Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Law On Sales:ReviewerDokumen51 halamanLaw On Sales:ReviewerfarBelum ada peringkat

- An Express TrustDokumen4 halamanAn Express TrustHo Wen HuiBelum ada peringkat

- G.R. No. L-27343 - Singson VDokumen18 halamanG.R. No. L-27343 - Singson Vabc defBelum ada peringkat

- Republic of The Philippines Regional Trial Court 5 Judicial Region Ligao City Branch 11Dokumen10 halamanRepublic of The Philippines Regional Trial Court 5 Judicial Region Ligao City Branch 11Jasmine Montero-GaribayBelum ada peringkat

- Manila Metal Container Corporation Vs Philippine NationalDokumen2 halamanManila Metal Container Corporation Vs Philippine NationalBernadetteGaleraBelum ada peringkat

- Philippine Aeolus Automotive United Corporation V NLRCDokumen1 halamanPhilippine Aeolus Automotive United Corporation V NLRCkeiffaceBelum ada peringkat

- Case Digest 1 Nmsmi Vs Military ShrineDokumen2 halamanCase Digest 1 Nmsmi Vs Military ShrineAronJames100% (2)

- Gue Vs RepublicDokumen2 halamanGue Vs RepublicRia Kriselle Francia PabaleBelum ada peringkat

- Sample Notice of Voluntary Dismissal Under Rule 41 in United States District CourtDokumen4 halamanSample Notice of Voluntary Dismissal Under Rule 41 in United States District CourtStan BurmanBelum ada peringkat

- Standard Professional Services Contract July 2009Dokumen28 halamanStandard Professional Services Contract July 2009volmink100% (1)

- Ortigas-Co-vs-Feati-Bank-DigestDokumen2 halamanOrtigas-Co-vs-Feati-Bank-DigestBea DiloyBelum ada peringkat

- Lichauco V LichaucoDokumen2 halamanLichauco V LichaucoNerissa BalboaBelum ada peringkat

- Gamboa Vs TevesDokumen6 halamanGamboa Vs TevesKaren Sheila B. Mangusan - DegayBelum ada peringkat

- Serg Products Vs PCI LeasingDokumen3 halamanSerg Products Vs PCI LeasingErika Angela Galceran100% (2)

- 33 SlideDokumen51 halaman33 SlidemohdsolahuddinBelum ada peringkat

- General Nature of The OASDHI ProgramDokumen43 halamanGeneral Nature of The OASDHI ProgrammohdsolahuddinBelum ada peringkat

- 28 SlideDokumen58 halaman28 SlidemohdsolahuddinBelum ada peringkat

- 30 SlideDokumen33 halaman30 SlidemohdsolahuddinBelum ada peringkat

- 32 SlideDokumen45 halaman32 SlidemohdsolahuddinBelum ada peringkat

- 34 SlideDokumen44 halaman34 SlidemohdsolahuddinBelum ada peringkat

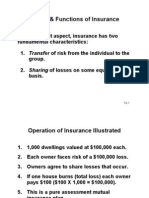

- Managing Organization Risks of Death and Disability: - As A Part of The Organization's Own RiskDokumen50 halamanManaging Organization Risks of Death and Disability: - As A Part of The Organization's Own RiskmohdsolahuddinBelum ada peringkat

- 27 SlideDokumen44 halaman27 SlidemohdsolahuddinBelum ada peringkat

- 23 SlideDokumen60 halaman23 SlidemohdsolahuddinBelum ada peringkat

- 21 SlideDokumen47 halaman21 SlidemohdsolahuddinBelum ada peringkat

- Employee Injuries: Risk Control: - For Many Businesses, The Largest Single ElementDokumen76 halamanEmployee Injuries: Risk Control: - For Many Businesses, The Largest Single ElementmohdsolahuddinBelum ada peringkat

- 22 SlideDokumen47 halaman22 SlidemohdsolahuddinBelum ada peringkat

- 25 SlideDokumen48 halaman25 SlidemohdsolahuddinBelum ada peringkat

- 19 SlideDokumen53 halaman19 SlidemohdsolahuddinBelum ada peringkat

- General Requirements - Enforceable ContractDokumen24 halamanGeneral Requirements - Enforceable ContractmohdsolahuddinBelum ada peringkat

- 20 SlideDokumen53 halaman20 SlidemohdsolahuddinBelum ada peringkat

- 17 SlideDokumen55 halaman17 SlidemohdsolahuddinBelum ada peringkat

- 16 SlideDokumen55 halaman16 SlidemohdsolahuddinBelum ada peringkat

- 10 SlideDokumen44 halaman10 SlidemohdsolahuddinBelum ada peringkat

- 18 SlideDokumen52 halaman18 SlidemohdsolahuddinBelum ada peringkat

- 15 SlideDokumen57 halaman15 SlidemohdsolahuddinBelum ada peringkat

- 12 SlideDokumen45 halaman12 SlidemohdsolahuddinBelum ada peringkat

- 14 SlideDokumen53 halaman14 SlidemohdsolahuddinBelum ada peringkat

- 11 SlideDokumen49 halaman11 SlidemohdsolahuddinBelum ada peringkat

- 07 DiskDokumen62 halaman07 DiskmohdsolahuddinBelum ada peringkat

- Before Anything Can Be Done About The Risks Facing An Organization, The Risks Must Be IdentifiedDokumen35 halamanBefore Anything Can Be Done About The Risks Facing An Organization, The Risks Must Be IdentifiedmohdsolahuddinBelum ada peringkat

- 08 DiskDokumen88 halaman08 DiskmohdsolahuddinBelum ada peringkat

- 09 DiskDokumen60 halaman09 DiskmohdsolahuddinBelum ada peringkat

- 03 DiskDokumen45 halaman03 DiskmohdsolahuddinBelum ada peringkat

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDokumen9 halamanBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDixie Mae JulveBelum ada peringkat

- Admissions: Balby Central Primary School Policy ForDokumen5 halamanAdmissions: Balby Central Primary School Policy ForcentralwebadminBelum ada peringkat

- PB Land Rev Act1882 Bk12Dokumen92 halamanPB Land Rev Act1882 Bk12VedBelum ada peringkat

- Application For Registration: Taxpayer Identification Number (TIN)Dokumen4 halamanApplication For Registration: Taxpayer Identification Number (TIN)Levi Tomol0% (2)

- DaVinci Editrice v. Ziko Games - Bang! Card Game CopyrightDokumen24 halamanDaVinci Editrice v. Ziko Games - Bang! Card Game CopyrightMark JaffeBelum ada peringkat

- 11 8 Soriano Padilla v. CADokumen28 halaman11 8 Soriano Padilla v. CAVanessa VelascoBelum ada peringkat

- Final - Complaint With ExhibitsDokumen273 halamanFinal - Complaint With ExhibitsAnn DwyerBelum ada peringkat

- Poet and PeasantDokumen1 halamanPoet and PeasantLuis ormeñoBelum ada peringkat

- Sudha Devi CaseDokumen15 halamanSudha Devi CaseAditiIndraniBelum ada peringkat

- Affidavit ProprietorshipDokumen2 halamanAffidavit Proprietorshipsumana rani100% (1)

- Peoria County Booking Sheet 09/02/13Dokumen8 halamanPeoria County Booking Sheet 09/02/13Journal Star police documentsBelum ada peringkat

- 8 Quita Vs CADokumen2 halaman8 Quita Vs CAGabriel DominguezBelum ada peringkat

- Deborah R. Hensler Nicholas Pace Bonita Dombey-Moore Beth Giddens Jennifer Gross Erik K. Moller-Class Action%Dokumen599 halamanDeborah R. Hensler Nicholas Pace Bonita Dombey-Moore Beth Giddens Jennifer Gross Erik K. Moller-Class Action%Lasmita SihalohoBelum ada peringkat

- Renewal Notice PrintDokumen1 halamanRenewal Notice PrinthamsBelum ada peringkat

- 7 - Liability Waiver, New Community Garden, Chicago ParksDokumen1 halaman7 - Liability Waiver, New Community Garden, Chicago ParksCelandine CharaBelum ada peringkat

- Cuadra Vs MonfortDokumen3 halamanCuadra Vs MonfortMJ DecolongonBelum ada peringkat