Anda mungkin juga menyukai

- Analysis of The Effect of Financial Ratio On Stock Returns of Non Cyclicals Consumer Companies Listed On IDX 2015-2020Dokumen11 halamanAnalysis of The Effect of Financial Ratio On Stock Returns of Non Cyclicals Consumer Companies Listed On IDX 2015-2020International Journal of Innovative Science and Research TechnologyBelum ada peringkat

- Determinant of ROE, CR, EPS, DER, PBV On Share Price On Mining Sector Companies Registered in IDX in 2014 - 2017Dokumen7 halamanDeterminant of ROE, CR, EPS, DER, PBV On Share Price On Mining Sector Companies Registered in IDX in 2014 - 2017Anonymous izrFWiQBelum ada peringkat

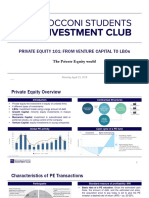

- Private Equity 101: From Venture Capital To LbosDokumen15 halamanPrivate Equity 101: From Venture Capital To LbosNeville SuraliwalaBelum ada peringkat

- Simon James & Clinton Alley - Tax Compliance, Self-Assessment and Tax AdministrationDokumen16 halamanSimon James & Clinton Alley - Tax Compliance, Self-Assessment and Tax AdministrationarekdarmoBelum ada peringkat

- Investments, 8 Edition: Equity Valuation ModelsDokumen45 halamanInvestments, 8 Edition: Equity Valuation ModelsErryBelum ada peringkat

- Excel Finance Tricks 1-17 FinishedDokumen52 halamanExcel Finance Tricks 1-17 FinishedXenopol XenopolBelum ada peringkat

- Soal Akuntansi ManajemenDokumen7 halamanSoal Akuntansi ManajemenInten RosmalinaBelum ada peringkat

- Return On Equity (Roe) Terhadap Harga Saham: Putri Hermawanti & Wahyu HidayatDokumen14 halamanReturn On Equity (Roe) Terhadap Harga Saham: Putri Hermawanti & Wahyu HidayatGanda Yulida Trisakti PamungkasBelum ada peringkat

- Strategic Cost Management (SCM) FrameworkDokumen11 halamanStrategic Cost Management (SCM) FrameworkcallmeasthaBelum ada peringkat

- Abc PDFDokumen6 halamanAbc PDFمحمد عقابنةBelum ada peringkat

- JKSW Annual Report 2017Dokumen54 halamanJKSW Annual Report 2017Riski Nurida RahmawatiBelum ada peringkat

- Write A Program in CDokumen12 halamanWrite A Program in Cmahima mishraBelum ada peringkat

- Stationery Management SystemDokumen4 halamanStationery Management SystemPawan Thareja25% (4)

- Ch01 Financial Reporting and Accounting StandardsDokumen27 halamanCh01 Financial Reporting and Accounting StandardsyyanpangBelum ada peringkat

- Standard Costs and Operating Performance MeasuresDokumen50 halamanStandard Costs and Operating Performance MeasuresJadeBelum ada peringkat

- Praktikum Akuntansi-BiayaDokumen27 halamanPraktikum Akuntansi-BiayaK-AnggunYulianaBelum ada peringkat

- Perencanaan Strategi Pemasaran Melalui Metode Swot Dan BCGDokumen12 halamanPerencanaan Strategi Pemasaran Melalui Metode Swot Dan BCGIqbhal WanaharaBelum ada peringkat

- Kelemahan Pengendalian InternalDokumen13 halamanKelemahan Pengendalian InternalSetio van HaostenBelum ada peringkat

- Innovative Management Methods in Terms of The Information Business Environment at The EnterpriseDokumen14 halamanInnovative Management Methods in Terms of The Information Business Environment at The EnterpriseIAEME PublicationBelum ada peringkat

- Chapter 5 Activity Based Cost SystemsDokumen40 halamanChapter 5 Activity Based Cost SystemsAli H. Ayoub100% (1)

- Write A Program in C To Simulate or To Implement A Stack Using A Pointer or StructureDokumen9 halamanWrite A Program in C To Simulate or To Implement A Stack Using A Pointer or StructureMunavalli Matt K SBelum ada peringkat

- 2022 Materi PSC Taxation FEBUPDokumen39 halaman2022 Materi PSC Taxation FEBUPvalen martaBelum ada peringkat

- Cost AccountingDokumen31 halamanCost Accountinguma soniBelum ada peringkat

- NPV & Other Investment Rules - RossDokumen30 halamanNPV & Other Investment Rules - RossPrometheus Smith100% (1)

- Solutions/solution Manual15Dokumen50 halamanSolutions/solution Manual15Bea BlancoBelum ada peringkat

- Ujian Akhir Semester 2014/2015: Akuntansi InternasionalDokumen5 halamanUjian Akhir Semester 2014/2015: Akuntansi InternasionalRatnaKemalaRitongaBelum ada peringkat

- Urnal Kuntansi Emerintah: Advance Pricing Agreement Dalam KaitannyaDokumen12 halamanUrnal Kuntansi Emerintah: Advance Pricing Agreement Dalam KaitannyaIin Mochamad SolihinBelum ada peringkat

- Soal Asistensi Akuntansi Manajemen 1-6Dokumen26 halamanSoal Asistensi Akuntansi Manajemen 1-6Lilik Adik KurniawanBelum ada peringkat

- 40 Corporate GovernanceDokumen34 halaman40 Corporate GovernanceNicolas Ernesto100% (1)

- Daa Project FileDokumen49 halamanDaa Project FileYogesh KathayatBelum ada peringkat

- Programming Fundamental (Swe-102) Assignment#01: Dated:28-01-2018Dokumen6 halamanProgramming Fundamental (Swe-102) Assignment#01: Dated:28-01-2018Samar FatimaBelum ada peringkat

- Investment Decision MethodDokumen44 halamanInvestment Decision MethodashwathBelum ada peringkat

- Contemporary Models of DevelopmentDokumen46 halamanContemporary Models of DevelopmentMuhammad Waqas100% (1)

- Feasibility Study of ProjectDokumen15 halamanFeasibility Study of ProjectMauliddha RachmiBelum ada peringkat

- Accounting Information System - Chapter 2Dokumen88 halamanAccounting Information System - Chapter 2Melisa May Ocampo AmpiloquioBelum ada peringkat

- ABC Costing (1) CostDokumen17 halamanABC Costing (1) CostMuhammad BilalBelum ada peringkat

- 2013 - SULI - SULI - Annual Report - 2013 PDFDokumen46 halaman2013 - SULI - SULI - Annual Report - 2013 PDFulfadwimustika0% (1)

- Eva & MvaDokumen5 halamanEva & MvaVineet ChouhanBelum ada peringkat

- Transfer PricingDokumen78 halamanTransfer Pricingirwansyah1617Belum ada peringkat

- Kotler Mm15e Inppt 18Dokumen25 halamanKotler Mm15e Inppt 18Hoàng Lâm LêBelum ada peringkat

- Bata Anual Report 2010Dokumen33 halamanBata Anual Report 2010Emon GtBelum ada peringkat

- Ch06 Payback PeriodDokumen6 halamanCh06 Payback Periodsunjith.sookdeo7441Belum ada peringkat

- 2009-01-06 043437 GoodDokumen3 halaman2009-01-06 043437 GoodAlthea LandichoBelum ada peringkat

- Ada Pharmaceutical Company Produces Three Drugs Diomycin HomycDokumen2 halamanAda Pharmaceutical Company Produces Three Drugs Diomycin HomycAmit PandeyBelum ada peringkat

- 1) / Write A Program To Print 0 01 010Dokumen54 halaman1) / Write A Program To Print 0 01 010rajbirkalerBelum ada peringkat

- Environmental Cost Management: Kelompok 1: Hilmy Fauzan Novia Kumala Sari Try SusantiDokumen34 halamanEnvironmental Cost Management: Kelompok 1: Hilmy Fauzan Novia Kumala Sari Try SusantiSeptian RizkyBelum ada peringkat

- Perhitungan IRR, BCR Dan NPVDokumen26 halamanPerhitungan IRR, BCR Dan NPVadhityamspBelum ada peringkat

- Case Study: Manajemen Logistik & Rantai PasokDokumen30 halamanCase Study: Manajemen Logistik & Rantai PasokDede AtmokoBelum ada peringkat

- Lakewood Laser Skincare S Ending Cash Balance As of January 31Dokumen1 halamanLakewood Laser Skincare S Ending Cash Balance As of January 31Let's Talk With HassanBelum ada peringkat

- McDonald's 2012-2013 Corporate Social Responsibility & Sustainability ReportDokumen116 halamanMcDonald's 2012-2013 Corporate Social Responsibility & Sustainability ReportedienewsBelum ada peringkat

- Porter Five Forces AnalysisDokumen6 halamanPorter Five Forces Analysisnaseeb_kakar_3Belum ada peringkat

- MCS Case 1-2Dokumen2 halamanMCS Case 1-2Shella FadelaBelum ada peringkat

- The Inherent Risk of Garuda Indonesia Around 2013 Until 2015Dokumen14 halamanThe Inherent Risk of Garuda Indonesia Around 2013 Until 2015arlindaBelum ada peringkat

- Romney Ch02Dokumen112 halamanRomney Ch02Maryjane YaranonBelum ada peringkat

- Implementing Activity Based CostingDokumen35 halamanImplementing Activity Based CostinggalaecumBelum ada peringkat

- Brigham & Ehrhardt: Financial Management: Theory and Practice 14eDokumen46 halamanBrigham & Ehrhardt: Financial Management: Theory and Practice 14eAmirah AliBelum ada peringkat

- Capital Budgeting TechniquesDokumen10 halamanCapital Budgeting TechniqueslehnehBelum ada peringkat

- Total Cost AnalysisDokumen10 halamanTotal Cost Analysisayane_sendoBelum ada peringkat

- Activity Based CostingDokumen29 halamanActivity Based CostingNaga Manasa KBelum ada peringkat

- PPT3201 W5Dokumen6 halamanPPT3201 W5Ayub Mohd AffendiBelum ada peringkat

- Maynard Operation Sequence Technique (MOST)Dokumen8 halamanMaynard Operation Sequence Technique (MOST)VivekBelum ada peringkat

- Ethics Case Coca-ColaDokumen2 halamanEthics Case Coca-ColaAmol AmraleBelum ada peringkat

- Chapter 2: Model of Scheduling Problem: Components of Any Model: - Decision Variables - Parameters - Objective FunctionDokumen23 halamanChapter 2: Model of Scheduling Problem: Components of Any Model: - Decision Variables - Parameters - Objective FunctionAmol AmraleBelum ada peringkat

- Services Management: 3-Focus On The CustomerDokumen7 halamanServices Management: 3-Focus On The CustomerAmol AmraleBelum ada peringkat

- 2 Gaps ModelDokumen10 halaman2 Gaps ModelAmol AmraleBelum ada peringkat

- Shoppers Stop Limited: ProfileDokumen3 halamanShoppers Stop Limited: ProfileAmol Amrale100% (1)

- Godrej Appliances Launches Largest Consumer Initiative On GreenDokumen3 halamanGodrej Appliances Launches Largest Consumer Initiative On GreenAmol AmraleBelum ada peringkat

- Amol 34Dokumen24 halamanAmol 34Amol AmraleBelum ada peringkat

- Order Winner and Order QualifiersDokumen10 halamanOrder Winner and Order QualifiersAmol AmraleBelum ada peringkat

- Lessons For Life: SE AgazDokumen5 halamanLessons For Life: SE AgazAmol AmraleBelum ada peringkat

- SSM ProDokumen13 halamanSSM ProAmol AmraleBelum ada peringkat

- Business Process Reengineering of An Air Cargo Handling ProcessDokumen12 halamanBusiness Process Reengineering of An Air Cargo Handling ProcessAmol AmraleBelum ada peringkat

- Fundamentals of Packaging TechnologyDokumen731 halamanFundamentals of Packaging TechnologyRohit Chawla94% (17)

- Img 20200920 0002Dokumen1 halamanImg 20200920 0002oniBelum ada peringkat

- EMD 2015 - Zielenkiewicz - Maksimowicz - Lightning Protection Zones Created by TractionDokumen5 halamanEMD 2015 - Zielenkiewicz - Maksimowicz - Lightning Protection Zones Created by TractionDHARMENDRABelum ada peringkat

- EX5 Dream110FI2018.CompressedDokumen106 halamanEX5 Dream110FI2018.CompressedZULUx9 SAADBelum ada peringkat

- Terex - Luffing TC.Dokumen16 halamanTerex - Luffing TC.guthaleBelum ada peringkat

- Jo 3120.4RDokumen271 halamanJo 3120.4RThinh Tien NguyenBelum ada peringkat

- Powergrid Organization ChartDokumen1 halamanPowergrid Organization ChartAnonymous l0MTRDGu3MBelum ada peringkat

- AED Design Requirements:: Sanitary Sewer & Septic SystemDokumen16 halamanAED Design Requirements:: Sanitary Sewer & Septic SystemIsuruSameeraBelum ada peringkat

- 1108 TicketDokumen2 halaman1108 TicketAnonymous TPVfFif6TOBelum ada peringkat

- Security Officer/GuardDokumen2 halamanSecurity Officer/Guardapi-121358674Belum ada peringkat

- Fundamentals of Automobile EngineeringDokumen18 halamanFundamentals of Automobile EngineeringLogeshwari RameshBelum ada peringkat

- Roof Headlining Assy: ComponentsDokumen3 halamanRoof Headlining Assy: Componentsjeremih alhegnBelum ada peringkat

- Desain Kebutuhan Unmanned Aerial Vehicle (Uav) Sebagai Pendukung Kegiatan Operasi Maritim BakamlaDokumen28 halamanDesain Kebutuhan Unmanned Aerial Vehicle (Uav) Sebagai Pendukung Kegiatan Operasi Maritim BakamlaDirektorat Penelitian dan Pengembangan Bakamla RIBelum ada peringkat

- 4.2 - Automatic Transmission (OCR)Dokumen156 halaman4.2 - Automatic Transmission (OCR)mnbvqwertBelum ada peringkat

- Bench Mark Nova CometDokumen41 halamanBench Mark Nova CometVeeresh T KumbarBelum ada peringkat

- NETZSCH Multiphase Pumps Crude Oil 07 12aDokumen16 halamanNETZSCH Multiphase Pumps Crude Oil 07 12aadrianioantomaBelum ada peringkat

- Parking Managements Solution For Teaching Hospital Karapitiya Galle Sri LankaDokumen33 halamanParking Managements Solution For Teaching Hospital Karapitiya Galle Sri LankaChiranjaya HulangamuwaBelum ada peringkat

- Daftar AccuDokumen3 halamanDaftar AccusetyoBelum ada peringkat

- Volvo TWD1643GE BrochureDokumen2 halamanVolvo TWD1643GE BrochureMTU650Belum ada peringkat

- NHAI Environment Impact AssesmentDokumen201 halamanNHAI Environment Impact AssesmentVinay Raj100% (1)

- Brewster Sb2a BuccaneerDokumen9 halamanBrewster Sb2a Buccaneerseafire470% (1)

- Commercial Invoice/Packing ListDokumen2 halamanCommercial Invoice/Packing ListVu Duc QuangBelum ada peringkat

- NL Liesinmovies Adv Ws 955569Dokumen6 halamanNL Liesinmovies Adv Ws 955569TheaBelum ada peringkat

- Statement of WorkDokumen12 halamanStatement of WorkSubash Gerrard DhakalBelum ada peringkat

- Risk Safety Management in Construction of Metro Rail ProjectsDokumen10 halamanRisk Safety Management in Construction of Metro Rail Projectsshailesh patilBelum ada peringkat

- 18SP546 (Search-Manual-Online - Com) PDFDokumen8 halaman18SP546 (Search-Manual-Online - Com) PDFJesus Vega HummerBelum ada peringkat

- B+V Manual - Power Slip, Hydraulic Op. PS 500 - Rev007 Valid From SN 45561-August 2008Dokumen106 halamanB+V Manual - Power Slip, Hydraulic Op. PS 500 - Rev007 Valid From SN 45561-August 2008施咏胜100% (3)

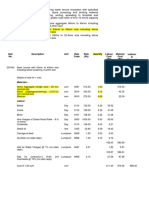

- Item No. Description Unit Rate Code Rate (RS) Quantity Labour Cost (RS) Material Cost (RS)Dokumen1 halamanItem No. Description Unit Rate Code Rate (RS) Quantity Labour Cost (RS) Material Cost (RS)RANADIP100% (2)

- CSP Panvel PDFDokumen79 halamanCSP Panvel PDFOMKAR JADHAVBelum ada peringkat

- Boudreau & McBirney 1997 PDFDokumen18 halamanBoudreau & McBirney 1997 PDFraguerreBelum ada peringkat