Anda mungkin juga menyukai

- Zechmeister Et Al. 2013 Page 30Dokumen1 halamanZechmeister Et Al. 2013 Page 30Pierre-Cécil KönigBelum ada peringkat

- Exploded Views and Parts List: 6-1 Indoor UnitDokumen11 halamanExploded Views and Parts List: 6-1 Indoor UnitandreiionBelum ada peringkat

- Shapes1 PDFDokumen2 halamanShapes1 PDFashleyBelum ada peringkat

- Captura de Pantalla 2023-09-21 A La(s) 5.32.58 P.M.Dokumen2 halamanCaptura de Pantalla 2023-09-21 A La(s) 5.32.58 P.M.Richard CarvajalBelum ada peringkat

- Subtraction Fluency Assessment-BrooksDokumen1 halamanSubtraction Fluency Assessment-Brooksapi-348736233Belum ada peringkat

- 22.01 IP4.2 MATH Rotation ExerciseDokumen1 halaman22.01 IP4.2 MATH Rotation ExerciseSong LoiBelum ada peringkat

- Rotate The Point: Sheet 1Dokumen2 halamanRotate The Point: Sheet 1Javzanlkham VanchinbazarBelum ada peringkat

- Cross-Hole Sonic Logging Test Record SheetDokumen1 halamanCross-Hole Sonic Logging Test Record Sheetkhraieric16Belum ada peringkat

- Answers Eighth Grade Find The Slope From A Graph Exit TicketDokumen1 halamanAnswers Eighth Grade Find The Slope From A Graph Exit TicketLousiana Dwinta UtamiBelum ada peringkat

- Transformation RotationsDokumen2 halamanTransformation RotationsyetriBelum ada peringkat

- Transformation RotationsDokumen2 halamanTransformation RotationsMazita BachokBelum ada peringkat

- A4 Quest 01 Adventure Hero Manual 10Dokumen6 halamanA4 Quest 01 Adventure Hero Manual 10Armand GuerreBelum ada peringkat

- Types of Slopes: NameDokumen2 halamanTypes of Slopes: NamehansBelum ada peringkat

- Activity 1 (Slope)Dokumen1 halamanActivity 1 (Slope)9CelbaJohnSzhayonMontoloBelum ada peringkat

- Name: Teacher: Date: Score:: RotationsDokumen2 halamanName: Teacher: Date: Score:: RotationsMadhavi KapadiaBelum ada peringkat

- Normam27 2019 EnglishDokumen161 halamanNormam27 2019 EnglishleobazethBelum ada peringkat

- Slope ks-BL3Dokumen1 halamanSlope ks-BL3Flaming Rose GamingBelum ada peringkat

- Transformation CombinedDokumen2 halamanTransformation CombinedRanBelum ada peringkat

- Write The Temperatures: Write The Temperatures: Write The Temperatures: Write The TemperaturesDokumen6 halamanWrite The Temperatures: Write The Temperatures: Write The Temperatures: Write The Temperaturesayman ayssaBelum ada peringkat

- KockaDokumen2 halamanKockaRyan Goh Chuang HongBelum ada peringkat

- Identifying Positive, Negative and Zero SlopesDokumen2 halamanIdentifying Positive, Negative and Zero SlopesJhems ElisBelum ada peringkat

- Graph Each Shape After Reflecting It As Directed.: NameDokumen2 halamanGraph Each Shape After Reflecting It As Directed.: NameKhatidja AllyBelum ada peringkat

- A4 Quest 03 PDFDokumen3 halamanA4 Quest 03 PDFsenhor_xBelum ada peringkat

- Transform The Quadrilaterals: Sheet 1Dokumen2 halamanTransform The Quadrilaterals: Sheet 1Javzanlkham VanchinbazarBelum ada peringkat

- Write The Fraction in WordsDokumen3 halamanWrite The Fraction in Wordsmomztutelage4182Belum ada peringkat

- Math Enlargement WorksheetsDokumen4 halamanMath Enlargement WorksheetsNadiva NuriftitahBelum ada peringkat

- Exercises InequalitiesInAlgebraDokumen1 halamanExercises InequalitiesInAlgebrareema ABDULLAHBelum ada peringkat

- Eighth Grade Find The Slope From A Graph Exit TicketDokumen1 halamanEighth Grade Find The Slope From A Graph Exit TicketLousiana Dwinta UtamiBelum ada peringkat

- Subtraction Timed Practice (0-3) : Name: - TimeDokumen2 halamanSubtraction Timed Practice (0-3) : Name: - TimeEllaine Mae TanBelum ada peringkat

- Rotations-21-4-23Dokumen2 halamanRotations-21-4-23tanishsangeethabalajiBelum ada peringkat

- Term 2 Maths Quiz 1 Q8-13Dokumen2 halamanTerm 2 Maths Quiz 1 Q8-13Kok Siong OngBelum ada peringkat

- QUADRATICS Notes and Homework Worksheets For TEAMDokumen21 halamanQUADRATICS Notes and Homework Worksheets For TEAMTrixiaBelum ada peringkat

- Candling Report Flock AnalysisDokumen6 halamanCandling Report Flock AnalysisMashrukh Islam SajalBelum ada peringkat

- Algebra1 Func Writing Equations 2Dokumen2 halamanAlgebra1 Func Writing Equations 2luis vimos calleBelum ada peringkat

- Spaceship Math Subtraction A 3-2, 3-1, 4-3, 4-1 Math Worksheet 1Dokumen2 halamanSpaceship Math Subtraction A 3-2, 3-1, 4-3, 4-1 Math Worksheet 1Wolf BorstBelum ada peringkat

- Front Squat Max Back Squat Max Day 3 Is BS OnlyDokumen4 halamanFront Squat Max Back Squat Max Day 3 Is BS OnlyHaft Cgb100% (1)

- Star Number Star Number: Battle Armor Record FormDokumen1 halamanStar Number Star Number: Battle Armor Record FormArt NicklesBelum ada peringkat

- Battle Armor Rs PDFDokumen1 halamanBattle Armor Rs PDFripecueBelum ada peringkat

- Star Number Star Number: Battle Armor Record FormDokumen1 halamanStar Number Star Number: Battle Armor Record FormCarlos GonzalezBelum ada peringkat

- BT - Battle Armour Record SheetDokumen1 halamanBT - Battle Armour Record SheetFabianoBorgBelum ada peringkat

- Find The Slope: Sheet 2Dokumen2 halamanFind The Slope: Sheet 2NouBooMBelum ada peringkat

- Transform The Triangles: Sheet 1Dokumen2 halamanTransform The Triangles: Sheet 1Franca OkechukwuBelum ada peringkat

- A4 Quest 01 Adventure Hero Manual 1 1 ENGDokumen6 halamanA4 Quest 01 Adventure Hero Manual 1 1 ENGGennaro FilomeneBelum ada peringkat

- Transform Triangles1 PDFDokumen2 halamanTransform Triangles1 PDFJavzanlkham VanchinbazarBelum ada peringkat

- 2nd Level Practice Sheet PDFDokumen9 halaman2nd Level Practice Sheet PDFMariam Atef100% (2)

- Master the Abacus Level 2 Sheet 1Dokumen9 halamanMaster the Abacus Level 2 Sheet 1vinayak50% (2)

- 2nd Level Practice Sheet PDFDokumen9 halaman2nd Level Practice Sheet PDFGirish Jha100% (1)

- 2nd Level Practice Sheet PDFDokumen9 halaman2nd Level Practice Sheet PDFChandrashekhar GurnuleBelum ada peringkat

- Solving Matrix Equation AxbDokumen6 halamanSolving Matrix Equation AxbCarloXs Xs MglBelum ada peringkat

- DSDSDSSDokumen6 halamanDSDSDSSCarloXs Xs MglBelum ada peringkat

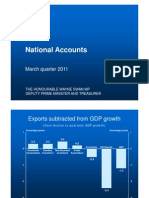

- National Accounts National Accounts: March Quarter 2011Dokumen6 halamanNational Accounts National Accounts: March Quarter 2011api-64584013Belum ada peringkat

- Find The Slope: Calculate The Rise and Run To Find The Slope of Each LineDokumen2 halamanFind The Slope: Calculate The Rise and Run To Find The Slope of Each Lineapi-703253998Belum ada peringkat

- Rise Over Run To Find Gradient With Given Graphs WSDokumen2 halamanRise Over Run To Find Gradient With Given Graphs WSafzabbasi100% (1)

- Rise Run Level1 1Dokumen2 halamanRise Run Level1 1hans100% (1)

- FlujoDokumen4 halamanFlujoHector RomeroBelum ada peringkat

- Graphing Points and Identifying ShapesDokumen2 halamanGraphing Points and Identifying ShapesCyrilBelum ada peringkat

- AB緩啟動器用戶手冊Dokumen148 halamanAB緩啟動器用戶手冊fly19810922Belum ada peringkat

- Trigonometry A Unit Circle Approach 10Th Edition Sullivan Test Bank Full Chapter PDFDokumen36 halamanTrigonometry A Unit Circle Approach 10Th Edition Sullivan Test Bank Full Chapter PDFerik.looney743100% (11)

- Foxchase Topo MapDokumen1 halamanFoxchase Topo MapJim DuncanBelum ada peringkat

- Crozet - Sales History and Comparison - 2013 V 2012Dokumen2 halamanCrozet - Sales History and Comparison - 2013 V 2012Jim DuncanBelum ada peringkat

- Dr. Yun PPT Feb 2014Dokumen41 halamanDr. Yun PPT Feb 2014Jim DuncanBelum ada peringkat

- Foxchase Landing Color PlatDokumen1 halamanFoxchase Landing Color PlatJim DuncanBelum ada peringkat

- Crozet - Year To Date Real Estate MarketDokumen1 halamanCrozet - Year To Date Real Estate MarketJim DuncanBelum ada peringkat

- Condos - Charlottesville MSA - 2Q 2013 Vs 2Q 2012Dokumen4 halamanCondos - Charlottesville MSA - 2Q 2013 Vs 2Q 2012Jim DuncanBelum ada peringkat

- Fardowners - Crozet Library DaysDokumen1 halamanFardowners - Crozet Library DaysJim DuncanBelum ada peringkat

- Foxchase Landing PlatDokumen1 halamanFoxchase Landing PlatJim DuncanBelum ada peringkat

- Crozet DEC03 Presentation 120-03-2013Dokumen18 halamanCrozet DEC03 Presentation 120-03-2013Jim DuncanBelum ada peringkat

- Tabor Presbyterian Church Is Hosting Camp Hanover, A Traveling Day Camp, June 17-21.Dokumen2 halamanTabor Presbyterian Church Is Hosting Camp Hanover, A Traveling Day Camp, June 17-21.Jim DuncanBelum ada peringkat

- AYLI Press ReleaseDokumen1 halamanAYLI Press ReleaseJim DuncanBelum ada peringkat

- Crozet - Market Comparison StatisticsDokumen1 halamanCrozet - Market Comparison StatisticsJim DuncanBelum ada peringkat

- Charlottesville Real Estate Market Report - 3Q 2013Dokumen7 halamanCharlottesville Real Estate Market Report - 3Q 2013Jim DuncanBelum ada peringkat

- Three Scenarios 5-16-13 Updated 5-24-13Dokumen72 halamanThree Scenarios 5-16-13 Updated 5-24-13Jim DuncanBelum ada peringkat

- Crozet TriathlonDokumen1 halamanCrozet TriathlonJim DuncanBelum ada peringkat

- Crozet UMC Is Hosting A Concert As A Fundraiser For The Crozet LibraryDokumen1 halamanCrozet UMC Is Hosting A Concert As A Fundraiser For The Crozet LibraryJim DuncanBelum ada peringkat

- 2012 Year End Charlottesville Real Estate Nest ReportDokumen9 halaman2012 Year End Charlottesville Real Estate Nest ReportJonathan KauffmannBelum ada peringkat

- Western Albemarle Camp FairDokumen1 halamanWestern Albemarle Camp FairJim DuncanBelum ada peringkat

- RAD Registration AnnouncementDokumen1 halamanRAD Registration AnnouncementJim DuncanBelum ada peringkat

- Charlottesville Nest Report Data SlidesDokumen6 halamanCharlottesville Nest Report Data SlidesJim DuncanBelum ada peringkat

- Art Fest in The WestDokumen1 halamanArt Fest in The WestJim DuncanBelum ada peringkat

- First Quarter 2013 Charlottesville Real Estate Market UpdateDokumen9 halamanFirst Quarter 2013 Charlottesville Real Estate Market UpdateJonathan KauffmannBelum ada peringkat

- Valentine Swing DanceDokumen1 halamanValentine Swing DanceJim DuncanBelum ada peringkat

- RAD Registration AnnouncementDokumen1 halamanRAD Registration AnnouncementJim DuncanBelum ada peringkat

- Peachtree Baseball 2013 RegistrationDokumen1 halamanPeachtree Baseball 2013 RegistrationJim DuncanBelum ada peringkat

- International Folk Dance Class at Tabor Church in CrozetDokumen1 halamanInternational Folk Dance Class at Tabor Church in CrozetJim DuncanBelum ada peringkat

- Crozet Park Master PlanDokumen1 halamanCrozet Park Master PlanJim DuncanBelum ada peringkat

- Nest Report: Charlottesville Area Real Estate Market Report Q3 2012Dokumen9 halamanNest Report: Charlottesville Area Real Estate Market Report Q3 2012Jonathan KauffmannBelum ada peringkat

- Charlottesville Real Estate Market Update: November 2012Dokumen2 halamanCharlottesville Real Estate Market Update: November 2012Jonathan KauffmannBelum ada peringkat

- Unisted States Air Force Langley Winds Ensemble - 11 October 2012 in Crozet, VirginiaDokumen1 halamanUnisted States Air Force Langley Winds Ensemble - 11 October 2012 in Crozet, VirginiaJim DuncanBelum ada peringkat

- Meeting Consumers ' Connectivity Needs: A Report From Frontier EconomicsDokumen74 halamanMeeting Consumers ' Connectivity Needs: A Report From Frontier EconomicsjkbuckwalterBelum ada peringkat

- E-Mobility - Ladestation - Charging Station in Thalham - Raspberry Pi OCPPDokumen8 halamanE-Mobility - Ladestation - Charging Station in Thalham - Raspberry Pi OCPPjpcmeBelum ada peringkat

- Action Plan for Integrated Waste Management in SaharanpurDokumen5 halamanAction Plan for Integrated Waste Management in SaharanpuramitBelum ada peringkat

- Chap1 HRM581 Oct Feb 2023Dokumen20 halamanChap1 HRM581 Oct Feb 2023liana bahaBelum ada peringkat

- Penyebaran Fahaman Bertentangan Akidah Islam Di Media Sosial Dari Perspektif Undang-Undang Dan Syariah Di MalaysiaDokumen12 halamanPenyebaran Fahaman Bertentangan Akidah Islam Di Media Sosial Dari Perspektif Undang-Undang Dan Syariah Di Malaysia2023225596Belum ada peringkat

- Case Study Format Hvco Srce UhvDokumen2 halamanCase Study Format Hvco Srce Uhvaayushjn290Belum ada peringkat

- Monitoring of SLM Distribution in Sta. Maria ElementaryDokumen3 halamanMonitoring of SLM Distribution in Sta. Maria ElementaryAnnalyn Gonzales ModeloBelum ada peringkat

- Class Xi BST Chapter 6. Social Resoposibility (Competency - Based Test Items) Marks WiseDokumen17 halamanClass Xi BST Chapter 6. Social Resoposibility (Competency - Based Test Items) Marks WiseNidhi ShahBelum ada peringkat

- How Zagreb's Socialist Experiment Finally Matured Long After Socialism - Failed ArchitectureDokumen12 halamanHow Zagreb's Socialist Experiment Finally Matured Long After Socialism - Failed ArchitectureAneta Mudronja PletenacBelum ada peringkat

- Cost of DebtDokumen3 halamanCost of DebtGonzalo De CorralBelum ada peringkat

- Pattaradday Festival: Celebrating Unity in Santiago City's HistoryDokumen16 halamanPattaradday Festival: Celebrating Unity in Santiago City's HistoryJonathan TolentinoBelum ada peringkat

- Capital Fixed & Working - New SyllabusDokumen6 halamanCapital Fixed & Working - New SyllabusNaaz AliBelum ada peringkat

- DEALCO FARMS vs. NLRCDokumen14 halamanDEALCO FARMS vs. NLRCGave ArcillaBelum ada peringkat

- Censorship Is Always Self Defeating and Therefore FutileDokumen2 halamanCensorship Is Always Self Defeating and Therefore Futileqwert2526Belum ada peringkat

- 50 Simple Interest Problems With SolutionsDokumen46 halaman50 Simple Interest Problems With SolutionsArnel MedinaBelum ada peringkat

- List of Universities in Tamil Nadu1Dokumen7 halamanList of Universities in Tamil Nadu1RCAS IICBelum ada peringkat

- MUN Resolution For The North Korean Missile CrisisDokumen2 halamanMUN Resolution For The North Korean Missile CrisissujalachamBelum ada peringkat

- Pub. 127 East Coast of Australia and New Zealand 10ed 2010Dokumen323 halamanPub. 127 East Coast of Australia and New Zealand 10ed 2010joop12Belum ada peringkat

- Personal Values: Definitions & TypesDokumen1 halamanPersonal Values: Definitions & TypesGermaeGonzalesBelum ada peringkat

- An Introduction To TeluguDokumen5 halamanAn Introduction To TeluguAnonymous 86cyUE2Belum ada peringkat

- The Princess AhmadeeDokumen6 halamanThe Princess AhmadeeAnnette EdwardsBelum ada peringkat

- Sabbia Food MenuDokumen2 halamanSabbia Food MenuNell CaseyBelum ada peringkat

- Student Majoriti Planing After GrdaduationDokumen13 halamanStudent Majoriti Planing After GrdaduationShafizahNurBelum ada peringkat

- Exploratory EssayDokumen9 halamanExploratory Essayapi-237899225Belum ada peringkat

- Fe en Accion - Morris VendenDokumen734 halamanFe en Accion - Morris VendenNicolas BertoaBelum ada peringkat

- True or FalseDokumen3 halamanTrue or FalseRB AbacaBelum ada peringkat

- Agreement InvestmentDokumen5 halamanAgreement InvestmentEricka Kim100% (6)

- ChildBook Mother Is Gold Father Is Glass Gender An - Lorelle D Semley PDFDokumen257 halamanChildBook Mother Is Gold Father Is Glass Gender An - Lorelle D Semley PDFTristan Pan100% (1)

- MTWD HistoryDokumen8 halamanMTWD HistoryVernie SaluconBelum ada peringkat

- Đề thi tuyển sinh vào lớp 10 năm 2018 - 2019 môn Tiếng Anh - Sở GD&ĐT An GiangDokumen5 halamanĐề thi tuyển sinh vào lớp 10 năm 2018 - 2019 môn Tiếng Anh - Sở GD&ĐT An GiangHaiBelum ada peringkat