Anda mungkin juga menyukai

- MCL CIL Laptop SchemeDokumen12 halamanMCL CIL Laptop SchemeDhruv ChatterjeeBelum ada peringkat

- 1322458912564-Org ChartDokumen1 halaman1322458912564-Org ChartDhruv ChatterjeeBelum ada peringkat

- CoalIndia Executives HRA Rules 2010 OrderNo 1499 Dt28092010Dokumen14 halamanCoalIndia Executives HRA Rules 2010 OrderNo 1499 Dt28092010Dhruv ChatterjeeBelum ada peringkat

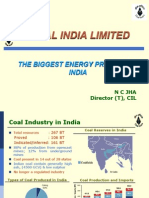

- Coal India Limited - The Biggest Energy Provider in IndiaDokumen27 halamanCoal India Limited - The Biggest Energy Provider in IndiaDhruv ChatterjeeBelum ada peringkat

- Exectv HRA Revised FlatDokumen4 halamanExectv HRA Revised FlatDhruv ChatterjeeBelum ada peringkat

- Exectv HRA Revised FlatDokumen4 halamanExectv HRA Revised FlatDhruv ChatterjeeBelum ada peringkat

- Routine For 4th Sem 2014 WBUTDokumen11 halamanRoutine For 4th Sem 2014 WBUTDhruv ChatterjeeBelum ada peringkat

- Cutt Off SynopsisDokumen13 halamanCutt Off SynopsisDhruv ChatterjeeBelum ada peringkat

- Sample Question Papers For MT 2014 25042014Dokumen10 halamanSample Question Papers For MT 2014 25042014smartersmartyBelum ada peringkat

- Kingfisher Airlines Performance and Financial TurmoilDokumen2 halamanKingfisher Airlines Performance and Financial TurmoilDhruv ChatterjeeBelum ada peringkat

- Kingfisher Airlines Performance and Financial TurmoilDokumen2 halamanKingfisher Airlines Performance and Financial TurmoilDhruv ChatterjeeBelum ada peringkat

- Burns & ScaidsDokumen3 halamanBurns & ScaidsDhruv ChatterjeeBelum ada peringkat

- Soil Physical RelationsDokumen1 halamanSoil Physical Relationszaheer0406Belum ada peringkat

- HR Management Multiple Choice QuestionsDokumen3 halamanHR Management Multiple Choice QuestionsYogendra Tiwari60% (5)

- Pile Foundation DesignDokumen70 halamanPile Foundation DesignDhruv ChatterjeeBelum ada peringkat

- Pile Foundation DesignDokumen70 halamanPile Foundation DesignDhruv ChatterjeeBelum ada peringkat

- Extraction of Developed Coal Pillars in SCCL, CILDokumen16 halamanExtraction of Developed Coal Pillars in SCCL, CILDhruv ChatterjeeBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Tata Steel Annual Report 2009 10Dokumen236 halamanTata Steel Annual Report 2009 10Rahul SinhaBelum ada peringkat

- Fundamental Equity Analysis & Analyst Recommendations - STOXX Large 200 Index ComponentsDokumen401 halamanFundamental Equity Analysis & Analyst Recommendations - STOXX Large 200 Index ComponentsQ.M.S Advisors LLCBelum ada peringkat

- Profit and Loss AccountDokumen2 halamanProfit and Loss AccountAstri HandayaniBelum ada peringkat

- Icahn - Earnings Presentation (9.30.20) VfinalDokumen21 halamanIcahn - Earnings Presentation (9.30.20) VfinalMiguel RamosBelum ada peringkat

- Essel Propack LTD: Blackstone Acquires Promoter's StakeDokumen4 halamanEssel Propack LTD: Blackstone Acquires Promoter's StakeanjugaduBelum ada peringkat

- Capital Structure of DR Reddy's LaboratoriesDokumen11 halamanCapital Structure of DR Reddy's LaboratoriesNikhil KumarBelum ada peringkat

- Equity Market Outlook 2018 Sinarmas Sekuritas - Powering The Economy PDFDokumen124 halamanEquity Market Outlook 2018 Sinarmas Sekuritas - Powering The Economy PDFfielimkarelBelum ada peringkat

- A Case Study On Changing Depreciation Methods and Quality of DisclosureDokumen13 halamanA Case Study On Changing Depreciation Methods and Quality of DisclosureDEMI0% (1)

- Formula SheetDokumen9 halamanFormula Sheetrocky2219Belum ada peringkat

- Aetna HumanaInvestorPresentationDokumen35 halamanAetna HumanaInvestorPresentationgregBelum ada peringkat

- Voltamp Transformers LTD: Result UpdateDokumen5 halamanVoltamp Transformers LTD: Result Updatevipin51Belum ada peringkat

- QS MbaDokumen222 halamanQS MbaAmaranath MedavarapuBelum ada peringkat

- Accounting For ValueDokumen15 halamanAccounting For Valueolst100% (5)

- FSA (Non) PDFDokumen469 halamanFSA (Non) PDFmubashar0092Belum ada peringkat

- Lc160808 PresentationDokumen28 halamanLc160808 PresentationCrowdfundInsiderBelum ada peringkat

- West Coast Paper Mills LTDDokumen9 halamanWest Coast Paper Mills LTDSneha SinghalBelum ada peringkat

- Sample Interior Business Plan Template PDFDokumen43 halamanSample Interior Business Plan Template PDFLinda zubyBelum ada peringkat

- A Cross-Border Cap BudgetingDokumen18 halamanA Cross-Border Cap BudgetingGaurav VermaBelum ada peringkat

- Ijrcm 1 Vol 3 Issue 1 Art 22Dokumen14 halamanIjrcm 1 Vol 3 Issue 1 Art 22mohan chouriwarBelum ada peringkat

- 2012 - ALTO - ALTO - Annual Report PDFDokumen120 halaman2012 - ALTO - ALTO - Annual Report PDFNuvita Puji KriswantiBelum ada peringkat

- Strengths and WeeknessesDokumen14 halamanStrengths and WeeknessesAriel AlvarezBelum ada peringkat

- JFC Consolidated Financial Statements 2018 PDFDokumen132 halamanJFC Consolidated Financial Statements 2018 PDFPHILLIP PACLEBBelum ada peringkat

- Financial RatiosDokumen8 halamanFinancial Ratiosavinash singhBelum ada peringkat

- Cervecería Nacional - FinanzasDokumen39 halamanCervecería Nacional - FinanzasLuismy VacacelaBelum ada peringkat

- The Insites: Vishnu Prayag Hydro Power Project (400Mw)Dokumen12 halamanThe Insites: Vishnu Prayag Hydro Power Project (400Mw)kittieyBelum ada peringkat

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokumen6 halamanAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaBelum ada peringkat

- (FINAL) - TELKOMSEL 2018AR Web-Ver PDFDokumen180 halaman(FINAL) - TELKOMSEL 2018AR Web-Ver PDFnanda bstnBelum ada peringkat

- March Quarter 2019 and Full Fiscal Year 2019 Results: ConfidentialDokumen17 halamanMarch Quarter 2019 and Full Fiscal Year 2019 Results: ConfidentialJ. BangjakBelum ada peringkat

- Naïade Resorts Annual Report Highlights Strong PerformanceDokumen112 halamanNaïade Resorts Annual Report Highlights Strong PerformanceRamchundar KarunaBelum ada peringkat

- Executive SummaryDokumen13 halamanExecutive SummaryTuấn Anh Hoàng100% (1)