Anda mungkin juga menyukai

- The New Tycoons: Inside the Trillion Dollar Private Equity Industry That Owns EverythingDari EverandThe New Tycoons: Inside the Trillion Dollar Private Equity Industry That Owns EverythingPenilaian: 4.5 dari 5 bintang4.5/5 (20)

- Saving, Investment, and the Financial System ExplainedDokumen66 halamanSaving, Investment, and the Financial System ExplainedFTU K59 Trần Yến LinhBelum ada peringkat

- Tencent Credit SuisseDokumen18 halamanTencent Credit SuisseMan Ho LiBelum ada peringkat

- (BNP Paribas) DivDax. Trade 2009-2010 Dividend SwapDokumen10 halaman(BNP Paribas) DivDax. Trade 2009-2010 Dividend SwapaacmasterblasterBelum ada peringkat

- Ch1 Nature Purpose and Scope of Financial ManagementDokumen8 halamanCh1 Nature Purpose and Scope of Financial ManagementEmma Ruth Rabacal50% (2)

- Republic Planters Bank Vs AganaDokumen2 halamanRepublic Planters Bank Vs AganaHoven Macasinag100% (2)

- Financing Decisions-1Dokumen56 halamanFinancing Decisions-1rajniBelum ada peringkat

- ACC2002L Financial Management Question PackDokumen67 halamanACC2002L Financial Management Question PackAhamed NabeelBelum ada peringkat

- Chapter 17 Flashcards - QuizletDokumen34 halamanChapter 17 Flashcards - QuizletAlucard77777Belum ada peringkat

- NJ Mutual Fund Project On Wealth CreationDokumen62 halamanNJ Mutual Fund Project On Wealth CreationSandeepMishra100% (1)

- Equity and Debt: First Some RevisionDokumen44 halamanEquity and Debt: First Some RevisionHay JirenyaaBelum ada peringkat

- Taxation Topic 3Dokumen29 halamanTaxation Topic 3Philip Gwadenya100% (2)

- Market Expansion Strategy of Square Pharmaceuticals Ltd.Dokumen65 halamanMarket Expansion Strategy of Square Pharmaceuticals Ltd.skpaul21994% (18)

- SP, GP, LLC, LLP, C Corp, S Corp:: Decoding The Alphabet Soup of IncorporationDokumen18 halamanSP, GP, LLC, LLP, C Corp, S Corp:: Decoding The Alphabet Soup of Incorporationcain velazquezBelum ada peringkat

- Limits To The Use of DebtDokumen40 halamanLimits To The Use of DebtMasumBelum ada peringkat

- Saving and InvestingDokumen17 halamanSaving and InvestingCP Mario Pérez LópezBelum ada peringkat

- Chapter 19 Dividends and Other PayoutsDokumen28 halamanChapter 19 Dividends and Other PayoutsHUONG NGUYEN VU QUYNHBelum ada peringkat

- Dividend PolicyDokumen32 halamanDividend PolicyitandonBelum ada peringkat

- Topic 10 Dividend Policy (Chapter 16, Brealey) : Information Content of Stock RepurchasesDokumen8 halamanTopic 10 Dividend Policy (Chapter 16, Brealey) : Information Content of Stock RepurchasesHashashahBelum ada peringkat

- BUSINESS FINANCE: THE FUNCTIONS OF A FINANCIAL MANAGERDokumen67 halamanBUSINESS FINANCE: THE FUNCTIONS OF A FINANCIAL MANAGERMatin Chris KisomboBelum ada peringkat

- Personal Finance Chapter 14: Understanding Common and Preferred StockDokumen25 halamanPersonal Finance Chapter 14: Understanding Common and Preferred Stock陈皮乌鸡Belum ada peringkat

- The Scope of Corporate Finance: © 2009 Cengage Learning/South-WesternDokumen25 halamanThe Scope of Corporate Finance: © 2009 Cengage Learning/South-WesternGenesis E. CarlosBelum ada peringkat

- Business Finance Chapter 1Dokumen43 halamanBusiness Finance Chapter 1Arafat UjjamanBelum ada peringkat

- UEU Manajemen Keuangan Pertemuan 3Dokumen51 halamanUEU Manajemen Keuangan Pertemuan 3HendriMaulanaBelum ada peringkat

- Chapter 1 - Accounting As A Form of Communication (Notes)Dokumen7 halamanChapter 1 - Accounting As A Form of Communication (Notes)Hareem Zoya WarsiBelum ada peringkat

- FE Chapter 16-Financial Structure of The FirmDokumen42 halamanFE Chapter 16-Financial Structure of The Firmnguyen tungBelum ada peringkat

- Corporate Governance and Other Stake HoldersDokumen15 halamanCorporate Governance and Other Stake HoldersrizwancgaBelum ada peringkat

- Fin 440 - Chapter - 16Dokumen14 halamanFin 440 - Chapter - 16Mehedi HasanBelum ada peringkat

- Week 3 - Payout PolicyDokumen47 halamanWeek 3 - Payout Policyminh daoBelum ada peringkat

- Entrepreneurship Module 3Dokumen33 halamanEntrepreneurship Module 3Anantha KrishnanBelum ada peringkat

- FE Chapter 16-Financial Structure of The FirmDokumen42 halamanFE Chapter 16-Financial Structure of The Firmnguyen tungBelum ada peringkat

- Saving, Investment, and The Financial SystemDokumen47 halamanSaving, Investment, and The Financial Systemjoebob1230Belum ada peringkat

- CF2 - Chapter 2 Capital Structure - SVDokumen45 halamanCF2 - Chapter 2 Capital Structure - SVleducBelum ada peringkat

- Long Term Financing: An Introduction: University of Economics - Ho Chi Minh CityDokumen22 halamanLong Term Financing: An Introduction: University of Economics - Ho Chi Minh CityMai HồBelum ada peringkat

- Corporate Finance Payout PolicyDokumen22 halamanCorporate Finance Payout PolicyDonBelum ada peringkat

- CF - 01Dokumen43 halamanCF - 01Нндн Н'Belum ada peringkat

- FIN 370T WK 5 - Apply Homework HTTPS://WWW - Hwtutorial.com/category/fin-370Dokumen57 halamanFIN 370T WK 5 - Apply Homework HTTPS://WWW - Hwtutorial.com/category/fin-370Donny JobBelum ada peringkat

- UntitledDokumen25 halamanUntitledEhab M. Abdel HadyBelum ada peringkat

- Company AccountingDokumen28 halamanCompany AccountingBeanka PaulBelum ada peringkat

- Accounting For Companies: BCM 1204: Accounting in Business IiDokumen49 halamanAccounting For Companies: BCM 1204: Accounting in Business IiMaryjoy KilonzoBelum ada peringkat

- Chapters 4 and 5Dokumen15 halamanChapters 4 and 5Estee FongBelum ada peringkat

- Stock Valuation Module 4.2Dokumen98 halamanStock Valuation Module 4.2Jemille MangawanBelum ada peringkat

- Stock and Their ValuationDokumen28 halamanStock and Their ValuationNusret MimiBelum ada peringkat

- Getting Started - Principles of FinanceDokumen78 halamanGetting Started - Principles of FinanceTaqiya NadiyaBelum ada peringkat

- Rose Hudgins Eighth Edition Power Point Chapter 15 JimDokumen76 halamanRose Hudgins Eighth Edition Power Point Chapter 15 JimJordan FaselBelum ada peringkat

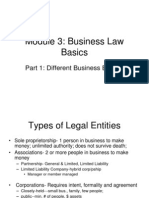

- Business Law - BasicDokumen30 halamanBusiness Law - BasicGama Kristian AdikurniaBelum ada peringkat

- Shareholders' EquityDokumen120 halamanShareholders' EquitySsewa AhmedBelum ada peringkat

- Strategic Financing DecisionsDokumen4 halamanStrategic Financing DecisionsushaBelum ada peringkat

- Lecture 1Dokumen44 halamanLecture 1Liyazhi LiuBelum ada peringkat

- FABM Fundamentals of ABM1Dokumen157 halamanFABM Fundamentals of ABM1Yoxi ZerunBelum ada peringkat

- The Scope of Corporate Finance: © 2009 Cengage Learning/South-WesternDokumen25 halamanThe Scope of Corporate Finance: © 2009 Cengage Learning/South-WesternPrema LathaBelum ada peringkat

- Chapter 6 - Essentials of Banking and FinanceDokumen27 halamanChapter 6 - Essentials of Banking and FinanceloubnaBelum ada peringkat

- Fundamentals of Corporate Finance Dividend and Stock Repurchase ChapterDokumen66 halamanFundamentals of Corporate Finance Dividend and Stock Repurchase ChapterKhadija AlkebsiBelum ada peringkat

- Corporate Finance FINA210 W1Dokumen36 halamanCorporate Finance FINA210 W1Jan DMAXBelum ada peringkat

- Topic 1 Overview of Financial Management and Financial EnvironmentDokumen68 halamanTopic 1 Overview of Financial Management and Financial EnvironmentMicaella Fevey BandejasBelum ada peringkat

- Dividend PolicyDokumen28 halamanDividend PolicySid Tushaar SiddharthBelum ada peringkat

- Chapter 15Dokumen49 halamanChapter 15m.garagan16Belum ada peringkat

- The 2012 Overture:: An Overview of Municipal BondsDokumen14 halamanThe 2012 Overture:: An Overview of Municipal BondsHannan KüçükBelum ada peringkat

- Understanding Financial StatementsDokumen16 halamanUnderstanding Financial StatementsCiarra CunananBelum ada peringkat

- CH 1Dokumen50 halamanCH 1zey9991Belum ada peringkat

- FINA2010 Financial Management: Lecture 2: Financial Statement AnalysisDokumen68 halamanFINA2010 Financial Management: Lecture 2: Financial Statement AnalysismoonBelum ada peringkat

- Long Term Sources of FundsDokumen63 halamanLong Term Sources of FundsAnonymous 9YyCbPABelum ada peringkat

- Corporate Finance Till Test 1Dokumen39 halamanCorporate Finance Till Test 1YogeeshBelum ada peringkat

- Lender Loan: Payoff - A Statement Prepared by ADokumen6 halamanLender Loan: Payoff - A Statement Prepared by AShrestha SachdevaBelum ada peringkat

- Corporate Finance Chapter6Dokumen20 halamanCorporate Finance Chapter6Dan688Belum ada peringkat

- Financial EconomicsDokumen18 halamanFinancial EconomicsvivianaBelum ada peringkat

- CF Topic 8 (Updated April 2020)Dokumen42 halamanCF Topic 8 (Updated April 2020)刘娅Belum ada peringkat

- Types of Business Organisations: Unit 1, Chapter 2Dokumen26 halamanTypes of Business Organisations: Unit 1, Chapter 2ananditaBelum ada peringkat

- Econ 371 Business Finance 1: Pirapa TharmalingamDokumen26 halamanEcon 371 Business Finance 1: Pirapa TharmalingamSamantha YuBelum ada peringkat

- ACC 642 - CH 01 SolutionsDokumen17 halamanACC 642 - CH 01 SolutionstboneuncwBelum ada peringkat

- Format of Revised Schedule VI To Companies Act 1956Dokumen23 halamanFormat of Revised Schedule VI To Companies Act 1956kuttaaBelum ada peringkat

- Pdf-Spend Compress PDFDokumen127 halamanPdf-Spend Compress PDFsabiyamathiasBelum ada peringkat

- Estimating Capital RequirementDokumen7 halamanEstimating Capital RequirementVishwo ShresthaBelum ada peringkat

- PromptDokumen10 halamanPromptRichik DadhichBelum ada peringkat

- Taxation and Investment in Thailand 2012 - DeloitteDokumen28 halamanTaxation and Investment in Thailand 2012 - DeloitteWISDOM-INGOODFAITHBelum ada peringkat

- Corporate Finance MCQs PDFDokumen63 halamanCorporate Finance MCQs PDFNhat QuangBelum ada peringkat

- Financial Management Theory and Practice 14th Edition Brigham Test BankDokumen36 halamanFinancial Management Theory and Practice 14th Edition Brigham Test Bankrappelpotherueo100% (20)

- Internship at The Outlook Group Task-1: Customer Relationship ManagementDokumen15 halamanInternship at The Outlook Group Task-1: Customer Relationship Managementrohit koyandeBelum ada peringkat

- Balance Sheet Ratio Analysis FormulaDokumen9 halamanBalance Sheet Ratio Analysis FormulaAbu Jahid100% (1)

- PracticeMock Bazooka September 2018 EditionDokumen61 halamanPracticeMock Bazooka September 2018 EditionCheenaBelum ada peringkat

- 2004-Lewis and Pendrill - Current Cost Accounting Developed-Chapter - 17Dokumen31 halaman2004-Lewis and Pendrill - Current Cost Accounting Developed-Chapter - 17EkralcdBelum ada peringkat

- Naspers FinancialDokumen169 halamanNaspers FinancialdaviesBelum ada peringkat

- Income from Other Sources ChapterDokumen5 halamanIncome from Other Sources ChapterSubramanian SenthilBelum ada peringkat

- Iifl - M-Reit - Kyc - 20200915Dokumen37 halamanIifl - M-Reit - Kyc - 20200915Saatvik ShettyBelum ada peringkat

- 434585710final Accounts QuestionDokumen15 halaman434585710final Accounts QuestionRithin RomyBelum ada peringkat

- BDO Unibank 2021 Annual Report Financial Highlights PDFDokumen2 halamanBDO Unibank 2021 Annual Report Financial Highlights PDFJohn Michael Dela CruzBelum ada peringkat

- Corporate Dividend Policy of Standard Bank GroupDokumen29 halamanCorporate Dividend Policy of Standard Bank GroupTivyaanga Chandra MohanBelum ada peringkat

- RecipeDokumen4 halamanRecipesasyedaBelum ada peringkat

- Taxation Law PrinciplesDokumen86 halamanTaxation Law PrinciplesEdmart Vicedo100% (1)

- Aramit Cement Limited: Rights Share Offer DocumentDokumen70 halamanAramit Cement Limited: Rights Share Offer DocumentSayeedMdAzaharulIslamBelum ada peringkat