Anda mungkin juga menyukai

- Target CostingDokumen17 halamanTarget CostingMoshmi MazumdarBelum ada peringkat

- McKinsey & Co - Nonprofit Board Self-Assessment Tool Short FormDokumen6 halamanMcKinsey & Co - Nonprofit Board Self-Assessment Tool Short Formmoctapka088100% (1)

- Target CostingDokumen4 halamanTarget CostingPriya KudnekarBelum ada peringkat

- Develop Your Kuji In Ability in Body and MindDokumen7 halamanDevelop Your Kuji In Ability in Body and MindLenjivac100% (3)

- Life Cycle CostingDokumen38 halamanLife Cycle CostingD A N Ī S HBelum ada peringkat

- Ch20 Introducing New Market OfferingsDokumen2 halamanCh20 Introducing New Market OfferingsRina Fordan BilogBelum ada peringkat

- Just-in-Time and Lean OperationsDokumen90 halamanJust-in-Time and Lean OperationsSaad PirzadaBelum ada peringkat

- Cost and Management AccountingDokumen29 halamanCost and Management AccountingAks SinhaBelum ada peringkat

- Throughput Accounting and The Theory of ConstraintsDokumen8 halamanThroughput Accounting and The Theory of ConstraintsMd AzimBelum ada peringkat

- (MCQ) - Arithmetic ProgressionDokumen5 halaman(MCQ) - Arithmetic Progressionrahul aravindBelum ada peringkat

- CVP Analysis TechniquesDokumen45 halamanCVP Analysis TechniquesYitera SisayBelum ada peringkat

- Pricing MethodsDokumen3 halamanPricing MethodsAkanksha VermaBelum ada peringkat

- 3.sales Variance AnalysisDokumen38 halaman3.sales Variance Analysiskamasuke hegdeBelum ada peringkat

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Dokumen31 halamanLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentBelum ada peringkat

- McCann MIA CredentialsDokumen20 halamanMcCann MIA CredentialsgbertainaBelum ada peringkat

- Wal-Mart's Balance Scorecard StrategyDokumen13 halamanWal-Mart's Balance Scorecard StrategyMIRAL PATELBelum ada peringkat

- Activity Design ScoutingDokumen10 halamanActivity Design ScoutingHoneyjo Nette100% (9)

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDokumen23 halamanProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombeBelum ada peringkat

- Variable Production Overhead Variance (VPOH)Dokumen9 halamanVariable Production Overhead Variance (VPOH)Wee Han ChiangBelum ada peringkat

- C1 Reading 1Dokumen2 halamanC1 Reading 1Alejandros BrosBelum ada peringkat

- Performance Management 1Dokumen159 halamanPerformance Management 1CleavonTenorioBelum ada peringkat

- Additional Aspects of Costing SystemsDokumen28 halamanAdditional Aspects of Costing SystemsKağan GrrgnBelum ada peringkat

- BM Introduction To BankingDokumen36 halamanBM Introduction To BankingNatasha OliviaBelum ada peringkat

- Just in Time Production: By-Tanvi Bhatia Swaranjeet Choudhary Sonal ShaileshDokumen14 halamanJust in Time Production: By-Tanvi Bhatia Swaranjeet Choudhary Sonal ShaileshDivya HarithaBelum ada peringkat

- Basel 3Dokumen32 halamanBasel 3Venkat SaiBelum ada peringkat

- Chapter 7Dokumen53 halamanChapter 7Baby KhorBelum ada peringkat

- CH 8Dokumen16 halamanCH 8emanmamdouh596Belum ada peringkat

- JitDokumen26 halamanJitRachanakumari100% (1)

- Finance Assignment InstructionDokumen7 halamanFinance Assignment InstructionJe-Ta CllBelum ada peringkat

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDokumen79 halamanLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaBelum ada peringkat

- CH 3 JITDokumen68 halamanCH 3 JITmaheshgBelum ada peringkat

- Standard Costing and Variance Analysis: Fall 2007 CrossonDokumen20 halamanStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaBelum ada peringkat

- Overhead VariancesDokumen11 halamanOverhead VariancesDanica VillaganteBelum ada peringkat

- Just in Time and BackflushingDokumen25 halamanJust in Time and BackflushingSilvani Margaretha SimangunsongBelum ada peringkat

- Financial Derivatives: Prof. Scott JoslinDokumen49 halamanFinancial Derivatives: Prof. Scott Joslinarnav100% (2)

- Productivity and Reliability-Based Maintenance Management, Second EditionDari EverandProductivity and Reliability-Based Maintenance Management, Second EditionBelum ada peringkat

- Target Costing, Kaizen Costing and Life Cycle Costing: Advanced Cost AccountingDokumen20 halamanTarget Costing, Kaizen Costing and Life Cycle Costing: Advanced Cost AccountingFatemaBelum ada peringkat

- Cost ManagementDokumen18 halamanCost ManagementGeo Rublico ManilaBelum ada peringkat

- Livros Vet LinksDokumen12 halamanLivros Vet LinksÉrica RebeloBelum ada peringkat

- Activity Emcee Mid-Year INSET 2021Dokumen3 halamanActivity Emcee Mid-Year INSET 2021Abegail A. Alangue-Calimag67% (6)

- Ch-8 (Managing Products, Product Lines, Brands, Packaging)Dokumen18 halamanCh-8 (Managing Products, Product Lines, Brands, Packaging)api-19958143Belum ada peringkat

- Backflush Costing, Kaizen Costing, and Strategic CostingDokumen9 halamanBackflush Costing, Kaizen Costing, and Strategic CostingShofiqBelum ada peringkat

- Strategic Planning and Control True/False QuestionsDokumen28 halamanStrategic Planning and Control True/False QuestionsReneeBelum ada peringkat

- Theory of CostraintsDokumen14 halamanTheory of CostraintsDaisy AroraBelum ada peringkat

- Module IV - Working Capital ManagementDokumen50 halamanModule IV - Working Capital ManagementAshwin DholeBelum ada peringkat

- Balanced Scorecard and Benchmarking StrategiesDokumen12 halamanBalanced Scorecard and Benchmarking StrategiesGaurav Sharma100% (1)

- Activity-Based Costing: A Guide to Calculating True Product CostsDokumen3 halamanActivity-Based Costing: A Guide to Calculating True Product CostsRoikhanatun Nafi'ahBelum ada peringkat

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDokumen58 halamanChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifBelum ada peringkat

- Target CostingDokumen32 halamanTarget CostingOnkar SawantBelum ada peringkat

- Lecture 2 Quality ManagementDokumen22 halamanLecture 2 Quality ManagementWilliam DC RiveraBelum ada peringkat

- International FInanceDokumen3 halamanInternational FInanceJemma JadeBelum ada peringkat

- Transfer Pricing MethodsDokumen41 halamanTransfer Pricing MethodsExcel100% (1)

- Quantitative Analysis For Management: Thirteenth Edition, Global EditionDokumen127 halamanQuantitative Analysis For Management: Thirteenth Edition, Global EditionMpho NkuBelum ada peringkat

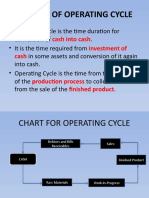

- Concept of Operating Cycle: Cash Into Cash Investment of CashDokumen6 halamanConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaBelum ada peringkat

- CHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)Dokumen54 halamanCHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)kenchong7150% (1)

- Bilaspur University presentation on managerial economics cost theoryDokumen22 halamanBilaspur University presentation on managerial economics cost theoryVi Pin SinghBelum ada peringkat

- 7 JitDokumen36 halaman7 JitFatima AsadBelum ada peringkat

- The Learning CurveDokumen17 halamanThe Learning CurvemohitkripalaniBelum ada peringkat

- Marginal CostingDokumen31 halamanMarginal Costingdivya dharmarajan50% (4)

- Measuring and Assigning Support Department CostsDokumen46 halamanMeasuring and Assigning Support Department CostsRavikumar Sampath100% (1)

- ThroughputDokumen15 halamanThroughputVaibhav KocharBelum ada peringkat

- Focussed FactoryDokumen13 halamanFocussed FactoryjcspaiBelum ada peringkat

- Wages and Salary AdministrationDokumen47 halamanWages and Salary Administrationsaha apurvaBelum ada peringkat

- Total Quality Management Toyota: Presented By: Rajat Tiwari Richa Vaish Shipra Singh Mba (G) Sem Ii Sec B ABSDokumen20 halamanTotal Quality Management Toyota: Presented By: Rajat Tiwari Richa Vaish Shipra Singh Mba (G) Sem Ii Sec B ABSmou777Belum ada peringkat

- 4 CVP AnalysisDokumen36 halaman4 CVP AnalysisBibaswan BanerjeeBelum ada peringkat

- 4 Ps of MarketingDokumen6 halaman4 Ps of Marketingfaizan 89Belum ada peringkat

- Just in TimeDokumen24 halamanJust in TimeMrinal KalitaBelum ada peringkat

- A Project On The Economic Order QuantityDokumen26 halamanA Project On The Economic Order QuantityFortune Fmx MushongaBelum ada peringkat

- Portfolio Evaluation Tools For InsuranceDokumen12 halamanPortfolio Evaluation Tools For InsuranceAks SinhaBelum ada peringkat

- Methods of CostingDokumen20 halamanMethods of CostingAks SinhaBelum ada peringkat

- Tax Planning MergerDokumen4 halamanTax Planning MergerAks SinhaBelum ada peringkat

- Tax CLASS NOTESDokumen17 halamanTax CLASS NOTESAks SinhaBelum ada peringkat

- Cost and Management AccountingDokumen18 halamanCost and Management AccountingAks SinhaBelum ada peringkat

- CMA Unit3Dokumen17 halamanCMA Unit3Aks SinhaBelum ada peringkat

- Benefits of Sunder KandDokumen1 halamanBenefits of Sunder KandAks SinhaBelum ada peringkat

- Cost and Management AccountingDokumen18 halamanCost and Management AccountingAks SinhaBelum ada peringkat

- Life Cycle CostingDokumen9 halamanLife Cycle CostingAks SinhaBelum ada peringkat

- Cost ManagementDokumen13 halamanCost ManagementAks SinhaBelum ada peringkat

- Mr. Rakesh Kumar Mittal, IAS (Retd.) at SMS VaranasiDokumen1 halamanMr. Rakesh Kumar Mittal, IAS (Retd.) at SMS VaranasiAks SinhaBelum ada peringkat

- Reforming Indirect Taxes in IndiaDokumen18 halamanReforming Indirect Taxes in IndiaAks SinhaBelum ada peringkat

- Instant Food ReportDokumen85 halamanInstant Food ReportAks SinhaBelum ada peringkat

- Corporate Tax PlanningDokumen10 halamanCorporate Tax PlanningAks Sinha100% (3)

- Tax Planning and ManagementDokumen23 halamanTax Planning and ManagementAks Sinha100% (2)

- International Business EnvironmentDokumen32 halamanInternational Business EnvironmentAks Sinha100% (1)

- Naure and Scope of Consumer BehaviourDokumen13 halamanNaure and Scope of Consumer BehaviourChandeshwar PaikraBelum ada peringkat

- Mind MapDokumen1 halamanMind Mapjebzkiah productionBelum ada peringkat

- Writing and Presenting A Project Proposal To AcademicsDokumen87 halamanWriting and Presenting A Project Proposal To AcademicsAllyBelum ada peringkat

- Dimensioning GuidelinesDokumen1 halamanDimensioning GuidelinesNabeela TunisBelum ada peringkat

- Malla Reddy Engineering College (Autonomous)Dokumen17 halamanMalla Reddy Engineering College (Autonomous)Ranjith KumarBelum ada peringkat

- RAGHAV Sound DesignDokumen16 halamanRAGHAV Sound DesignRaghav ChaudhariBelum ada peringkat

- Fazlur Khan - Father of Tubular Design for Tall BuildingsDokumen19 halamanFazlur Khan - Father of Tubular Design for Tall BuildingsyisauBelum ada peringkat

- Proportions PosterDokumen1 halamanProportions Posterapi-214764900Belum ada peringkat

- Date ValidationDokumen9 halamanDate ValidationAnonymous 9B0VdTWiBelum ada peringkat

- Agricultural Typology Concept and MethodDokumen13 halamanAgricultural Typology Concept and MethodAre GalvánBelum ada peringkat

- Nektar Impact LX25 (En)Dokumen32 halamanNektar Impact LX25 (En)Camila Gonzalez PiatBelum ada peringkat

- CV Raman's Discovery of the Raman EffectDokumen10 halamanCV Raman's Discovery of the Raman EffectjaarthiBelum ada peringkat

- Assignment 1 - Tiered LessonDokumen15 halamanAssignment 1 - Tiered Lessonapi-320736246Belum ada peringkat

- Remapping The Small Things PDFDokumen101 halamanRemapping The Small Things PDFAme RaBelum ada peringkat

- RBI and Maintenance For RCC Structure SeminarDokumen4 halamanRBI and Maintenance For RCC Structure SeminarcoxshulerBelum ada peringkat

- DCinv V6 Rev2 CleanDokumen38 halamanDCinv V6 Rev2 Cleanyasirarafat91Belum ada peringkat

- Studies On Diffusion Approach of MN Ions Onto Granular Activated CarbonDokumen7 halamanStudies On Diffusion Approach of MN Ions Onto Granular Activated CarbonInternational Journal of Application or Innovation in Engineering & ManagementBelum ada peringkat

- JEE Test Series ScheduleDokumen4 halamanJEE Test Series ScheduleB.K.Sivaraj rajBelum ada peringkat

- Lesson Plan V The ImperativeDokumen3 halamanLesson Plan V The ImperativeViviana Bursuc100% (1)

- NIT JRF OpportunityDokumen4 halamanNIT JRF Opportunitybalaguru78Belum ada peringkat

- Justice, Governance, CosmopolitanismDokumen152 halamanJustice, Governance, CosmopolitanismIban MiusikBelum ada peringkat

- ASTM C 136 Sieve Analysis of Fine and Coarse Aggregates (D)Dokumen5 halamanASTM C 136 Sieve Analysis of Fine and Coarse Aggregates (D)Yasir DharejoBelum ada peringkat

- 【小马过河】35 TOEFL iBT Speaking Frequent WordsDokumen10 halaman【小马过河】35 TOEFL iBT Speaking Frequent WordskakiwnBelum ada peringkat