Anda mungkin juga menyukai

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- CPPIB's Private Equity Strategy vs Fund of FundsDokumen3 halamanCPPIB's Private Equity Strategy vs Fund of FundsJitesh Thakur100% (1)

- Resume Book: Columbia Healthcare and Pharmaceutical Management ProgramDokumen44 halamanResume Book: Columbia Healthcare and Pharmaceutical Management ProgramJohn Mathias100% (2)

- Day Trading Money ManagementDokumen8 halamanDay Trading Money ManagementJoe PonziBelum ada peringkat

- Soleadea Mock Exam 1 Level I CFADokumen33 halamanSoleadea Mock Exam 1 Level I CFAAshutosh Singh100% (3)

- Finals - Assignment 4 PDFDokumen2 halamanFinals - Assignment 4 PDFcharlies parrenoBelum ada peringkat

- Group 10 VivendiDokumen18 halamanGroup 10 Vivendipkm84uch100% (1)

- Apprenticeships To Change The WorldDokumen36 halamanApprenticeships To Change The WorldKhawaja SohailBelum ada peringkat

- Ratios Analysis For StudentsDokumen16 halamanRatios Analysis For StudentsMichael AsieduBelum ada peringkat

- 2 ACC5215 2020 M11 Associates and JV All SlidesDokumen23 halaman2 ACC5215 2020 M11 Associates and JV All SlidesDev GargBelum ada peringkat

- Cfa Level III Errata PDFDokumen7 halamanCfa Level III Errata PDFTran HongBelum ada peringkat

- Eco Project Chapter 5Dokumen2 halamanEco Project Chapter 5Sanket KumarBelum ada peringkat

- Factsheet NiftyMidcapSelectDokumen2 halamanFactsheet NiftyMidcapSelectmohanchinnaiya7Belum ada peringkat

- AFARDokumen15 halamanAFARBetchelyn Dagwayan BenignosBelum ada peringkat

- Ponzi SchemesDokumen4 halamanPonzi SchemesNisa Hajja Qadri HarahapBelum ada peringkat

- SHARESDokumen5 halamanSHARESMohammad Tariq AnsariBelum ada peringkat

- Water Ownership DatabaseDokumen21 halamanWater Ownership DatabaseAlessandre OliveiraBelum ada peringkat

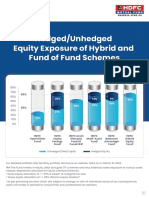

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDokumen2 halamanLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakBelum ada peringkat

- CRISIL Research - Ipo Grading Rat - Modern TubeDokumen12 halamanCRISIL Research - Ipo Grading Rat - Modern Tubejaydeep daveBelum ada peringkat

- BTMM Price-ActionDokumen4 halamanBTMM Price-ActionHamlet GalvezBelum ada peringkat

- Introduction to Currency Trading: The Ultimate Beginner's GuideDokumen25 halamanIntroduction to Currency Trading: The Ultimate Beginner's Guidearunchary007Belum ada peringkat

- Foreign Capital Inflows and Stock Market Development in PakistanDokumen10 halamanForeign Capital Inflows and Stock Market Development in PakistanSadaf KazmiBelum ada peringkat

- Exchange Rate Risk & Cost of CapitalDokumen22 halamanExchange Rate Risk & Cost of CapitalmonuBelum ada peringkat

- Practice Problems On LPPDokumen2 halamanPractice Problems On LPPFahad Ansari 20-296Belum ada peringkat

- Nepal Stock Exchange Ltd. Closing Price: Nepse Commercial Banks. PriceDokumen15 halamanNepal Stock Exchange Ltd. Closing Price: Nepse Commercial Banks. PriceChakra DahalBelum ada peringkat

- Feed The Future, Tanzania Land Tenure Assistance: DAI GlobalDokumen57 halamanFeed The Future, Tanzania Land Tenure Assistance: DAI GlobalJacob PeterBelum ada peringkat

- Pro Forma Escrow AgreementDokumen4 halamanPro Forma Escrow AgreementJonathan P. Ong100% (1)

- Elliott Wave CalculatorDokumen11 halamanElliott Wave CalculatorthairckshanBelum ada peringkat

- Merchant Banking in IndiaDokumen66 halamanMerchant Banking in IndiaNitishMarathe80% (40)

- TA112. BQA F.L Solution CMA September 2022 Exam.Dokumen6 halamanTA112. BQA F.L Solution CMA September 2022 Exam.Mohammed Javed UddinBelum ada peringkat

- 201FIN Tutorial 3 Financial Statements Analysis and RatiosDokumen3 halaman201FIN Tutorial 3 Financial Statements Analysis and RatiosAbdulaziz HBelum ada peringkat