFRANCIS JOSEPHBelum ada peringkat

- Accounting For Managers - FinalDokumen21 halamanAccounting For Managers - FinalAnuj SharmaBelum ada peringkat

- Management Accounting Chapter 4: Fund Flow Statement (FFS) : o o o o oDokumen21 halamanManagement Accounting Chapter 4: Fund Flow Statement (FFS) : o o o o oHemantha RajBelum ada peringkat

- Question Bank of Financial and Management Accounting - 2 MarkDokumen28 halamanQuestion Bank of Financial and Management Accounting - 2 MarklakkuMS100% (1)

- Basics of AccountingDokumen3 halamanBasics of AccountingAjesh Mukundan PBelum ada peringkat

- How external forces impact business strategiesDokumen7 halamanHow external forces impact business strategiesRevati MenghaniBelum ada peringkat

- Payroll in TallyDokumen227 halamanPayroll in Tallybhatia_priaBelum ada peringkat

- 08-Rectification-Of-Errors Good OneDokumen54 halaman08-Rectification-Of-Errors Good OneAejaz MohamedBelum ada peringkat

- Tally NotesDokumen76 halamanTally NotesManikandan Manohar100% (2)

- A Presentation On Cash Book, Pass Book & Bank Reconciliation Statement - Sudarshan Kr. PatelDokumen26 halamanA Presentation On Cash Book, Pass Book & Bank Reconciliation Statement - Sudarshan Kr. Patelsh0101100% (1)

- JM Institute of Technologies: Duration: 1 Hr. MM: 50Dokumen2 halamanJM Institute of Technologies: Duration: 1 Hr. MM: 50Rahul NigamBelum ada peringkat

- ITC Report and Accounts 2018Dokumen332 halamanITC Report and Accounts 2018Anonymous DfSizzc4lBelum ada peringkat

- Solved Problems: OlutionDokumen5 halamanSolved Problems: OlutionSavoir PenBelum ada peringkat

- History of Accounting StandardsDokumen62 halamanHistory of Accounting StandardsdestfertBelum ada peringkat

- Tally Erp 9.0 Material Creating Inventory Masters in Tally Erp 9.0Dokumen20 halamanTally Erp 9.0 Material Creating Inventory Masters in Tally Erp 9.0Raghavendra yadav KMBelum ada peringkat

- Jaiib Tricks To Remember Accounting StandardsDokumen3 halamanJaiib Tricks To Remember Accounting Standardshrocking1Belum ada peringkat

- PoaDokumen75 halamanPoaNISHANTH100% (1)

- Worksheet On Accounting For Partnership - Admission of A Partner Board QuestionsDokumen16 halamanWorksheet On Accounting For Partnership - Admission of A Partner Board QuestionsCfa Deepti BindalBelum ada peringkat

- Final-Accounts-Q - A P&L ACCDokumen31 halamanFinal-Accounts-Q - A P&L ACCNikhil PrasannaBelum ada peringkat

- Chapter 10 - Dividend PolicyDokumen37 halamanChapter 10 - Dividend PolicyShubhra Srivastava100% (1)

- Accounting For Specialized Institution Set 2 Scheme of ValuationDokumen19 halamanAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Dissolution QuestionsDokumen5 halamanDissolution Questionsstudyystuff7Belum ada peringkat

- Valuation of GoodwillDokumen6 halamanValuation of GoodwillPrasad NaikBelum ada peringkat

- Petty Cash Book BDokumen15 halamanPetty Cash Book Bgnanaselvi88Belum ada peringkat

- Royalty AccountsDokumen19 halamanRoyalty Accountsjashveer rekhi100% (2)

- 30 Transactions With Their Journal EntriesDokumen9 halaman30 Transactions With Their Journal EntriesPrashant BhardwajBelum ada peringkat

- Worksheet For Issue of Share and DebentureDokumen2 halamanWorksheet For Issue of Share and DebentureLaxmi Kant SahaniBelum ada peringkat

- TS Grewal Solutions for Class 11 Accountancy Chapter 14 - Capital and Revenue ExpenditureDokumen39 halamanTS Grewal Solutions for Class 11 Accountancy Chapter 14 - Capital and Revenue ExpenditureShivant GuptaBelum ada peringkat

- Jashobanti Project On Final AccountsDokumen17 halamanJashobanti Project On Final AccountsBiplab SwainBelum ada peringkat

- Love Letter by An AccountantDokumen2 halamanLove Letter by An AccountantRakshi BegumBelum ada peringkat

- Extra Questions - Financial Statements (Final Accounts) - Everonn - Class-11th CommerceDokumen26 halamanExtra Questions - Financial Statements (Final Accounts) - Everonn - Class-11th Commerceganesh86.1250% (4)

- Questions and Answers About TallyDokumen9 halamanQuestions and Answers About TallykumarbcomcaBelum ada peringkat

- Accounting and BookkeepingDokumen37 halamanAccounting and BookkeepingtekleyBelum ada peringkat

- Rectification of ErrorsDokumen23 halamanRectification of ErrorsSarthak GuptaBelum ada peringkat

- Project On Finalization of Partnership FirmDokumen38 halamanProject On Finalization of Partnership Firmvenkynaidu67% (3)

- Tally Erp 9.0 Material Tax Collected at Source Tally Erp 9.0Dokumen25 halamanTally Erp 9.0 Material Tax Collected at Source Tally Erp 9.0Raghavendra yadav KMBelum ada peringkat

- 01 Sample PaperDokumen24 halaman01 Sample Papergaming loverBelum ada peringkat

- Bad Debts and Provision For Doubtful DebtDokumen22 halamanBad Debts and Provision For Doubtful DebtNauman HashmiBelum ada peringkat

- Mod 4.2Dokumen27 halamanMod 4.2NitishBelum ada peringkat

- Adjustments for Bad Debts and DiscountsDokumen24 halamanAdjustments for Bad Debts and DiscountsMuhammad Adib100% (2)

- Final Account (Satyanath Mohapatra)Dokumen38 halamanFinal Account (Satyanath Mohapatra)smrutiranjan swainBelum ada peringkat

- Adjusting Entries in Accounting - Introduction: Accounting Cycle Preparing A Trial BalanceDokumen4 halamanAdjusting Entries in Accounting - Introduction: Accounting Cycle Preparing A Trial BalanceJayne Carly CabardoBelum ada peringkat

- Financial Statements II Class 11 Notes CBSE Accountancy Chapter 10 PDF 1Dokumen7 halamanFinancial Statements II Class 11 Notes CBSE Accountancy Chapter 10 PDF 1Parth PahwaBelum ada peringkat

- Financial AccountingDokumen6 halamanFinancial Accountingprachi kewalramaniBelum ada peringkat

- Final AccountDokumen14 halamanFinal AccountStiloflexindia Enterprise100% (1)

- Homework QuestionsDokumen17 halamanHomework QuestionsABelum ada peringkat

- Exchange Traded FundsDokumen24 halamanExchange Traded FundsSarthak GuptaBelum ada peringkat

- Fundamental AnalysisDokumen46 halamanFundamental AnalysisSarthak GuptaBelum ada peringkat

- Money and Capital Markets - OverviewDokumen16 halamanMoney and Capital Markets - OverviewSarthak GuptaBelum ada peringkat

- Is Development ConceptsDokumen46 halamanIs Development ConceptsSarthak GuptaBelum ada peringkat

- Reverse MortgageDokumen28 halamanReverse MortgageSarthak GuptaBelum ada peringkat

- Introduction To Organizational SystemsDokumen76 halamanIntroduction To Organizational SystemsSarthak GuptaBelum ada peringkat

- FM - Private EquityDokumen19 halamanFM - Private EquityAniket SinghBelum ada peringkat

- Made By:: Anshul Gupta Ankit Gupta Mohit Jain Prashant Priyadarshi Prateek Mishra Rahul SharmaDokumen29 halamanMade By:: Anshul Gupta Ankit Gupta Mohit Jain Prashant Priyadarshi Prateek Mishra Rahul SharmaSarthak GuptaBelum ada peringkat

- Sovereign Wealth FundsDokumen22 halamanSovereign Wealth FundsSarthak GuptaBelum ada peringkat

- Sources of Long Term FinanceDokumen13 halamanSources of Long Term FinanceSarthak GuptaBelum ada peringkat

- Current TrendsDokumen38 halamanCurrent TrendsSarthak GuptaBelum ada peringkat

- Excel Data AnalysisDokumen14 halamanExcel Data AnalysisSarthak GuptaBelum ada peringkat

- Information Systems in BusinessDokumen58 halamanInformation Systems in BusinessSarthak GuptaBelum ada peringkat

- Information Systems in Functional AreasDokumen77 halamanInformation Systems in Functional AreasSarthak GuptaBelum ada peringkat

- 05b-Sales Force ManagementDokumen11 halaman05b-Sales Force ManagementSarthak GuptaBelum ada peringkat

- 06-Sales Management, Control and Professional ApproachDokumen12 halaman06-Sales Management, Control and Professional ApproachSarthak GuptaBelum ada peringkat

- 05a Sales OrganisationDokumen13 halaman05a Sales OrganisationSarthak GuptaBelum ada peringkat

- ISM - Information Systems - Basic ConceptsDokumen68 halamanISM - Information Systems - Basic ConceptsSarthak Gupta100% (1)

- Sales Management: Some of The Important Terms Are As UnderDokumen14 halamanSales Management: Some of The Important Terms Are As UnderSarthak GuptaBelum ada peringkat

- 03-Role & Responsibility Sales PersonDokumen6 halaman03-Role & Responsibility Sales PersonSarthak GuptaBelum ada peringkat

- Organization Change & DevelopmentDokumen33 halamanOrganization Change & DevelopmentSarthak GuptaBelum ada peringkat

- 01-02-Introduction and Personal SellingDokumen17 halaman01-02-Introduction and Personal SellingSarthak GuptaBelum ada peringkat

- LearningDokumen44 halamanLearningSarthak GuptaBelum ada peringkat

- Techniques of Stress MGT CopingDokumen3 halamanTechniques of Stress MGT CopingSarthak GuptaBelum ada peringkat

- Power and PoliticsDokumen23 halamanPower and PoliticsSarthak GuptaBelum ada peringkat

- Organizational Culture 2Dokumen11 halamanOrganizational Culture 2Sarthak GuptaBelum ada peringkat

- Inductive and Deductive ReasoningDokumen1 halamanInductive and Deductive ReasoningSarthak GuptaBelum ada peringkat

- NegotiationDokumen9 halamanNegotiationSarthak GuptaBelum ada peringkat

- Managing Stress and CopingDokumen15 halamanManaging Stress and CopingSarthak GuptaBelum ada peringkat

- Organizational CultureDokumen18 halamanOrganizational CultureSarthak GuptaBelum ada peringkat

- Intro & SwotDokumen26 halamanIntro & SwotPuneet Singh DhaniBelum ada peringkat

- Banking Sector Overview: Definitions, Regulation, FunctionsDokumen39 halamanBanking Sector Overview: Definitions, Regulation, FunctionsDieu NguyenBelum ada peringkat

- Module 2 Math of InvestmentDokumen17 halamanModule 2 Math of InvestmentvlythevergreenBelum ada peringkat

- Banks and TaglinesDokumen7 halamanBanks and TaglinesmanojballaBelum ada peringkat

- Philippine Postal Corporation Notes To Financial Statements 1. Agency ProfileDokumen15 halamanPhilippine Postal Corporation Notes To Financial Statements 1. Agency ProfileJD BallosBelum ada peringkat

- Quiz 1 (Answer)Dokumen3 halamanQuiz 1 (Answer)Ali SaeedBelum ada peringkat

- Metrobank A Filipino Global CorporationDokumen2 halamanMetrobank A Filipino Global CorporationG'well Maika LongcopBelum ada peringkat

- Interest Rates and Bond Valuation Chapter 6Dokumen29 halamanInterest Rates and Bond Valuation Chapter 6Mariana MuñozBelum ada peringkat

- Loan Agreement Template 3Dokumen4 halamanLoan Agreement Template 3Athena Salas0% (1)

- Col. House and The League of NationsDokumen5 halamanCol. House and The League of NationsSolomon Cosmin Ionut100% (1)

- GR No. 7593, March 27, 1913: Supreme Court of The PhilippinesDokumen6 halamanGR No. 7593, March 27, 1913: Supreme Court of The PhilippinesM A J esty FalconBelum ada peringkat

- Pedersen - Wall Street Primer (2009)Dokumen262 halamanPedersen - Wall Street Primer (2009)Cosmin VintilăBelum ada peringkat

- Financial Analysis of HDFC BankDokumen48 halamanFinancial Analysis of HDFC BankAbhay JainBelum ada peringkat

- Panoramic Kerala GetawayDokumen11 halamanPanoramic Kerala GetawaymailsrinyBelum ada peringkat

- Multination Finance Butler 5th EditionDokumen3 halamanMultination Finance Butler 5th EditionUnostudent2014Belum ada peringkat

- DEBT BURDEN LIBERATION CERTIFICATE English Translated 22 2 2016Dokumen4 halamanDEBT BURDEN LIBERATION CERTIFICATE English Translated 22 2 2016WORLD MEDIA & COMMUNICATIONS80% (5)

- Games v. Allied BankingDokumen8 halamanGames v. Allied BankingRoan HabocBelum ada peringkat

- Treasury BillsDokumen11 halamanTreasury BillspoojaBelum ada peringkat

- HRMDokumen57 halamanHRMShaheen MahmudBelum ada peringkat

- P&S Bylaw 2072 II Amendment in NepaliDokumen27 halamanP&S Bylaw 2072 II Amendment in NepaliNarayanPrajapatiBelum ada peringkat

- Configuration of SAP Special GLDokumen20 halamanConfiguration of SAP Special GLAtulWalvekar100% (3)

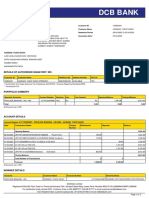

- DCB Bank: Statement of AccountDokumen2 halamanDCB Bank: Statement of AccounthasnainBelum ada peringkat

- Zain - Management TeamDokumen2 halamanZain - Management TeamalbidaiaBelum ada peringkat

- CF Chapter 4Dokumen25 halamanCF Chapter 4ASHWIN MOHANTYBelum ada peringkat

- 2034 Glyn CT New Water BillDokumen2 halaman2034 Glyn CT New Water BillAce MereriaBelum ada peringkat

- Business ServicesDokumen11 halamanBusiness ServicesBhoomi KachhiaBelum ada peringkat

- GRC - Governance, Risk Management, and ComplianceDokumen16 halamanGRC - Governance, Risk Management, and ComplianceBhavesh RathodBelum ada peringkat

- Interim Statement 10-Mar-2023 12-25-49Dokumen2 halamanInterim Statement 10-Mar-2023 12-25-49zani arslanBelum ada peringkat

- CH 5 Place of SupplyDokumen63 halamanCH 5 Place of SupplyManas Kumar SahooBelum ada peringkat

- Macro-Chapter 16 - UnlockedDokumen10 halamanMacro-Chapter 16 - UnlockedTrúc LinhBelum ada peringkat