Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Advanced Accounting by Antonio Dayag SolmanDokumen230 halamanAdvanced Accounting by Antonio Dayag SolmanNorfaidah Didato Gogo100% (4)

- Disposal of Subsidiary PDFDokumen9 halamanDisposal of Subsidiary PDFCourage KanyonganiseBelum ada peringkat

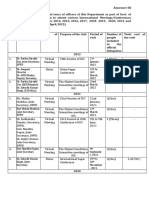

- Annexure IDokumen3 halamanAnnexure IchengadBelum ada peringkat

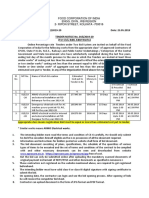

- Notice Inviting Bids For Sale of Raw Rice Ga To Bulk Consumers/Traders Under Omss (D) Bulk Through E-AuctionDokumen1 halamanNotice Inviting Bids For Sale of Raw Rice Ga To Bulk Consumers/Traders Under Omss (D) Bulk Through E-AuctionchengadBelum ada peringkat

- Annex Ure IVDokumen2 halamanAnnex Ure IVchengadBelum ada peringkat

- Annexure IIIDokumen13 halamanAnnexure IIIchengadBelum ada peringkat

- NIT Rice 27.08.18Dokumen1 halamanNIT Rice 27.08.18chengadBelum ada peringkat

- MTF Rice 27.08.18 PDFDokumen13 halamanMTF Rice 27.08.18 PDFchengadBelum ada peringkat

- Notice Inviting Financial Bids For Sale of Wheat To Bulk Consumers/Traders Under Omss (D) Bulk Through E-AuctionDokumen1 halamanNotice Inviting Financial Bids For Sale of Wheat To Bulk Consumers/Traders Under Omss (D) Bulk Through E-AuctionchengadBelum ada peringkat

- Food Corporation of India Regional Office JammuDokumen13 halamanFood Corporation of India Regional Office JammuchengadBelum ada peringkat

- NIT Dt.23.05.19 (FSD Kathua)Dokumen3 halamanNIT Dt.23.05.19 (FSD Kathua)chengadBelum ada peringkat

- NIT Dt.23.05.19 (FSD Srinagar)Dokumen3 halamanNIT Dt.23.05.19 (FSD Srinagar)chengadBelum ada peringkat

- NIT dt.23.05.19 PDFDokumen3 halamanNIT dt.23.05.19 PDFchengadBelum ada peringkat

- Tender NoticeDokumen2 halamanTender NoticechengadBelum ada peringkat

- NIT 01E 2019-20 (Electrical Work)Dokumen4 halamanNIT 01E 2019-20 (Electrical Work)chengadBelum ada peringkat

- Food Corporation of India Regional Office: JammuDokumen3 halamanFood Corporation of India Regional Office: JammuchengadBelum ada peringkat

- Rice Depotwise QuantityDokumen1 halamanRice Depotwise QuantitychengadBelum ada peringkat

- Food Corporation of India: Ph. No. 0135-2970038, 0135-2665993 e Mail: Gmukfci@gov - inDokumen1 halamanFood Corporation of India: Ph. No. 0135-2970038, 0135-2665993 e Mail: Gmukfci@gov - inchengadBelum ada peringkat

- Wheat Depotwise QuantityDokumen1 halamanWheat Depotwise QuantitychengadBelum ada peringkat

- MTF Wheat 03 - 10 - 2019Dokumen17 halamanMTF Wheat 03 - 10 - 2019chengadBelum ada peringkat

- Wheat MTF - 9Dokumen13 halamanWheat MTF - 9chengadBelum ada peringkat

- Food Corporation of India Regional Office: Kesavadasapuram Pattom Palace P.O: Thiruvananthapuram 695 004Dokumen2 halamanFood Corporation of India Regional Office: Kesavadasapuram Pattom Palace P.O: Thiruvananthapuram 695 004chengadBelum ada peringkat

- MTF Wheat Dt.14.01.16Dokumen11 halamanMTF Wheat Dt.14.01.16chengadBelum ada peringkat

- Rice Guidelines 8Dokumen5 halamanRice Guidelines 8chengadBelum ada peringkat

- fci Date of NIT Last Date For Depositing EMD Starting Date and Time For Online Bidding End Date and Time For Online BiddingDokumen1 halamanfci Date of NIT Last Date For Depositing EMD Starting Date and Time For Online Bidding End Date and Time For Online BiddingchengadBelum ada peringkat

- MTF Rice - 9Dokumen12 halamanMTF Rice - 9chengadBelum ada peringkat

- 2.MTF Rice - 6Dokumen18 halaman2.MTF Rice - 6chengadBelum ada peringkat

- MTF Wheat 16.08.2019Dokumen17 halamanMTF Wheat 16.08.2019chengadBelum ada peringkat

- 61 - Ee11 - 2019 MTFDokumen12 halaman61 - Ee11 - 2019 MTFchengadBelum ada peringkat

- 61 - Ee11 - 2019 NITDokumen1 halaman61 - Ee11 - 2019 NITchengadBelum ada peringkat

- MTF of Wheat - 5Dokumen18 halamanMTF of Wheat - 5chengadBelum ada peringkat

- Tender NIT No - 03 2017-18 Website-BSWCDokumen4 halamanTender NIT No - 03 2017-18 Website-BSWCchengadBelum ada peringkat

- Passport To Success Solutions - L3 AccountingDokumen52 halamanPassport To Success Solutions - L3 Accountingfaifai0714Belum ada peringkat

- Investments (FAR)Dokumen30 halamanInvestments (FAR)James CantorneBelum ada peringkat

- Dividend PolicyDokumen9 halamanDividend PolicyKavita PoddarBelum ada peringkat

- PDS Debit Card enDokumen2 halamanPDS Debit Card enYus RieyBelum ada peringkat

- Cash Receipt PDFDokumen1 halamanCash Receipt PDFMarsa ArrahmanBelum ada peringkat

- Afar - Mr. AccountingDokumen11 halamanAfar - Mr. AccountingGeorizz Kristine EscañoBelum ada peringkat

- Sun Mobiles and Electronics Prop S Mohamed Rafi No.19 Abs Complex Ground Floor Mettur Road Erode 638011 Profit and Loss Account 01.04.2015 TO 31.03.2016 Particulars Rs. Particulars RsDokumen6 halamanSun Mobiles and Electronics Prop S Mohamed Rafi No.19 Abs Complex Ground Floor Mettur Road Erode 638011 Profit and Loss Account 01.04.2015 TO 31.03.2016 Particulars Rs. Particulars RssamaadhuBelum ada peringkat

- GINGER CHIPS Laurilla EnterpriseDokumen29 halamanGINGER CHIPS Laurilla Enterprisejanjantuazon24Belum ada peringkat

- Use The Following Information To Answer The Next Four QuestionsDokumen5 halamanUse The Following Information To Answer The Next Four QuestionsAkshadaBelum ada peringkat

- Cost of CapitalDokumen23 halamanCost of CapitalnigemahamatiBelum ada peringkat

- Brief Exercise - Solutions - Chapter 9Dokumen3 halamanBrief Exercise - Solutions - Chapter 9Quynh Nguyen HuongBelum ada peringkat

- Date AND Time Learning Area Learning Competencie S Learning Tasks Mode of DeliveryDokumen4 halamanDate AND Time Learning Area Learning Competencie S Learning Tasks Mode of DeliveryAvegail SayonBelum ada peringkat

- Investment Management of BanksDokumen28 halamanInvestment Management of BanksGragnor PrideBelum ada peringkat

- Project Topics For Mutual Funds: A Study of Selected Indian Public Sector and Private Sector Banks Using Camel ModelDokumen3 halamanProject Topics For Mutual Funds: A Study of Selected Indian Public Sector and Private Sector Banks Using Camel ModelShashank Pal100% (1)

- Financial Modeling Chapter 1Dokumen36 halamanFinancial Modeling Chapter 1Sabaa if100% (1)

- Cashflow AnalysisDokumen19 halamanCashflow Analysisgl101Belum ada peringkat

- Quiz 3Dokumen4 halamanQuiz 3ErionBelum ada peringkat

- Cfas Mock Test PDFDokumen71 halamanCfas Mock Test PDFRose Dumadaug50% (2)

- Checklist of Key Figures: Inancial Ccounting Ools FOR Usiness Ecision Aking Eventh DitionDokumen15 halamanChecklist of Key Figures: Inancial Ccounting Ools FOR Usiness Ecision Aking Eventh Ditionkindergarten tutorialBelum ada peringkat

- Results Reporter: Multiple Choice QuizDokumen4 halamanResults Reporter: Multiple Choice QuizVinit ChawlaBelum ada peringkat

- BASIC FINANCE qm1Dokumen3 halamanBASIC FINANCE qm1Erica GaytosBelum ada peringkat

- Bajaj Electrical: (Bajele)Dokumen9 halamanBajaj Electrical: (Bajele)premBelum ada peringkat

- CH 4 MCQ AccDokumen23 halamanCH 4 MCQ AccLONE WOLF TECHBelum ada peringkat

- Abbott Company and Its Financial Statement Analysis Using Ratios Abbott CompanyDokumen17 halamanAbbott Company and Its Financial Statement Analysis Using Ratios Abbott CompanyMaryam EjazBelum ada peringkat

- Reading 42 Fixed-Income Securities - Defining ElementsDokumen14 halamanReading 42 Fixed-Income Securities - Defining ElementsAmineBelum ada peringkat

- CFAS Reviewer - Module 6Dokumen14 halamanCFAS Reviewer - Module 6Lizette Janiya SumantingBelum ada peringkat

- Corpo QuamtoDokumen38 halamanCorpo QuamtomichelleBelum ada peringkat

- Relative Strengths and Weaknesses of Financial Analysis Methodologie1Dokumen9 halamanRelative Strengths and Weaknesses of Financial Analysis Methodologie1Anastasiia SidorovaBelum ada peringkat