Anda mungkin juga menyukai

- Financial Risk Management: A Simple IntroductionDari EverandFinancial Risk Management: A Simple IntroductionPenilaian: 4.5 dari 5 bintang4.5/5 (7)

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2Dari EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2Belum ada peringkat

- Lecture 5312312Dokumen55 halamanLecture 5312312Tam Chun LamBelum ada peringkat

- 10 InclassDokumen50 halaman10 InclassTBelum ada peringkat

- 2268Dokumen43 halaman2268asmaBelum ada peringkat

- Bond Price VolatilityDokumen63 halamanBond Price VolatilityJithesh JanardhananBelum ada peringkat

- Bond Valuation: Case: Atlas InvestmentsDokumen853 halamanBond Valuation: Case: Atlas Investmentsjk kumarBelum ada peringkat

- Unit 3 - Term Structure of Interest Rates Slides 2022Dokumen53 halamanUnit 3 - Term Structure of Interest Rates Slides 2022ndonithando2207Belum ada peringkat

- Understanding the Yield CurveDokumen14 halamanUnderstanding the Yield CurveAmirBelum ada peringkat

- Managing Interest Rate RiskDokumen32 halamanManaging Interest Rate RiskHenry So E Diarko100% (1)

- Duration & ConvexityDokumen18 halamanDuration & ConvexityHrishikesh Malu100% (3)

- Bond Prices and Yields: Mcgraw-Hill/IrwinDokumen47 halamanBond Prices and Yields: Mcgraw-Hill/IrwinAboAdham100100Belum ada peringkat

- Duration: Measuring Interest Rate SensitivityDokumen19 halamanDuration: Measuring Interest Rate SensitivityALBelum ada peringkat

- BondsDokumen26 halamanBondsPranav SanturkarBelum ada peringkat

- Bond Price Volatility: Dr. Himanshu Joshi FORE School of Management New DelhiDokumen51 halamanBond Price Volatility: Dr. Himanshu Joshi FORE School of Management New Delhiashishbansal85Belum ada peringkat

- The Structure of Interest RatesDokumen72 halamanThe Structure of Interest RatesMarwa HassanBelum ada peringkat

- Bond Prices and Yields: Mcgraw-Hill/IrwinDokumen24 halamanBond Prices and Yields: Mcgraw-Hill/IrwinAshutosh KalraBelum ada peringkat

- Valuation of Bonds and SharesDokumen45 halamanValuation of Bonds and SharessmsmbaBelum ada peringkat

- Bond RiskDokumen31 halamanBond RiskSophia ChouBelum ada peringkat

- The Duration MeasureDokumen38 halamanThe Duration MeasureKatrina Vianca DecapiaBelum ada peringkat

- Chapter Five: Interest Rate Determination and Bond ValuationDokumen38 halamanChapter Five: Interest Rate Determination and Bond ValuationMikias DegwaleBelum ada peringkat

- Investment Analysis and Portfolio Management: Lecture 6 Part 2Dokumen35 halamanInvestment Analysis and Portfolio Management: Lecture 6 Part 2jovvy24Belum ada peringkat

- Bond Prices Yields FundamentalsDokumen40 halamanBond Prices Yields FundamentalssaysuuBelum ada peringkat

- UntitledDokumen29 halamanUntitledDEEPIKA S R BUSINESS AND MANAGEMENT (BGR)Belum ada peringkat

- Bond ValuationDokumen57 halamanBond ValuationRajib BurmanBelum ada peringkat

- Intermediate Finance Session 9 Chapter 18 Key ConceptsDokumen56 halamanIntermediate Finance Session 9 Chapter 18 Key ConceptsrizaunBelum ada peringkat

- FINA5520 Risk Management and Interest RatesDokumen46 halamanFINA5520 Risk Management and Interest RatesthelittlebirdyBelum ada peringkat

- Bonds DurationDokumen31 halamanBonds DurationAashima GroverBelum ada peringkat

- Valuation and Factors Affecting Bonds and SharesDokumen71 halamanValuation and Factors Affecting Bonds and SharesRubal GargBelum ada peringkat

- BondsDokumen55 halamanBondsfecaxeyivuBelum ada peringkat

- Valuation of Securities: Key ConceptsDokumen53 halamanValuation of Securities: Key ConceptsKshitishBelum ada peringkat

- BOND VALUATION Week 4Dokumen43 halamanBOND VALUATION Week 4desblahBelum ada peringkat

- F303 - Intermediate Investments: Interest Rate Sensitivity and Bond DurationDokumen19 halamanF303 - Intermediate Investments: Interest Rate Sensitivity and Bond Durationhussain_nBelum ada peringkat

- Duration PDFDokumen8 halamanDuration PDFMohammad Khaled Saifullah CdcsBelum ada peringkat

- Lec 10Dokumen26 halamanLec 10danphamm226Belum ada peringkat

- Term Structure of Interest RatesDokumen44 halamanTerm Structure of Interest RatesmasatiBelum ada peringkat

- Introduction To Bond ValuationDokumen24 halamanIntroduction To Bond ValuationVarun SinghBelum ada peringkat

- Lecture 3Dokumen29 halamanLecture 3Nurfaiqah AmniBelum ada peringkat

- 4 - Term Structures TheoriesDokumen15 halaman4 - Term Structures Theoriesmajmmallikarachchi.mallikarachchiBelum ada peringkat

- IcrddcDokumen7 halamanIcrddcapi-213789026Belum ada peringkat

- Chapter Three Interest Rates in The Financial SystemDokumen40 halamanChapter Three Interest Rates in The Financial SystemKalkayeBelum ada peringkat

- Duration Convexity Bond Portfolio ManagementDokumen49 halamanDuration Convexity Bond Portfolio ManagementParijatVikramSingh100% (1)

- Bond valuation and yield analysisDokumen35 halamanBond valuation and yield analysisTanmay MehtaBelum ada peringkat

- Third Party Issuer: ABS Vs MBS When You Invest in Mortgage-Backed (MBS) and Asset-Backed (ABS) Securities You AreDokumen4 halamanThird Party Issuer: ABS Vs MBS When You Invest in Mortgage-Backed (MBS) and Asset-Backed (ABS) Securities You AreElla Marie WicoBelum ada peringkat

- Use Duration and Convexity To Measure RiskDokumen4 halamanUse Duration and Convexity To Measure RiskSreenesh PaiBelum ada peringkat

- Term Structure of Interest RatesDokumen21 halamanTerm Structure of Interest RatestoabhishekpalBelum ada peringkat

- Bond TheoremDokumen27 halamanBond TheoremparulkakBelum ada peringkat

- Interest Rate TutorialsDokumen81 halamanInterest Rate TutorialsdvobqvpigpwzcfvsgdBelum ada peringkat

- Bond Portfolio Management StrategiesDokumen36 halamanBond Portfolio Management StrategiesMuhammad HarisBelum ada peringkat

- Riding The Yield Curve 1663880194Dokumen81 halamanRiding The Yield Curve 1663880194Daniel PeñaBelum ada peringkat

- Understanding Bond Price VolatilityDokumen37 halamanUnderstanding Bond Price VolatilityHarpreetBelum ada peringkat

- 14 Fixed Income Portfolio ManagementDokumen60 halaman14 Fixed Income Portfolio ManagementPawan ChoudharyBelum ada peringkat

- Chapter 1 Overview of Debt SecuritiesDokumen64 halamanChapter 1 Overview of Debt SecuritiesHồng Nhung PhạmBelum ada peringkat

- Financial Management - Bonds 2014Dokumen34 halamanFinancial Management - Bonds 2014Joe ChungBelum ada peringkat

- DurationDokumen5 halamanDurationNiño Rey LopezBelum ada peringkat

- Valuation of BondsDokumen91 halamanValuation of BondsraymondBelum ada peringkat

- Bond Duration 2Dokumen9 halamanBond Duration 2Mian Qamar Ul ZamanBelum ada peringkat

- Bonds Overview Pricing YieldDokumen40 halamanBonds Overview Pricing YieldRajesh Chowdary ChintamaneniBelum ada peringkat

- High-Q Financial Basics. Skills & Knowlwdge for Today's manDari EverandHigh-Q Financial Basics. Skills & Knowlwdge for Today's manBelum ada peringkat

- Chapter 4 Supplement Process Costing Using The FIFO Method: True/FalseDokumen38 halamanChapter 4 Supplement Process Costing Using The FIFO Method: True/FalseRashedul Islam PaponBelum ada peringkat

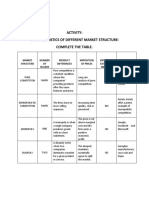

- Characteristics of Different Market Structures TableDokumen2 halamanCharacteristics of Different Market Structures TableJustine PadohilaoBelum ada peringkat

- Yap Ke Huat & Ors V Pembangunan Warisan MurniDokumen16 halamanYap Ke Huat & Ors V Pembangunan Warisan MurniZawani RahimBelum ada peringkat

- ABNT NBR 6330 2020 - General Purpose Carbon Steel Wire RodDokumen12 halamanABNT NBR 6330 2020 - General Purpose Carbon Steel Wire RodElton Felipe Gularte dos SantosBelum ada peringkat

- OfferLetter SignedDokumen19 halamanOfferLetter SignedNalin bhattBelum ada peringkat

- Ablockers Fitness 101Dokumen10 halamanAblockers Fitness 101iqbal kamilBelum ada peringkat

- Qdoc - Tips - Kunci Jawaban Supply Chain Management Presales SpeDokumen19 halamanQdoc - Tips - Kunci Jawaban Supply Chain Management Presales SpeEyuBelum ada peringkat

- Master The Data: An Introduction To Accounting Data: A Look BackDokumen81 halamanMaster The Data: An Introduction To Accounting Data: A Look Backsalsabila.rafy-2021Belum ada peringkat

- FA Work BookDokumen59 halamanFA Work BookUnais AhmedBelum ada peringkat

- Sps Agner v. BPIDokumen2 halamanSps Agner v. BPIKarla Lois de GuzmanBelum ada peringkat

- Maruti suzuki Ambal Auto ExperienceDokumen26 halamanMaruti suzuki Ambal Auto Experience18UGCP078 SUJITHBelum ada peringkat

- Ac 418 Group AssignmentDokumen6 halamanAc 418 Group AssignmentJacob PossibilityBelum ada peringkat

- Business DirectoryDokumen4 halamanBusiness DirectoryRegunathan PadmanathanBelum ada peringkat

- Chapter 3 PlanningDokumen29 halamanChapter 3 PlanningDagm alemayehuBelum ada peringkat

- Welder Job Clearance Card for Ali QurbanDokumen43 halamanWelder Job Clearance Card for Ali QurbanDhanush NairBelum ada peringkat

- Catalog Central Parts Warehouse Plow Parts 2018 - 19Dokumen132 halamanCatalog Central Parts Warehouse Plow Parts 2018 - 19BillBelum ada peringkat

- Busm4696 Political Economy of International Business Cover SheetDokumen14 halamanBusm4696 Political Economy of International Business Cover SheetThuỳ Dung0% (1)

- Blue Danube Si Green HydrobenDokumen11 halamanBlue Danube Si Green HydrobenDiana AchimescuBelum ada peringkat

- Organizing Global Marketing ProgramsDokumen19 halamanOrganizing Global Marketing ProgramsSabin ShresthaBelum ada peringkat

- GN Cement Industry 05022021 RevDokumen97 halamanGN Cement Industry 05022021 RevNetaji Dasari100% (1)

- KohlerDokumen25 halamanKohlertousif AhmedBelum ada peringkat

- s3879661 A1 Slides mktg1420-1Dokumen15 halamans3879661 A1 Slides mktg1420-1Huy Quang100% (1)

- Onondaga County 2021 BudgetDokumen424 halamanOnondaga County 2021 BudgetNewsChannel 9Belum ada peringkat

- Economics Assignment IDokumen2 halamanEconomics Assignment IDEVASISHBelum ada peringkat

- Income Statement 2014 2015: 3. Net Revenue 5. Gross ProfitDokumen71 halamanIncome Statement 2014 2015: 3. Net Revenue 5. Gross ProfitThu ThuBelum ada peringkat

- Excel calendarDokumen28 halamanExcel calendarThanh LêBelum ada peringkat

- Prosthetid Hand Pugh MethodDokumen91 halamanProsthetid Hand Pugh MethodFaddhila FadhilaBelum ada peringkat

- BCIF - Ver7 Back With SignatureDokumen1 halamanBCIF - Ver7 Back With SignatureKatrina JarabejoBelum ada peringkat

- Esemen AsrsDokumen25 halamanEsemen AsrsAtiqah Binti Abu HassanBelum ada peringkat

- Financial Accounting CH 2Dokumen12 halamanFinancial Accounting CH 2Karim KhaledBelum ada peringkat