Anda mungkin juga menyukai

- Long-Term Construction ContractsDokumen12 halamanLong-Term Construction Contractsblackphoenix303Belum ada peringkat

- Derivatives & PPEDokumen7 halamanDerivatives & PPEblackphoenix303Belum ada peringkat

- BL CompilationDokumen48 halamanBL Compilationblackphoenix303100% (3)

- Risk Audit PlanDokumen6 halamanRisk Audit Planblackphoenix3030% (1)

- Auditing TheoryDokumen5 halamanAuditing Theoryblackphoenix303Belum ada peringkat

- 08 MarchewkaDokumen57 halaman08 Marchewkablackphoenix303Belum ada peringkat

- Mosquito CoilDokumen2 halamanMosquito Coilblackphoenix303Belum ada peringkat

- Auditing TheoryDokumen5 halamanAuditing Theoryblackphoenix303Belum ada peringkat

- 3words 8letters BoomDokumen1.043 halaman3words 8letters Boomblackphoenix303Belum ada peringkat

- Filipino Contemporary WritersDokumen10 halamanFilipino Contemporary WritersLRB67% (6)

- NIL - Discharge Cases Negotiable InstrumentsDokumen8 halamanNIL - Discharge Cases Negotiable Instrumentsblackphoenix303Belum ada peringkat

- Chapter 15: Controlling Computer-Based Accounting Information System Information Systems, Part I 3 Edition James HallDokumen5 halamanChapter 15: Controlling Computer-Based Accounting Information System Information Systems, Part I 3 Edition James Hallblackphoenix303Belum ada peringkat

- Accounting Alert SEC Amended SRC Rule 68Dokumen10 halamanAccounting Alert SEC Amended SRC Rule 68blackphoenix303Belum ada peringkat

- Capital BudgetingDokumen6 halamanCapital Budgetingblackphoenix303Belum ada peringkat

- Income TaxationDokumen32 halamanIncome Taxationblackphoenix303Belum ada peringkat

- Outsourcing in The PhilippinesDokumen32 halamanOutsourcing in The Philippinesblackphoenix303Belum ada peringkat

- Negotiable Instruments - Alteration CasesDokumen17 halamanNegotiable Instruments - Alteration Casesblackphoenix303Belum ada peringkat

- Sales ReviewerDokumen29 halamanSales ReviewerHoward Chan95% (21)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Acc 109 - P2 Quiz Revenue Recognition and Non Current Assets Held For SaleDokumen7 halamanAcc 109 - P2 Quiz Revenue Recognition and Non Current Assets Held For SaleRosemarie Villanueva89% (9)

- 1 Valuation Exercise Fall 2020 1Dokumen3 halaman1 Valuation Exercise Fall 2020 1Elizabeth PGBelum ada peringkat

- Gel Cash FlowDokumen3 halamanGel Cash Flowravibhartia1978Belum ada peringkat

- Ratio Analysis and Comparison of Two CompaniesDokumen28 halamanRatio Analysis and Comparison of Two Companiesmadhu hotwaniBelum ada peringkat

- Summary of New CF 2018Dokumen23 halamanSummary of New CF 2018Ashraf Uz ZamanBelum ada peringkat

- The Cpa Licensure Examination Syllabus Management Services Effective October 2022 ExaminationDokumen3 halamanThe Cpa Licensure Examination Syllabus Management Services Effective October 2022 ExaminationMarc Anthony Max MagbalonBelum ada peringkat

- 3.2. Finance 1 Quiz On Horizontal VerticalDokumen3 halaman3.2. Finance 1 Quiz On Horizontal VerticalZham JavierBelum ada peringkat

- Stock Valuation - Financial ManagementDokumen10 halamanStock Valuation - Financial ManagementNoelia Mc DonaldBelum ada peringkat

- Analisis Fundamental WikaDokumen5 halamanAnalisis Fundamental WikaAnonymous XoUqrqyuBelum ada peringkat

- Sale of Partnership To A Limited CompanyDokumen5 halamanSale of Partnership To A Limited CompanyRonel Buhay100% (1)

- Finance Applications and Theory 4Th Edition Cornett Solutions Manual Full Chapter PDFDokumen42 halamanFinance Applications and Theory 4Th Edition Cornett Solutions Manual Full Chapter PDFheulwenvalerie7dr100% (12)

- ReceivablesDokumen12 halamanReceivablesRizalene AgustinBelum ada peringkat

- Mutual Funds Correction PDFDokumen48 halamanMutual Funds Correction PDFPrethesh JainBelum ada peringkat

- Chapter 11 International AccountingDokumen25 halamanChapter 11 International AccountingMuneera Al HassanBelum ada peringkat

- Working: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000Dokumen8 halamanWorking: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000kudkhanBelum ada peringkat

- Fixed Asset Register SampleDokumen55 halamanFixed Asset Register SampleClarisse30Belum ada peringkat

- Thoughtful Investors Excel ScreenerDokumen21 halamanThoughtful Investors Excel ScreenermattanurmunnaBelum ada peringkat

- IAS 32 - Part C - Basis For ConclusionsDokumen34 halamanIAS 32 - Part C - Basis For ConclusionssachaaabgrallBelum ada peringkat

- Module 1 PDFDokumen21 halamanModule 1 PDFIj Ilarde50% (2)

- MKT1506-Individual AssignmentDokumen22 halamanMKT1506-Individual AssignmentBảo TrânBelum ada peringkat

- CA01 VariableCostingFDokumen114 halamanCA01 VariableCostingFVenise BaliaBelum ada peringkat

- Practice ques-CVP AnalysisDokumen5 halamanPractice ques-CVP AnalysisSuchita GaonkarBelum ada peringkat

- 1st Year Class - Depreciation - EditedDokumen60 halaman1st Year Class - Depreciation - EditedAnkit Patnaik67% (3)

- Tanauan Institute, Inc.: Adjusting EntriesDokumen8 halamanTanauan Institute, Inc.: Adjusting EntriesHanna CaraigBelum ada peringkat

- Statement of Changes in Equity MCQDokumen4 halamanStatement of Changes in Equity MCQMia CatanBelum ada peringkat

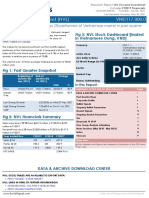

- No Va Land Investment (NVL) VND117,000.0: Fig 3: NVL Stock Dashboard (Traded in Vietnamese Dong, VND)Dokumen27 halamanNo Va Land Investment (NVL) VND117,000.0: Fig 3: NVL Stock Dashboard (Traded in Vietnamese Dong, VND)DIDIBelum ada peringkat

- 10 Managing Economics of Scale in A Supply Chain - Cycle InventoryDokumen25 halaman10 Managing Economics of Scale in A Supply Chain - Cycle InventoryWei JunBelum ada peringkat

- LK Juni 2017 Unaudited PDFDokumen210 halamanLK Juni 2017 Unaudited PDFnandiwardhana aryagunaBelum ada peringkat

- WACCDokumen7 halamanWACCAndre IndoBelum ada peringkat

- Advanced Financial ReportingDokumen6 halamanAdvanced Financial ReportingRobin G'koolBelum ada peringkat