Anda mungkin juga menyukai

- Tire City AnalysisDokumen3 halamanTire City AnalysisKailash HegdeBelum ada peringkat

- Tire City IncDokumen12 halamanTire City Incdownloadsking100% (1)

- Tire CityDokumen3 halamanTire CityenypurwaningsihBelum ada peringkat

- 93-Tire-City 22 22Dokumen26 halaman93-Tire-City 22 22Daniel InfanteBelum ada peringkat

- Tire City Inc.Dokumen6 halamanTire City Inc.Samta Singh YadavBelum ada peringkat

- Tire City SolutionDokumen4 halamanTire City SolutionUmeshKumarBelum ada peringkat

- Tire City AssignmentDokumen7 halamanTire City AssignmentShivam Kanojia100% (1)

- Netscape ProformaDokumen6 halamanNetscape ProformabobscribdBelum ada peringkat

- Tire City IncDokumen12 halamanTire City IncMahesh Kumar Meena100% (1)

- Tire City CaseDokumen12 halamanTire City CaseAngela ThorntonBelum ada peringkat

- Tire City AssignmentDokumen6 halamanTire City AssignmentXRiloXBelum ada peringkat

- Tire - City AnalysisDokumen17 halamanTire - City AnalysisJustin HoBelum ada peringkat

- Tire City Spreadsheet SolutionDokumen6 halamanTire City Spreadsheet Solutionalmasy99100% (1)

- Tire City IncDokumen5 halamanTire City IncAfrin FarhanaBelum ada peringkat

- Tire CityDokumen3 halamanTire Cityrahulchohan2108Belum ada peringkat

- Tire City Inc. Case StudyDokumen8 halamanTire City Inc. Case StudyKyeli TanBelum ada peringkat

- Marriott Solutions WACC LodgingDokumen3 halamanMarriott Solutions WACC LodgingPabloCaicedoArellanoBelum ada peringkat

- Ameritrade Case SolutionDokumen34 halamanAmeritrade Case SolutionAbhishek GargBelum ada peringkat

- Tire City, Inc - Examen FinalDokumen3 halamanTire City, Inc - Examen Finalmacro_jBelum ada peringkat

- Tire City Spreadsheet SolutionDokumen8 halamanTire City Spreadsheet SolutionsuwimolJBelum ada peringkat

- Tire City Spreadsheet SolutionDokumen7 halamanTire City Spreadsheet SolutionSyed Ali MurtuzaBelum ada peringkat

- Clarkson Lumber Analysis - TylerDokumen9 halamanClarkson Lumber Analysis - TylerTyler TreadwayBelum ada peringkat

- Debt Policy at UST Inc.Dokumen47 halamanDebt Policy at UST Inc.karthikk1990100% (2)

- Case Analysis - Toy WorldDokumen11 halamanCase Analysis - Toy Worldvarjin71% (7)

- Tire City Case 1Dokumen28 halamanTire City Case 1Srikanth VasantadaBelum ada peringkat

- Session 19 - Dividend Policy at Linear TechDokumen2 halamanSession 19 - Dividend Policy at Linear TechRichBrook7Belum ada peringkat

- Excel File Exhibits For Marriott CaseDokumen18 halamanExcel File Exhibits For Marriott Caset3ddyme123Belum ada peringkat

- Tire City Case AnalysisDokumen10 halamanTire City Case AnalysisVASANTADA SRIKANTH (PGP 2016-18)Belum ada peringkat

- Tire City AnalysisDokumen1 halamanTire City AnalysisNikhil Kangutkar80% (10)

- Nike Case AnalysisDokumen9 halamanNike Case AnalysisFami FamzBelum ada peringkat

- Energy GelDokumen4 halamanEnergy Gelchetan DuaBelum ada peringkat

- Toy World - ExhibitsDokumen9 halamanToy World - Exhibitsakhilkrishnan007Belum ada peringkat

- Tire City SolutionDokumen2 halamanTire City Solutionadityaintouch60% (5)

- Netscape CaseDokumen6 halamanNetscape CaseVikram RathiBelum ada peringkat

- RJR Nabisco ValuationDokumen33 halamanRJR Nabisco ValuationKrishna Chaitanya KothapalliBelum ada peringkat

- Case Study Debt Policy Ust IncDokumen10 halamanCase Study Debt Policy Ust IncIrfan MohdBelum ada peringkat

- Tire City AssignmentDokumen6 halamanTire City AssignmentderronsBelum ada peringkat

- Case StudyDokumen10 halamanCase StudyEvelyn VillafrancaBelum ada peringkat

- Tire CityDokumen5 halamanTire CitySudip BrahmacharyBelum ada peringkat

- Midland Energy Resources Inc SolutionDokumen2 halamanMidland Energy Resources Inc SolutionAashna MehtaBelum ada peringkat

- Assessing Earnings Quality at NuwareDokumen7 halamanAssessing Earnings Quality at Nuwaremyhellonearth0% (1)

- Tire City Case Study SolutionDokumen2 halamanTire City Case Study SolutionPrathap Sankar0% (1)

- Nike Inc. Case StudyDokumen3 halamanNike Inc. Case Studyshikhagupta3288Belum ada peringkat

- Midland Case CalculationsDokumen24 halamanMidland Case CalculationsSharry_xxx60% (5)

- Tire City Case SolutionDokumen6 halamanTire City Case SolutionShivam Bhasin60% (10)

- Case Report FinalDokumen12 halamanCase Report Finalsimplyabeer100% (3)

- FIN RealOptionsDokumen3 halamanFIN RealOptionsveda20Belum ada peringkat

- Uttam Kumar Sec-A Dividend Policy Linear TechnologyDokumen11 halamanUttam Kumar Sec-A Dividend Policy Linear TechnologyUttam Kumar100% (1)

- Midland EnergyDokumen9 halamanMidland EnergyPrashant MishraBelum ada peringkat

- WorldCom Bond IssuanceDokumen9 halamanWorldCom Bond IssuanceAniket DubeyBelum ada peringkat

- Case 51 Palamon Capital Partners Team System SPADokumen10 halamanCase 51 Palamon Capital Partners Team System SPAcrs50% (2)

- Alliance Concrete ForecastingDokumen7 halamanAlliance Concrete ForecastingS r kBelum ada peringkat

- FMG Comsat FCCDokumen18 halamanFMG Comsat FCCMuhammad Rizwan AsimBelum ada peringkat

- Case Submission - Stone Container Corporation (A) ' Group VIIIDokumen5 halamanCase Submission - Stone Container Corporation (A) ' Group VIIIGURNEET KAURBelum ada peringkat

- Corporate Valuation: Group - 2Dokumen6 halamanCorporate Valuation: Group - 2RiturajPaulBelum ada peringkat

- UST Debt Policy SpreadsheetDokumen9 halamanUST Debt Policy Spreadsheetjchodgson0% (2)

- Vocabulary English For AccountingDokumen8 halamanVocabulary English For AccountingMi NhonBelum ada peringkat

- Ch. 12 Financial Planning and Forecasting Financial Statements The Financial PlanDokumen6 halamanCh. 12 Financial Planning and Forecasting Financial Statements The Financial PlanAnis AtmojoBelum ada peringkat

- Exhibit 6.3 Margin Money For Working CapitalDokumen12 halamanExhibit 6.3 Margin Money For Working Capitalanon_285857320Belum ada peringkat

- Solution To Y Guess Jeans:: Item 1. Consolidated Financial StatementsDokumen7 halamanSolution To Y Guess Jeans:: Item 1. Consolidated Financial StatementsAbuBakarSiddiqueBelum ada peringkat

- Salary Certificate FormatDokumen1 halamanSalary Certificate FormatshajahanBelum ada peringkat

- Problem 10Dokumen2 halamanProblem 10novyBelum ada peringkat

- BIR Ruling No. 317-18 (BVI Law)Dokumen3 halamanBIR Ruling No. 317-18 (BVI Law)Liz100% (1)

- Audit Problems CashDokumen18 halamanAudit Problems CashYenelyn Apistar Cambarijan0% (1)

- In The United States Bankruptcy Court For The District of Delaware in Re:) Chapter 11 Pacific Energy Resources LTD., Et Al.,') Case No. 09-10785 (KJC) ) (Jointly Administered) Debtor.)Dokumen67 halamanIn The United States Bankruptcy Court For The District of Delaware in Re:) Chapter 11 Pacific Energy Resources LTD., Et Al.,') Case No. 09-10785 (KJC) ) (Jointly Administered) Debtor.)Chapter 11 DocketsBelum ada peringkat

- Abella vs. Abella GR No. 195166 July 08, 2015Dokumen6 halamanAbella vs. Abella GR No. 195166 July 08, 2015ErikEspinoBelum ada peringkat

- New BIT Structure For 081 AboveDokumen17 halamanNew BIT Structure For 081 Aboveعلي برادةBelum ada peringkat

- 92611902-KrugmanMacro SM Ch19 PDFDokumen6 halaman92611902-KrugmanMacro SM Ch19 PDFAlejandro Fernandez RodriguezBelum ada peringkat

- Accounting For Income TaxDokumen14 halamanAccounting For Income TaxJasmin Gubalane100% (1)

- TallyPrime Essential Level 2Dokumen26 halamanTallyPrime Essential Level 2Lavanya TBelum ada peringkat

- Indian Income Tax Return Acknowledgement 2020-21: Esappo445Q Mohan Prathap PandianDokumen4 halamanIndian Income Tax Return Acknowledgement 2020-21: Esappo445Q Mohan Prathap PandianVignesh KanagarajBelum ada peringkat

- A Case Study On Moser BaerDokumen13 halamanA Case Study On Moser BaerShubham AgarwalBelum ada peringkat

- 3.kingsun Financial Statement FinalDokumen22 halaman3.kingsun Financial Statement FinalDharamrajBelum ada peringkat

- Brokerage Agreement-ExclusiveDokumen3 halamanBrokerage Agreement-ExclusiveMarvin B. SoteloBelum ada peringkat

- Co Operative SocietyDokumen101 halamanCo Operative SocietyRaghu Ck100% (2)

- Recruitment Selection Process in HDFCDokumen102 halamanRecruitment Selection Process in HDFCaccord123100% (2)

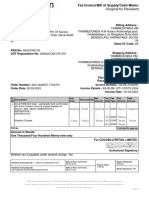

- InvoiceDokumen2 halamanInvoiceTHIMMEGOWDA H MBelum ada peringkat

- Fin Ca2 FinalDokumen6 halamanFin Ca2 FinalVaishali SonareBelum ada peringkat

- IA2 Chapter 20 ActivitiesDokumen13 halamanIA2 Chapter 20 ActivitiesShaina TorraineBelum ada peringkat

- A Study On Claims ManagementDokumen77 halamanA Study On Claims Managementarjunmba119624100% (2)

- Chapter OneDokumen119 halamanChapter Onegary galangBelum ada peringkat

- Ms8-Set A Midterm - With AnswersDokumen5 halamanMs8-Set A Midterm - With AnswersOscar Bocayes Jr.Belum ada peringkat

- Auditing MCQs Multiple Choice Questions and Answers 2023 - Auditing MCQs For B.Com, CA, CS and CMA ExamsDokumen38 halamanAuditing MCQs Multiple Choice Questions and Answers 2023 - Auditing MCQs For B.Com, CA, CS and CMA Examsvenakata3722Belum ada peringkat

- Ssi FinancingDokumen7 halamanSsi FinancingAnanya ChoudharyBelum ada peringkat

- Sales Invoice: Customer InformationDokumen1 halamanSales Invoice: Customer InformationRaghavendra S DBelum ada peringkat

- UPSA 2019 Tutorial Questions Fs WITH ANSWERSDokumen14 halamanUPSA 2019 Tutorial Questions Fs WITH ANSWERSLaud ListowellBelum ada peringkat

- Mamis Last LetterDokumen10 halamanMamis Last LetterTBP_Think_Tank100% (3)

- India Cements Result UpdatedDokumen12 halamanIndia Cements Result UpdatedAngel BrokingBelum ada peringkat

- Audit of Property, Plant and Equipment: Auditing ProblemsDokumen5 halamanAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanBelum ada peringkat

- Tabel DFDokumen15 halamanTabel DFSexy TofuBelum ada peringkat