Anda mungkin juga menyukai

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideDari EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideBelum ada peringkat

- How To Increase A Credit Score QuicklyDokumen15 halamanHow To Increase A Credit Score QuicklyJoel Curtis100% (2)

- AmazonRestrictedProductsList PDFDokumen44 halamanAmazonRestrictedProductsList PDFnitishhdesaiBelum ada peringkat

- Annual Payroll Processing TemplateDokumen71 halamanAnnual Payroll Processing TemplateChris ZSCBelum ada peringkat

- Cycle Time ImprovementDokumen134 halamanCycle Time ImprovementKuladeepa KrBelum ada peringkat

- General and Subsidiary Ledgers ExplainedDokumen57 halamanGeneral and Subsidiary Ledgers ExplainedSavage NicoBelum ada peringkat

- Accounting for Price Level Changes ExplainedDokumen5 halamanAccounting for Price Level Changes ExplainedIndu Gupta100% (1)

- Bonus Assignment 1Dokumen4 halamanBonus Assignment 1Zain Zulfiqar100% (2)

- Definition of InfletionDokumen2 halamanDefinition of InfletionKonika DudhatraBelum ada peringkat

- Price Level ChangesDokumen7 halamanPrice Level Changestwyn774918100% (1)

- Inflation Accounting: BY, Nadeem Zehera Prathiksha Pooja J Raheela Banu Ramya JDokumen36 halamanInflation Accounting: BY, Nadeem Zehera Prathiksha Pooja J Raheela Banu Ramya JLikitha T AppajiBelum ada peringkat

- Price Level AccountingDokumen3 halamanPrice Level AccountingRajveer Singh Sekhon100% (2)

- Reliabiliity and AccuracyDokumen6 halamanReliabiliity and AccuracyReiner PrayogaBelum ada peringkat

- Unit 4 Accounting For Price Level ChangesDokumen5 halamanUnit 4 Accounting For Price Level ChangesKunja Bihari PadhiBelum ada peringkat

- Accounting Theory - Summary Chapter 6Dokumen10 halamanAccounting Theory - Summary Chapter 6Boby Kristanto ChandraBelum ada peringkat

- Accounting for InflationDokumen6 halamanAccounting for InflationkunjapBelum ada peringkat

- Financial ReportingDokumen7 halamanFinancial ReportingInnocent MollaBelum ada peringkat

- Inflation AccountingDokumen3 halamanInflation Accountingsunil.ctBelum ada peringkat

- Accounting For Price Level ChangesDokumen8 halamanAccounting For Price Level ChangesSonal RathhiBelum ada peringkat

- Hra Unit 4Dokumen19 halamanHra Unit 4World is GoldBelum ada peringkat

- Impact of Inflation On The Financial StatementsDokumen22 halamanImpact of Inflation On The Financial StatementsabbyplexxBelum ada peringkat

- Measurement Theory and Cost AllocationDokumen17 halamanMeasurement Theory and Cost AllocationYusuf RaharjaBelum ada peringkat

- Conventional AccountingDokumen2 halamanConventional AccountingChoi Minri0% (1)

- Price Level Accounting by Rekha - 5212Dokumen30 halamanPrice Level Accounting by Rekha - 5212Khesari Lal YadavBelum ada peringkat

- Acc PresentationDokumen24 halamanAcc PresentationjainrinkiBelum ada peringkat

- A Simple Definition of Income Measurement Is The Calculation of Profit or LossDokumen7 halamanA Simple Definition of Income Measurement Is The Calculation of Profit or LossKirosTeklehaimanotBelum ada peringkat

- InflationAccountingMethodsDokumen4 halamanInflationAccountingMethodsanjalikapoorBelum ada peringkat

- Inflation AccountingDokumen23 halamanInflation AccountingthejojoseBelum ada peringkat

- CORPORATE ACCOUNTING IA2-pdf 2Dokumen12 halamanCORPORATE ACCOUNTING IA2-pdf 2Surya GowdaBelum ada peringkat

- 2.aklesia Kefelegn - Essay On InflationDokumen13 halaman2.aklesia Kefelegn - Essay On InflationTeddishoBelum ada peringkat

- Chapter One Introdutoin: 1.1. What Is Cost Accounting?Dokumen156 halamanChapter One Introdutoin: 1.1. What Is Cost Accounting?NatnaelBelum ada peringkat

- Important Accounting Concepts Mini Thesis Syndicate 7Dokumen20 halamanImportant Accounting Concepts Mini Thesis Syndicate 7rifkiBelum ada peringkat

- F & M AccountingDokumen6 halamanF & M AccountingCherry PieBelum ada peringkat

- Accrual Accounting and Financial Reporting ConceptsDokumen4 halamanAccrual Accounting and Financial Reporting ConceptsGesa StephenBelum ada peringkat

- Section - A 201: (I) Discuss About Accounting PrinciplesDokumen7 halamanSection - A 201: (I) Discuss About Accounting PrinciplesPrem KumarBelum ada peringkat

- Accounting Standard-1: Disclosure of Accounting PoliciesDokumen8 halamanAccounting Standard-1: Disclosure of Accounting Policieskeshvika singlaBelum ada peringkat

- Accountancy Notes ch-2Dokumen4 halamanAccountancy Notes ch-2Ansh JaiswalBelum ada peringkat

- Current Cost Accounting (CCA) Technique - Inflation Accounting - Play AccountingDokumen2 halamanCurrent Cost Accounting (CCA) Technique - Inflation Accounting - Play AccountingVikas Singh0% (1)

- 100 006 Measuring Business IncomeDokumen4 halaman100 006 Measuring Business IncomeaymieBelum ada peringkat

- Measurement Theory Chapter SummaryThe title provides a concise yet informative summary of the document content. It mentions the key chapter topic of "Measurement TheoryDokumen17 halamanMeasurement Theory Chapter SummaryThe title provides a concise yet informative summary of the document content. It mentions the key chapter topic of "Measurement TheoryYusuf Raharja100% (1)

- Cost AccountingDokumen12 halamanCost AccountingMeenakshi SeerviBelum ada peringkat

- The impact of income measurement theories on financial reportingDokumen13 halamanThe impact of income measurement theories on financial reportingMusa oforiBelum ada peringkat

- Bafs NotesDokumen5 halamanBafs Notes小孩葉Belum ada peringkat

- As 1 Disclosure of Accounting PoliciesDokumen38 halamanAs 1 Disclosure of Accounting PoliciesPrashant SoniBelum ada peringkat

- Cost & Management AccountingDokumen6 halamanCost & Management Accountingshivam goyalBelum ada peringkat

- Course Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Inflation Accounting Faculty: Dr. Gousia ShahDokumen14 halamanCourse Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Inflation Accounting Faculty: Dr. Gousia ShahLeo SaimBelum ada peringkat

- Cost and Financial AccountingDokumen9 halamanCost and Financial AccountingSrikant RaoBelum ada peringkat

- Rules and principles govern accountingDokumen22 halamanRules and principles govern accountingMartha AntonBelum ada peringkat

- Cost AccountingDokumen26 halamanCost AccountingdivinamariageorgeBelum ada peringkat

- Task 2Dokumen18 halamanTask 2Yashmi BhanderiBelum ada peringkat

- Study G Fs Ratio 808Dokumen3 halamanStudy G Fs Ratio 808Marygrace MillerBelum ada peringkat

- Sta. Ana AsynchTaskNov16Dokumen2 halamanSta. Ana AsynchTaskNov16John Christopher Sta AnaBelum ada peringkat

- Accounting Notes ALL at MBADokumen43 halamanAccounting Notes ALL at MBABabasab Patil (Karrisatte)Belum ada peringkat

- Generally Accepted Accounting Principles - GAAP: Concept DefinitionDokumen8 halamanGenerally Accepted Accounting Principles - GAAP: Concept DefinitiontasyriqBelum ada peringkat

- Issues in Financial Reporting Izza Urooj Sap Id 6884 Sir AmanullahDokumen11 halamanIssues in Financial Reporting Izza Urooj Sap Id 6884 Sir AmanullahAli AwanBelum ada peringkat

- MB41 Ans IDokumen14 halamanMB41 Ans IAloke SharmaBelum ada peringkat

- Limitations of Historical Cost AccountingDokumen20 halamanLimitations of Historical Cost Accountinghamarshi2010100% (2)

- Accounting For Price Level Changes: Concept MethodsDokumen4 halamanAccounting For Price Level Changes: Concept MethodsLucky'rishika' UpadhyayBelum ada peringkat

- ACCT 1005 Summary Notes 1.2 Accounting Concepts and PrinciplesDokumen3 halamanACCT 1005 Summary Notes 1.2 Accounting Concepts and PrinciplesShamark EdwardsBelum ada peringkat

- Finac Ass NyashaDokumen8 halamanFinac Ass NyashaNyasha mudapakatiBelum ada peringkat

- Acc 1Dokumen3 halamanAcc 1navi4s3Belum ada peringkat

- Draft 1Dokumen7 halamanDraft 1John Ray RonaBelum ada peringkat

- CPP Method Explained for Inflationary AccountingDokumen3 halamanCPP Method Explained for Inflationary AccountingVivek SaurabhBelum ada peringkat

- Companies Act-: Lecture 4 Revision NotesDokumen5 halamanCompanies Act-: Lecture 4 Revision NotesAnisah HabibBelum ada peringkat

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsDari EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsBelum ada peringkat

- Creative Side and Message StrategyDokumen18 halamanCreative Side and Message StrategyKuladeepa KrBelum ada peringkat

- 02 CopywritingDokumen22 halaman02 CopywritingZonaira PervezBelum ada peringkat

- AFR February 01-15-2016-LrDokumen28 halamanAFR February 01-15-2016-LrKuladeepa KrBelum ada peringkat

- BTM 2014 - Mba Sem IV - Chapter 00 - PrologueDokumen10 halamanBTM 2014 - Mba Sem IV - Chapter 00 - PrologueKuladeepa KrBelum ada peringkat

- Framework For Assessing Multinational StrategiesDokumen10 halamanFramework For Assessing Multinational StrategiesKuladeepa KrBelum ada peringkat

- Hetzel 93Dokumen106 halamanHetzel 93Kuladeepa KrBelum ada peringkat

- Combining Commercial and Technological StrengthDokumen2 halamanCombining Commercial and Technological StrengthKuladeepa KrBelum ada peringkat

- What Is A Good Brand Name?Dokumen2 halamanWhat Is A Good Brand Name?Kuladeepa KrBelum ada peringkat

- Balance Sheet 2012Dokumen1 halamanBalance Sheet 2012Kuladeepa KrBelum ada peringkat

- DigitalIndia 4Dokumen1 halamanDigitalIndia 4Kuladeepa KrBelum ada peringkat

- S.No Description Cash Credit TotalDokumen1 halamanS.No Description Cash Credit TotalKuladeepa KrBelum ada peringkat

- Fund Flow Statement PresentationDokumen22 halamanFund Flow Statement PresentationKuladeepa KrBelum ada peringkat

- BookDokumen3 halamanBookKuladeepa KrBelum ada peringkat

- Concept of Child AbuseDokumen4 halamanConcept of Child AbuseKuladeepa KrBelum ada peringkat

- Finacial Reporting and Analyis Assignment-1Dokumen7 halamanFinacial Reporting and Analyis Assignment-1Kuladeepa KrBelum ada peringkat

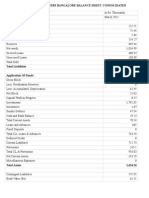

- Target Advertisers Bangalore Balance Sheet-ConsolidatedDokumen2 halamanTarget Advertisers Bangalore Balance Sheet-ConsolidatedKuladeepa KrBelum ada peringkat

- Module 2Dokumen51 halamanModule 2Kuladeepa KrBelum ada peringkat

- Balance Sheet 2012Dokumen1 halamanBalance Sheet 2012Kuladeepa KrBelum ada peringkat

- BookDokumen3 halamanBookKuladeepa KrBelum ada peringkat

- Concept of Child AbuseDokumen4 halamanConcept of Child AbuseKuladeepa KrBelum ada peringkat

- Balance Sheet 2011Dokumen1 halamanBalance Sheet 2011Kuladeepa KrBelum ada peringkat

- Fund Flow Statement PresentationDokumen22 halamanFund Flow Statement PresentationKuladeepa KrBelum ada peringkat

- Book 2Dokumen2 halamanBook 2Kuladeepa KrBelum ada peringkat

- 1Hwzrun0Hgld, Qyhvwphqwv: 3uhylrxv HduvDokumen2 halaman1Hwzrun0Hgld, Qyhvwphqwv: 3uhylrxv HduvKuladeepa KrBelum ada peringkat

- Module 1Dokumen58 halamanModule 1Kuladeepa KrBelum ada peringkat

- Questionnaire Behavior of Customer'S Towards Nestle ProductsDokumen4 halamanQuestionnaire Behavior of Customer'S Towards Nestle ProductsKuladeepa KrBelum ada peringkat

- Bank Service Questionnaire FeedbackDokumen5 halamanBank Service Questionnaire FeedbackKuladeepa KrBelum ada peringkat

- Visitor SurveyDokumen6 halamanVisitor SurveyvarunbandiBelum ada peringkat

- Shrunga M N: Career ObjectiveDokumen3 halamanShrunga M N: Career ObjectiveKuladeepa KrBelum ada peringkat

- Shapiro CHAPTER 3 Altered SolutionsDokumen17 halamanShapiro CHAPTER 3 Altered Solutionsjimmy_chou1314100% (1)

- Acct Statement XX6669 23062023Dokumen66 halamanAcct Statement XX6669 23062023Suraj KoratkarBelum ada peringkat

- E 14-6 Acquisition-Excess Allocation and Amortization EffectDokumen13 halamanE 14-6 Acquisition-Excess Allocation and Amortization EffectRizkina MoelBelum ada peringkat

- Development Power of Attorny After Registration of Development AgreementDokumen12 halamanDevelopment Power of Attorny After Registration of Development AgreementAchyut Bhattacharya100% (1)

- An Overview of The Shariah Issues of Rahn Based Financing in MalaysiaDokumen15 halamanAn Overview of The Shariah Issues of Rahn Based Financing in MalaysiaPekasam LautBelum ada peringkat

- Practice Problems On Incidence of TaxDokumen3 halamanPractice Problems On Incidence of TaxPratik DesaiBelum ada peringkat

- AFAR-02 (Partnership Dissolution & Liquidation)Dokumen15 halamanAFAR-02 (Partnership Dissolution & Liquidation)Jennelyn CapenditBelum ada peringkat

- Tax CalculatorDokumen2 halamanTax CalculatorJeffree Lann AlvarezBelum ada peringkat

- Basic Concepts 1Dokumen42 halamanBasic Concepts 1puneet80% (5)

- Rich Poor Foolish ExcerptDokumen35 halamanRich Poor Foolish ExcerptRahul SharmaBelum ada peringkat

- PDFDokumen2 halamanPDFParvez KhanBelum ada peringkat

- A Compilation of The Messages and Papers of The Presidents Volume 8, Part 2: Grover Cleveland by Cleveland, Grover, 1837-1908Dokumen387 halamanA Compilation of The Messages and Papers of The Presidents Volume 8, Part 2: Grover Cleveland by Cleveland, Grover, 1837-1908Gutenberg.orgBelum ada peringkat

- Inter IKEA Holding B.V. Annual Report FY18 Financial StatementsDokumen4 halamanInter IKEA Holding B.V. Annual Report FY18 Financial StatementsaretaBelum ada peringkat

- Investment Banking - Securities Dealing in The US Industry ReportDokumen42 halamanInvestment Banking - Securities Dealing in The US Industry ReportEldar Sedaghatparast SalehBelum ada peringkat

- Forex ICAI ModifiedDokumen34 halamanForex ICAI Modifiedantim routBelum ada peringkat

- What Do Financial Managers DoDokumen5 halamanWhat Do Financial Managers DoSerena Van Der WoodsenBelum ada peringkat

- Lecture 9 - International Investment and Financing DecisionDokumen22 halamanLecture 9 - International Investment and Financing DecisionAlice LowBelum ada peringkat

- Funding African InfrastructureDokumen4 halamanFunding African InfrastructureKofikoduahBelum ada peringkat

- Dec ChallanDokumen1 halamanDec ChallanMoon MunawarBelum ada peringkat

- Weather Bureau Credit Ccoperative: Science Garden Complex, Agham Road Diliman, Quezon City DateDokumen1 halamanWeather Bureau Credit Ccoperative: Science Garden Complex, Agham Road Diliman, Quezon City DateAugieray D. MercadoBelum ada peringkat

- Guiding Principles of Monetary Administration by The Bangko SentralDokumen8 halamanGuiding Principles of Monetary Administration by The Bangko SentralEuphoria BTSBelum ada peringkat

- Uang NewDokumen23 halamanUang Newjhosi yosiBelum ada peringkat

- PledgeDokumen14 halamanPledgeShareen AnwarBelum ada peringkat

- Unit 1: Derivatives - FuturesDokumen90 halamanUnit 1: Derivatives - Futuresseema mundaleBelum ada peringkat

- Chapter 24Dokumen20 halamanChapter 24Daphne PerezBelum ada peringkat