Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Electronic New Government Accounting SystemDokumen61 halamanElectronic New Government Accounting SystemJoseph PamaongBelum ada peringkat

- Employee Loan ApplicationDokumen2 halamanEmployee Loan Applicationdexdex110% (1)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- (Davey) Entry and Exit Confessions of A Champion Trader 52 WaysDokumen214 halaman(Davey) Entry and Exit Confessions of A Champion Trader 52 Wayssim tykes67% (3)

- Securitization of DebtDokumen52 halamanSecuritization of Debtnjsnghl100% (1)

- Treasury & Capital MarketsDokumen5 halamanTreasury & Capital MarketsHIMANSHI MADANBelum ada peringkat

- Wealth Management & Asset ManagementDokumen32 halamanWealth Management & Asset ManagementVineetChandakBelum ada peringkat

- Assessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesDokumen5 halamanAssessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesYingzhi XuBelum ada peringkat

- Tugas - Strategic Planning For The Family in BussinesDokumen10 halamanTugas - Strategic Planning For The Family in BussinestariBelum ada peringkat

- Ch-12 Innovation and EntrepeneurshipDokumen23 halamanCh-12 Innovation and EntrepeneurshiptariBelum ada peringkat

- Ch-12 Innovation and EntrepeneurshipDokumen23 halamanCh-12 Innovation and EntrepeneurshiptariBelum ada peringkat

- Fig 12Dokumen20 halamanFig 12tariBelum ada peringkat

- Strategic Capacity Planning and Ideal Process CapacityDokumen31 halamanStrategic Capacity Planning and Ideal Process CapacitytariBelum ada peringkat

- Lecture 6Dokumen9 halamanLecture 6tariBelum ada peringkat

- Local Currency Change For A Consolidation UnitDokumen6 halamanLocal Currency Change For A Consolidation UnittariBelum ada peringkat

- Note Parallel Currency 1Dokumen5 halamanNote Parallel Currency 1tariBelum ada peringkat

- Fsa SVBDokumen5 halamanFsa SVBlakshya jainBelum ada peringkat

- Allahabad Bank Auction of Mortgaged Property in BhubaneswarDokumen1 halamanAllahabad Bank Auction of Mortgaged Property in BhubaneswarDesikanBelum ada peringkat

- TAX of PinalizeDokumen19 halamanTAX of PinalizeDennis IsananBelum ada peringkat

- Lazy Lagoon Sarovar Portico Suites: Hotel Confirmation VoucherDokumen2 halamanLazy Lagoon Sarovar Portico Suites: Hotel Confirmation VoucherHimanshu WadaskarBelum ada peringkat

- IDBICapital Auto Sep2010Dokumen73 halamanIDBICapital Auto Sep2010raj.mehta2103Belum ada peringkat

- Departamento de Matemáticas: Mathematics - 3º E.S.ODokumen2 halamanDepartamento de Matemáticas: Mathematics - 3º E.S.OketraBelum ada peringkat

- Bank entitled to sell pledged shares in default of Islamic facilityDokumen16 halamanBank entitled to sell pledged shares in default of Islamic facilityabdul rahimBelum ada peringkat

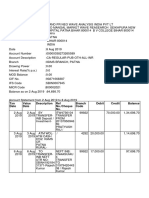

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDokumen3 halamanTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaBelum ada peringkat

- BENEFITS ILLUSTRATIONDokumen2 halamanBENEFITS ILLUSTRATIONRon CatalanBelum ada peringkat

- Monthly Digest from Byju's Exam Prep provides important news and events of February 2022Dokumen31 halamanMonthly Digest from Byju's Exam Prep provides important news and events of February 2022PRADIP WANIBelum ada peringkat

- Tax 2 4Dokumen9 halamanTax 2 4amlecdeyojBelum ada peringkat

- Curtain InvoiceDokumen1 halamanCurtain Invoicebilalahmad566Belum ada peringkat

- IASB Conceptual Framework OverviewDokumen28 halamanIASB Conceptual Framework OverviewTinoManhangaBelum ada peringkat

- Banking Industry Adopts Augmented RealityDokumen50 halamanBanking Industry Adopts Augmented RealityAkash KatiyarBelum ada peringkat

- of CommodityDokumen9 halamanof CommoditysusiracharyaBelum ada peringkat

- Cash in Bank Register: Appendix 37Dokumen2 halamanCash in Bank Register: Appendix 37Lani LacarrozaBelum ada peringkat

- The WheelDokumen6 halamanThe Wheeldantulo1234Belum ada peringkat

- PrefaceDokumen49 halamanPrefaceManish RajakBelum ada peringkat

- A Study On Customer Satisfaction of Reliance Life InsuranceDokumen57 halamanA Study On Customer Satisfaction of Reliance Life InsuranceRishabh PandeBelum ada peringkat

- Court Rules Expropriation for Private Subdivision Not Valid Public UseDokumen489 halamanCourt Rules Expropriation for Private Subdivision Not Valid Public UseNico FerrerBelum ada peringkat

- A Brief History of BankingDokumen42 halamanA Brief History of Bankingtasaduq70% (1)

- Invoice Artech010723 Artech Alliance Owners Association Artech RealtorsDokumen2 halamanInvoice Artech010723 Artech Alliance Owners Association Artech RealtorsPrasad SBelum ada peringkat

- Research ProposalDokumen11 halamanResearch ProposalQaiser Khalil100% (1)