Anda mungkin juga menyukai

- Innovations in Portland Cement ManufacturingDokumen2 halamanInnovations in Portland Cement ManufacturingGiequatBelum ada peringkat

- Emission Reduction CalculationsDokumen51 halamanEmission Reduction CalculationsUmair UddinBelum ada peringkat

- TheCementPlantOperations B PDFDokumen32 halamanTheCementPlantOperations B PDFUmair UddinBelum ada peringkat

- Problem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Dokumen20 halamanProblem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Umair UddinBelum ada peringkat

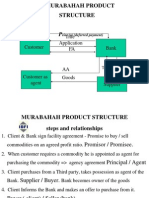

- MURABAHAH PRODUCT TITLEDokumen26 halamanMURABAHAH PRODUCT TITLEUmair UddinBelum ada peringkat

- Du Annual Report English LR 160314 12.00Dokumen44 halamanDu Annual Report English LR 160314 12.00Umair UddinBelum ada peringkat

- Pakistan AnnexuresDokumen8 halamanPakistan AnnexuresUmair UddinBelum ada peringkat

- Problem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Dokumen20 halamanProblem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Umair UddinBelum ada peringkat

- Pakistan-US-IMF Relations and Dutch DiseaseDokumen23 halamanPakistan-US-IMF Relations and Dutch DiseaseUmair UddinBelum ada peringkat

- The IMF and Pakistan Seminar PIDE ExpansionDokumen19 halamanThe IMF and Pakistan Seminar PIDE ExpansionUmair UddinBelum ada peringkat

- InterviewsDokumen13 halamanInterviewsUmair UddinBelum ada peringkat

- Chi Square Test For IndependeceDokumen40 halamanChi Square Test For IndependeceNaman Bansal100% (1)

- Lab5 SPSS ChiSquareDokumen14 halamanLab5 SPSS ChiSquareUmair UddinBelum ada peringkat

- Al-Faysal Bank LTDDokumen44 halamanAl-Faysal Bank LTDqalander abbasBelum ada peringkat

- Pub Blic D Debt: CH Apter 9Dokumen21 halamanPub Blic D Debt: CH Apter 9Umair UddinBelum ada peringkat

- Kinds of ContractsDokumen10 halamanKinds of ContractsUmair UddinBelum ada peringkat

- Discharge of ContractDokumen14 halamanDischarge of ContractherhamBelum ada peringkat

- Tax ExpenditureDokumen3 halamanTax ExpenditureUmair UddinBelum ada peringkat

- Schiffman CB10 PPT 05Dokumen55 halamanSchiffman CB10 PPT 05Syed Wahaj100% (1)

- Chapter 1 - HRM - Introduction To HRM 120609Dokumen64 halamanChapter 1 - HRM - Introduction To HRM 120609Umair UddinBelum ada peringkat

- IcIDokumen39 halamanIcIUmair UddinBelum ada peringkat

- IcIDokumen39 halamanIcIUmair UddinBelum ada peringkat

- How To Develop Presentation SkillsDokumen29 halamanHow To Develop Presentation Skillsppinku0003100% (1)

- Chemical Resistance of PlasticsDokumen4 halamanChemical Resistance of PlasticsUmair UddinBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- VOC To CTQ Conversion SampleDokumen5 halamanVOC To CTQ Conversion SampleshivaprasadmvitBelum ada peringkat

- Group12 - Section C - HRM - Wrapitup PDFDokumen8 halamanGroup12 - Section C - HRM - Wrapitup PDFAMITESH RANJANBelum ada peringkat

- Dungca, Jomyro Atadero: ObjectiveDokumen3 halamanDungca, Jomyro Atadero: ObjectiveJomyro DungcaBelum ada peringkat

- Manufacturing Accounts NotesDokumen9 halamanManufacturing Accounts NotesFegason FegyBelum ada peringkat

- MGNT 3430 Homework Answers for Operations ManagementDokumen4 halamanMGNT 3430 Homework Answers for Operations ManagementKeron TzulBelum ada peringkat

- MGL Economics Chapter 2Dokumen41 halamanMGL Economics Chapter 2jannat_sondiBelum ada peringkat

- Customer Relationship Management ROIDokumen19 halamanCustomer Relationship Management ROIHồng PhúcBelum ada peringkat

- G1 6.2 Partnership - ReconstitutionDokumen55 halamanG1 6.2 Partnership - Reconstitutionsridhartks100% (1)

- Project Report - CG - Urvashi SharmaDokumen73 halamanProject Report - CG - Urvashi SharmacomplianceBelum ada peringkat

- Acctg201 Support Cost Department AllocationDokumen3 halamanAcctg201 Support Cost Department AllocationEab RondinaBelum ada peringkat

- A Study On Customer Satifaction Towards FlipkartDokumen5 halamanA Study On Customer Satifaction Towards FlipkartDulcet LyricsBelum ada peringkat

- Marketing For DemographicDokumen7 halamanMarketing For DemographicSujit Kumar SahooBelum ada peringkat

- Given The P&L and Balance Sheet Assumptions, Calculate The FollowingDokumen37 halamanGiven The P&L and Balance Sheet Assumptions, Calculate The FollowingvaishaliBelum ada peringkat

- Solutions 11 18Dokumen7 halamanSolutions 11 18Ariel LusaresBelum ada peringkat

- ITC Rajputana ReportDokumen34 halamanITC Rajputana ReportArjun RathoreBelum ada peringkat

- mcq1 PDFDokumen15 halamanmcq1 PDFjack100% (1)

- DHL Supply Chain Market Leader in Contract LogisticsDokumen2 halamanDHL Supply Chain Market Leader in Contract LogisticsJindalBelum ada peringkat

- 0452 s07 QP 3 PDFDokumen20 halaman0452 s07 QP 3 PDFAbirHudaBelum ada peringkat

- Academic Module 4.0 Entrep. Management Sec - Sem. Ay 2022 2023Dokumen23 halamanAcademic Module 4.0 Entrep. Management Sec - Sem. Ay 2022 2023Daniela Nicole Manibog ValentinoBelum ada peringkat

- Supply Chain Management: SESSION 21& 23Dokumen54 halamanSupply Chain Management: SESSION 21& 23DYPUSM WECBelum ada peringkat

- Joint Venture - Practice ProblemsDokumen9 halamanJoint Venture - Practice ProblemsrnbharathirajaBelum ada peringkat

- Strategic AnalysisDokumen6 halamanStrategic AnalysisShrestha KishorBelum ada peringkat

- June 2021 Question Paper 11Dokumen12 halamanJune 2021 Question Paper 11lydia.cBelum ada peringkat

- Finace in Business ReDokumen20 halamanFinace in Business ReGauri SidharthBelum ada peringkat

- Weight Watchers Business Plan 2019Dokumen71 halamanWeight Watchers Business Plan 2019mhetfield100% (1)

- BLUE WATER Business & Operation Plan Financial Projections SummaryDokumen67 halamanBLUE WATER Business & Operation Plan Financial Projections SummaryAly Khalaf80% (5)

- Sip-PresentationDokumen12 halamanSip-PresentationBharadwaja JoshiBelum ada peringkat

- Crocs Case StudyDokumen18 halamanCrocs Case StudyAndrea BonfantiBelum ada peringkat

- Quiz on Target Costing and Activity-Based ManagementDokumen3 halamanQuiz on Target Costing and Activity-Based ManagementDeelan AppaBelum ada peringkat

- Retail Drug Store Financial Analysis and Audit RisksDokumen9 halamanRetail Drug Store Financial Analysis and Audit RisksNeLson ALcanarBelum ada peringkat