Anda mungkin juga menyukai

- Summary of Joshua Rosenbaum & Joshua Pearl's Investment BankingDari EverandSummary of Joshua Rosenbaum & Joshua Pearl's Investment BankingBelum ada peringkat

- M&a PpaDokumen41 halamanM&a PpaAnna LinBelum ada peringkat

- 12 Things Not To Do in M&ADokumen15 halaman12 Things Not To Do in M&Aflorinj72Belum ada peringkat

- The Art of M&A Integration 2nd Ed: A Guide to Merging Resources, Processes,and ResponsibiltiesDari EverandThe Art of M&A Integration 2nd Ed: A Guide to Merging Resources, Processes,and ResponsibiltiesBelum ada peringkat

- JPM M&A BibleDokumen146 halamanJPM M&A BibleAly Kanji100% (1)

- Curing Corporate Short-Termism: Future Growth vs. Current EarningsDari EverandCuring Corporate Short-Termism: Future Growth vs. Current EarningsBelum ada peringkat

- The M&A Deal CycleDokumen17 halamanThe M&A Deal Cycledarkmagician3839151Belum ada peringkat

- Due Diligence The Critical Stage in Acquisitions and Mergers 0-566-08524-0Dokumen296 halamanDue Diligence The Critical Stage in Acquisitions and Mergers 0-566-08524-0Victor Nobiuz100% (3)

- Finance Due DelegenceDokumen12 halamanFinance Due DelegenceMohammed Abu-ElezzBelum ada peringkat

- Valulation Skills Session 2015Dokumen31 halamanValulation Skills Session 2015AndrewBelum ada peringkat

- How Synergies Drive Successful AcquisitionsDokumen24 halamanHow Synergies Drive Successful AcquisitionsClaudiu OprescuBelum ada peringkat

- Business Valuation M&a and Post Merger IntegrationDokumen63 halamanBusiness Valuation M&a and Post Merger IntegrationKlaus LaurBelum ada peringkat

- M&A Roadmap: W578 Final ProjectDokumen11 halamanM&A Roadmap: W578 Final ProjectJosé Pablo (JP) Vega100% (2)

- Accenture Inside Corporate MandADokumen28 halamanAccenture Inside Corporate MandAshshanksBelum ada peringkat

- CFA M&A Rationale Synergy Part 16 Aug 2020Dokumen195 halamanCFA M&A Rationale Synergy Part 16 Aug 2020aditya singhBelum ada peringkat

- WMF Buyout KKR Hec PDFDokumen116 halamanWMF Buyout KKR Hec PDFsukses100% (1)

- Positioning A Company For Sale: Silicon Forest ForumDokumen24 halamanPositioning A Company For Sale: Silicon Forest ForumraoplnsBelum ada peringkat

- Negotiations, Deal StructuringDokumen30 halamanNegotiations, Deal StructuringVishakha PawarBelum ada peringkat

- Sell Side M&ADokumen17 halamanSell Side M&AAbhishek SinghBelum ada peringkat

- M&A Integration: How To Do ItDokumen6 halamanM&A Integration: How To Do Itjeffhatch0% (1)

- LBO Sensitivity Tables BeforeDokumen37 halamanLBO Sensitivity Tables BeforeMamadouB100% (2)

- LBO PowerpointDokumen36 halamanLBO Powerpointfalarkys100% (1)

- Post Merger People IntegrationDokumen28 halamanPost Merger People IntegrationDebasish Chakraborty100% (4)

- M&ADokumen230 halamanM&APramod Gosavi100% (1)

- 07 DCF Steel Dynamics AfterDokumen2 halaman07 DCF Steel Dynamics AfterJack JacintoBelum ada peringkat

- M&ADokumen151 halamanM&APallavi Prasad100% (1)

- LBO In-Depth AnalysisDokumen12 halamanLBO In-Depth Analysisricoman19890% (1)

- Corporate RestructuringDokumen18 halamanCorporate Restructuring160286sanjeevjha50% (6)

- VP Corporate Development M&A in San Francisco Bay CA Resume Kostas KatsohirakisDokumen2 halamanVP Corporate Development M&A in San Francisco Bay CA Resume Kostas KatsohirakisKostasKatsohirakis100% (1)

- Ascend Hedge Fund Investment Due Diligence Report 0811redactedDokumen17 halamanAscend Hedge Fund Investment Due Diligence Report 0811redactedJoshua ElkingtonBelum ada peringkat

- M&A Deal CycleDokumen17 halamanM&A Deal Cycleoliver100% (1)

- PWC Roadmap For An IpoDokumen92 halamanPWC Roadmap For An IpoBassamBelum ada peringkat

- Guide For M&a-DeloitteDokumen21 halamanGuide For M&a-DeloitteFelipeGuimarãesBelum ada peringkat

- Private Equity Fund Study PDFDokumen237 halamanPrivate Equity Fund Study PDFprasan gudeBelum ada peringkat

- Sample Business Valuation - BAGDokumen43 halamanSample Business Valuation - BAGjeygar12Belum ada peringkat

- Introduction To M&ADokumen44 halamanIntroduction To M&AChirag ShahBelum ada peringkat

- 7 MA Docs DemystifiedDokumen30 halaman7 MA Docs Demystifiedwhaza789Belum ada peringkat

- How To Set Up A KPI Dashboard For Your Pre-Seed and Seed Stage Startup - Alex IskoldDokumen12 halamanHow To Set Up A KPI Dashboard For Your Pre-Seed and Seed Stage Startup - Alex IskoldLindsey SantosBelum ada peringkat

- Acquisition Integration Finance ChecklistDokumen4 halamanAcquisition Integration Finance Checklistleandropereira_itBelum ada peringkat

- Axial - 7 MA Documents DemystifiedDokumen23 halamanAxial - 7 MA Documents DemystifiedcubanninjaBelum ada peringkat

- LBO ModellingDokumen22 halamanLBO ModellingRoshan PriyadarshiBelum ada peringkat

- LBO Valuation Model PDFDokumen101 halamanLBO Valuation Model PDFAbhishek Singh100% (3)

- VP Corporate Finance CFO in Dallas Fort Worth TX Resume Joe RenfroeDokumen2 halamanVP Corporate Finance CFO in Dallas Fort Worth TX Resume Joe RenfroeJoeRenfroeBelum ada peringkat

- M and A Engagement Letters Power PointDokumen79 halamanM and A Engagement Letters Power PointjonnyrevBelum ada peringkat

- Concept Notes Mergers Acquisitions, and Strategic AlliancesDokumen233 halamanConcept Notes Mergers Acquisitions, and Strategic AlliancesvijayselvarajBelum ada peringkat

- M&A IntegrationDokumen36 halamanM&A IntegrationMarc ChanBelum ada peringkat

- Cogent Analytics M&A ManualDokumen19 halamanCogent Analytics M&A Manualvan070100% (1)

- PWC New M& A Accounting 2009Dokumen24 halamanPWC New M& A Accounting 2009wallstreetprepBelum ada peringkat

- PWC Pitch BookDokumen42 halamanPWC Pitch BookshruthiBelum ada peringkat

- Private Equity Valuation - BrochureDokumen5 halamanPrivate Equity Valuation - BrochureJustine9910% (1)

- Business Valuation Project Presentation: Sector: Pharmaceutical Stock, India: Cipla LTD Stock, USA: Mylan IncDokumen32 halamanBusiness Valuation Project Presentation: Sector: Pharmaceutical Stock, India: Cipla LTD Stock, USA: Mylan Incpuneet.glennBelum ada peringkat

- Comparable Companies AnalysisDokumen13 halamanComparable Companies AnalysisRehaan_Khan_RangerBelum ada peringkat

- Checklist M A It Integration Checklist Active Directory Technical Brief 27305Dokumen6 halamanChecklist M A It Integration Checklist Active Directory Technical Brief 27305lidiangBelum ada peringkat

- The AMA of Due DiligencyDokumen85 halamanThe AMA of Due DiligencySanjay Rathi100% (2)

- ValuationDokumen24 halamanValuationAkhil BansalBelum ada peringkat

- M&A ProcessDokumen20 halamanM&A ProcessSweta HansariaBelum ada peringkat

- Defenses Against Hostile TakeoversDokumen30 halamanDefenses Against Hostile TakeoversNeerav SharmaBelum ada peringkat

- Leveraged Buyout Structures and ValuationDokumen35 halamanLeveraged Buyout Structures and Valuationsamm123456100% (1)

- Income Declaration Scheme Rules, 2016: Form 1Dokumen9 halamanIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatBelum ada peringkat

- Types of Stamps and Some Concepts of Stamp DutyDokumen5 halamanTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

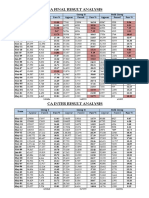

- CA Result AnalysisDokumen1 halamanCA Result AnalysisNikhil KasatBelum ada peringkat

- Black Money BillDokumen30 halamanBlack Money BillNikhil KasatBelum ada peringkat

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Dokumen21 halamanSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatBelum ada peringkat

- Hedging With Financial DerivativesDokumen30 halamanHedging With Financial DerivativesNikhil KasatBelum ada peringkat

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDokumen9 halamanAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatBelum ada peringkat

- CA Final Writing Professional Ethics AnswersDokumen2 halamanCA Final Writing Professional Ethics AnswersNikhil KasatBelum ada peringkat

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDokumen10 halamanFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatBelum ada peringkat

- Defamation Under Common LawDokumen6 halamanDefamation Under Common LawNikhil KasatBelum ada peringkat

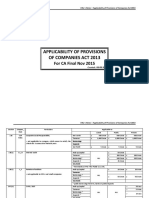

- ApplicabiliTY of ProvisionsDokumen3 halamanApplicabiliTY of ProvisionsNikhil KasatBelum ada peringkat

- Curriculum VitaeDokumen13 halamanCurriculum VitaeNikhil KasatBelum ada peringkat

- Privileges To Small CompaniesDokumen2 halamanPrivileges To Small CompaniesNikhil KasatBelum ada peringkat

- August Month CompliancesDokumen1 halamanAugust Month CompliancesNikhil KasatBelum ada peringkat

- SN Vertical Due Dates Particular Consequence of Non ComplianceDokumen1 halamanSN Vertical Due Dates Particular Consequence of Non ComplianceNikhil KasatBelum ada peringkat

- Cusoms Valuation MaterialDokumen8 halamanCusoms Valuation MaterialNikhil KasatBelum ada peringkat

- Blackbook M&aDokumen74 halamanBlackbook M&aSiddhartha100% (1)

- Chap 026Dokumen26 halamanChap 026suneshdeviBelum ada peringkat

- Hostile Takeover in Respect To IndiaDokumen39 halamanHostile Takeover in Respect To IndiadebankaBelum ada peringkat

- A Study On Acquisition of Aditya Birla Company and Columbian Chemicals CompanyDokumen42 halamanA Study On Acquisition of Aditya Birla Company and Columbian Chemicals Companysneha91210% (1)

- Hostile Takeovers India and Abroad - The Adani OneDokumen4 halamanHostile Takeovers India and Abroad - The Adani OneAditi SinghBelum ada peringkat

- US Board and EUDokumen55 halamanUS Board and EUschwarzardengrossBelum ada peringkat

- Growth Strategies Part 2Dokumen18 halamanGrowth Strategies Part 2sabyasachi samalBelum ada peringkat

- Chapter 1 5 DayagDokumen28 halamanChapter 1 5 DayagJymldy Encln100% (1)

- Time WarnerDokumen8 halamanTime WarnerGl AdityaBelum ada peringkat

- Manajemen Keuangan - Merger and Acquisition PDFDokumen36 halamanManajemen Keuangan - Merger and Acquisition PDFvrieskaBelum ada peringkat

- Case ADokumen7 halamanCase A徐楷筑Belum ada peringkat

- Anti-Takeover Defences in India (Rajat Kaushik)Dokumen35 halamanAnti-Takeover Defences in India (Rajat Kaushik)Abhimanyu SinghBelum ada peringkat

- Analysis On Combating Hostile TakeoversDokumen14 halamanAnalysis On Combating Hostile TakeoversLAW MANTRABelum ada peringkat

- Chapter 8Dokumen27 halamanChapter 8pranav sarawagiBelum ada peringkat

- Poison PillsDokumen15 halamanPoison Pillsadibhai06100% (1)

- Arcelor and Mittal Merger - Priyanshi and NidhiDokumen23 halamanArcelor and Mittal Merger - Priyanshi and Nidhipriyanshi gandhiBelum ada peringkat

- Mergers and Acquisitions: Mcgraw-Hill/Irwin Corporate Finance, 7/EDokumen13 halamanMergers and Acquisitions: Mcgraw-Hill/Irwin Corporate Finance, 7/EKrishna KumarBelum ada peringkat

- Z TheoriesDokumen255 halamanZ TheoriesKezBelum ada peringkat

- 5ffb Ims17Dokumen21 halaman5ffb Ims17Yvonne TotesoraBelum ada peringkat

- CHP 29Dokumen27 halamanCHP 29杰小Belum ada peringkat

- Golden Parachutes: KnightDokumen2 halamanGolden Parachutes: KnightLuciene SantosBelum ada peringkat

- Mergers Acquisitions and DivestituresDokumen58 halamanMergers Acquisitions and DivestituresAditya SinghBelum ada peringkat

- Poison Pill StrategyDokumen4 halamanPoison Pill StrategyAdnan AshrafBelum ada peringkat

- Icahn's Lawsuit Against Lions GateDokumen32 halamanIcahn's Lawsuit Against Lions GateDealBookBelum ada peringkat

- Theories Chapter1Dokumen15 halamanTheories Chapter1Aimee DyingBelum ada peringkat

- Session 5 and 6 M&A PGDM 2023Dokumen16 halamanSession 5 and 6 M&A PGDM 2023Archisman SahaBelum ada peringkat

- 05 Mergers and AcquisitionsDokumen40 halaman05 Mergers and AcquisitionsGabriel AmerBelum ada peringkat

- Ragupati Chandrasekaran's Notes From The Biglari Holdings 2012 Annual MeetingDokumen10 halamanRagupati Chandrasekaran's Notes From The Biglari Holdings 2012 Annual MeetingThe Manual of Ideas100% (1)

- Chapter 7 Strategic ControlDokumen55 halamanChapter 7 Strategic ControlejayBelum ada peringkat

- Assignment 7Dokumen9 halamanAssignment 7poddarprateek1Belum ada peringkat