Anda mungkin juga menyukai

- Management Accounting and The Business EnvironmentDokumen36 halamanManagement Accounting and The Business EnvironmentArmi Niña Bacho RoselBelum ada peringkat

- 20089ipcc Paper7B Vol2 Cp7Dokumen19 halaman20089ipcc Paper7B Vol2 Cp7Piyush GambaniBelum ada peringkat

- Cost ManagementDokumen41 halamanCost Managementsuperdole83Belum ada peringkat

- 26managing Accounting in A Changing EnvironmentDokumen60 halaman26managing Accounting in A Changing EnvironmentJolianne SalvadoOfc0% (1)

- Module 3 - Strategic Cost ManagementDokumen7 halamanModule 3 - Strategic Cost ManagementFrancis Ryan PorquezBelum ada peringkat

- Chapter 26 Managing Accounting in A Changing Environment: EssayDokumen68 halamanChapter 26 Managing Accounting in A Changing Environment: Essayjanine0% (1)

- Operations ManagementDokumen20 halamanOperations Managementamna61529Belum ada peringkat

- Operations Management Summary Reviewer Chapter 1 To 3Dokumen6 halamanOperations Management Summary Reviewer Chapter 1 To 3Ralph AbutinBelum ada peringkat

- Balanced Scorecard: The BS PhilosophyDokumen6 halamanBalanced Scorecard: The BS PhilosophyFarBelum ada peringkat

- Materials ManagementDokumen41 halamanMaterials ManagementManohar Gupta100% (1)

- AE 27 Lesson 2Dokumen36 halamanAE 27 Lesson 2Ces GarceraBelum ada peringkat

- Best Practices & Benchmarking (Compatibility Mode) PDFDokumen34 halamanBest Practices & Benchmarking (Compatibility Mode) PDFvkvivekvk1Belum ada peringkat

- Chapter 2 ManACDokumen7 halamanChapter 2 ManACRizza Mae RaferBelum ada peringkat

- Balanced Score Card:: Performance ManagementDokumen4 halamanBalanced Score Card:: Performance Managementtappu0410Belum ada peringkat

- Changes in The Business EnvironmentDokumen30 halamanChanges in The Business EnvironmentAbdulmajed Unda MimbantasBelum ada peringkat

- Reaching Strategic EdgeDokumen14 halamanReaching Strategic EdgeVivek ReddyBelum ada peringkat

- CHAPTER 2 and 3 MANAGEMENT ACCOUNTINGDokumen14 halamanCHAPTER 2 and 3 MANAGEMENT ACCOUNTINGMae Ann RaquinBelum ada peringkat

- IT Notes Old SyllabusDokumen51 halamanIT Notes Old SyllabusDhivyaBelum ada peringkat

- Assignment 1 - Darshan BhavsarDokumen5 halamanAssignment 1 - Darshan BhavsarDarshan BhavsarBelum ada peringkat

- CSP - SM - Strategic EdgeDokumen14 halamanCSP - SM - Strategic EdgeDhun ChhawchhariaBelum ada peringkat

- Operations Management LESSON MIDTERM AutoRecoveredDokumen23 halamanOperations Management LESSON MIDTERM AutoRecoveredKrisha Ann TabanaoBelum ada peringkat

- QM 0010Dokumen20 halamanQM 0010Hariharan RajaramanBelum ada peringkat

- Preparation Answers - TQMDokumen12 halamanPreparation Answers - TQMKosal ThunBelum ada peringkat

- AE 27 Lesson 2Dokumen37 halamanAE 27 Lesson 2MARC BENNETH BERIÑABelum ada peringkat

- A. Total Quality ManagementDokumen11 halamanA. Total Quality ManagementNhan Thien NhuBelum ada peringkat

- Workshop 1 - BMG706 Overview & Important of Operations and Quality MGMT - JLSS 2022Dokumen26 halamanWorkshop 1 - BMG706 Overview & Important of Operations and Quality MGMT - JLSS 2022Hương Ly LêBelum ada peringkat

- SM Chapter 7 DefinitionsDokumen2 halamanSM Chapter 7 DefinitionsSelva GaneshBelum ada peringkat

- Process Management e Book PDFDokumen25 halamanProcess Management e Book PDFmorozco1965Belum ada peringkat

- Business Process Reengineering Faculty-Avadhesh GuptaDokumen43 halamanBusiness Process Reengineering Faculty-Avadhesh GuptaskusonuBelum ada peringkat

- Stratigic Cost Management ReportDokumen30 halamanStratigic Cost Management ReportKhing Dragon ManlangitBelum ada peringkat

- Process Management: P I R Z A D ADokumen27 halamanProcess Management: P I R Z A D ARaja Awais LiaqautBelum ada peringkat

- Business Process ReengineeringDokumen49 halamanBusiness Process ReengineeringSohaib AkhtarBelum ada peringkat

- TQM Final Presentation Rutir & GroupDokumen31 halamanTQM Final Presentation Rutir & GroupVishal NalamwadBelum ada peringkat

- Quality and Business Process ReDokumen19 halamanQuality and Business Process ReasvanmalindiBelum ada peringkat

- Section 5-35 (Domain 3) : Quality PrinciplesDokumen8 halamanSection 5-35 (Domain 3) : Quality Principlesapi-3828205Belum ada peringkat

- CTEA 3227 Management Accounting III Topic 7 Performance Management Systems 2 (Contemporary Approach)Dokumen36 halamanCTEA 3227 Management Accounting III Topic 7 Performance Management Systems 2 (Contemporary Approach)Nero ShaBelum ada peringkat

- المحاضرة الثانيةDokumen20 halamanالمحاضرة الثانيةa.abdeewi99Belum ada peringkat

- ACTIVITIESDokumen2 halamanACTIVITIESJhen-Jhen Geol-oh BaclasBelum ada peringkat

- Picpa - Managing CostDokumen138 halamanPicpa - Managing CostRodel Ryan YanaBelum ada peringkat

- Chapter 5 - Process FocusDokumen11 halamanChapter 5 - Process FocusShaina Trish TaguiamBelum ada peringkat

- Strategic Cost Management 2Dokumen19 halamanStrategic Cost Management 2mariyaBelum ada peringkat

- Core Processes in TQMDokumen5 halamanCore Processes in TQMĐiền Lê GiaBelum ada peringkat

- Balanced ScorecardDokumen22 halamanBalanced Scorecardshreyas_1392100% (1)

- BudgetingDokumen6 halamanBudgetingHasnat AsifBelum ada peringkat

- Process ManagementDokumen30 halamanProcess ManagementPARVEENBelum ada peringkat

- Cost Audit Strategies: A Business Costing ApproachDokumen15 halamanCost Audit Strategies: A Business Costing Approachasiwishtodo gmail comBelum ada peringkat

- Total Quality in Supply Chain Management Cat 4.2Dokumen15 halamanTotal Quality in Supply Chain Management Cat 4.2Hashi MohamedBelum ada peringkat

- Iso 9001Dokumen11 halamanIso 9001Thiyaga RajanBelum ada peringkat

- Total Quality Management-HrsDokumen9 halamanTotal Quality Management-HrsNehaBelum ada peringkat

- SUB: Production and Operation ManagementDokumen6 halamanSUB: Production and Operation ManagementMd. Roukon UddinBelum ada peringkat

- Management Accounting Chapter 1Dokumen4 halamanManagement Accounting Chapter 1Ieda ShaharBelum ada peringkat

- Module 1 Notes - 18ME734.Dokumen17 halamanModule 1 Notes - 18ME734.SANTOSH0% (1)

- Management Control Is The Process by Which Managers Influence OtherDokumen21 halamanManagement Control Is The Process by Which Managers Influence OtherFernandes RudolfBelum ada peringkat

- Techniques Under Development in Managerial AccountingDokumen27 halamanTechniques Under Development in Managerial AccountingMostafa MahmoudBelum ada peringkat

- BAHRIA UNIVERSITY, (Karachi Campus) : Department of Software EngineeringDokumen8 halamanBAHRIA UNIVERSITY, (Karachi Campus) : Department of Software Engineeringshariqa tahirBelum ada peringkat

- AF313 Lecture 2.1 Strategic Management AccountingDokumen28 halamanAF313 Lecture 2.1 Strategic Management Accountings11186706Belum ada peringkat

- Financial and Management Accounting: Basic FeaturesDokumen12 halamanFinancial and Management Accounting: Basic FeaturesMahediBelum ada peringkat

- TEC 7 Module 1Dokumen30 halamanTEC 7 Module 1danrell pasagueBelum ada peringkat

- Mastermind: Business Plan PresentationDokumen23 halamanMastermind: Business Plan PresentationSuhani jainBelum ada peringkat

- TCN Quotation - TCN Vending (16th, March)Dokumen8 halamanTCN Quotation - TCN Vending (16th, March)Gusthavo VidalBelum ada peringkat

- Option Trading Tactics With Oliver VelezDokumen62 halamanOption Trading Tactics With Oliver VelezRenato89% (9)

- CadburyDokumen11 halamanCadburyArchit AprameyanBelum ada peringkat

- MDLZ - Presentation July 20thDokumen12 halamanMDLZ - Presentation July 20thapi-342469173Belum ada peringkat

- Kpis: Improving Supply Chain Performance ManagementDokumen33 halamanKpis: Improving Supply Chain Performance Managementgaumzy091985Belum ada peringkat

- Sample Chapter PDFDokumen36 halamanSample Chapter PDFDinesh KumarBelum ada peringkat

- 19.lewin, David. Human Resources Management in The 21st CenturyDokumen12 halaman19.lewin, David. Human Resources Management in The 21st CenturymiudorinaBelum ada peringkat

- Article - SarfaesiDokumen32 halamanArticle - SarfaesiATUL100% (2)

- Central Sales Tax-2Dokumen8 halamanCentral Sales Tax-2Krystle DseuzaBelum ada peringkat

- Economic Order Quantity & Its Determination: Dr. S. C. Singh Shivam SrivastavaDokumen16 halamanEconomic Order Quantity & Its Determination: Dr. S. C. Singh Shivam Srivastavashivamsrivastava85Belum ada peringkat

- Bbim 4103Dokumen16 halamanBbim 4103Sharifah Md IbrahimBelum ada peringkat

- Adv and Disadv of Using Credit CardsDokumen5 halamanAdv and Disadv of Using Credit CardsSophia RusliBelum ada peringkat

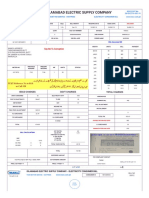

- Iesco Online BilllDokumen2 halamanIesco Online BilllQasimbuttBelum ada peringkat

- (Ind) 3. CHP 10 Horngren - Ca16 - PPT - 10Dokumen47 halaman(Ind) 3. CHP 10 Horngren - Ca16 - PPT - 10SindymhnBelum ada peringkat

- Latest ACI 3I0-012 Exam Training Materials Free TryDokumen5 halamanLatest ACI 3I0-012 Exam Training Materials Free TryGonzalezoesBelum ada peringkat

- Real Property Taxation FINALDokumen54 halamanReal Property Taxation FINALIc San PedroBelum ada peringkat

- Sol. Man. - Chapter 16 - Ppe Part 2 - Ia Part 1B 1Dokumen15 halamanSol. Man. - Chapter 16 - Ppe Part 2 - Ia Part 1B 1Rezzan Joy Camara MejiaBelum ada peringkat

- Chapter 2 - Project Selection and Project Portfolio ProcessDokumen71 halamanChapter 2 - Project Selection and Project Portfolio ProcessNguyễn Xuân TùngBelum ada peringkat

- Explanatory Memorandum SSDokumen23 halamanExplanatory Memorandum SSkalluvarmaBelum ada peringkat

- Company Presentation BY Sudhanshu Kumar Nirala Bba (Semvi) ST - Xavier'S CollegeDokumen20 halamanCompany Presentation BY Sudhanshu Kumar Nirala Bba (Semvi) ST - Xavier'S CollegeAnant JainBelum ada peringkat

- Choice of Tow CarDokumen23 halamanChoice of Tow Carlionheartuk0% (1)

- Net-Metering and The Promotion of Distributed Solar PV Generation in Ghana, Financial and Economic Analysis.Dokumen123 halamanNet-Metering and The Promotion of Distributed Solar PV Generation in Ghana, Financial and Economic Analysis.kanahumaBelum ada peringkat

- Andrew Coulson - Tanzania - A Political Economy (2013, Oxford University Press) PDFDokumen441 halamanAndrew Coulson - Tanzania - A Political Economy (2013, Oxford University Press) PDFemmanuel santoyo rioBelum ada peringkat

- VP Engineering and Service: Purchase OrderDokumen1 halamanVP Engineering and Service: Purchase OrderVP Engineering & Service BangaloreBelum ada peringkat

- Notes - Reasons For High Inventory Holding CostsDokumen4 halamanNotes - Reasons For High Inventory Holding Costsmaria luzBelum ada peringkat

- (ECONOMICS) Basic Concepts in MicroeconomicsDokumen12 halaman(ECONOMICS) Basic Concepts in Microeconomicschlsc50% (2)

- Pricing StrategiesDokumen58 halamanPricing StrategiesMark K. Eapen100% (2)

- HCL Aptitude QuestionsDokumen6 halamanHCL Aptitude QuestionsAbhishek SoniBelum ada peringkat

- Investment Basics I: ObjectivesDokumen14 halamanInvestment Basics I: Objectivesno nameBelum ada peringkat