Anda mungkin juga menyukai

- MCQ Single EntryDokumen11 halamanMCQ Single EntryAdi100% (8)

- Materi Ibu Ningsih - Webinar IAPI-ACCA "Key Audit Matters in The Context of The New Audit Regulation"Dokumen37 halamanMateri Ibu Ningsih - Webinar IAPI-ACCA "Key Audit Matters in The Context of The New Audit Regulation"sus anto100% (1)

- Punj Bank StatementDokumen2 halamanPunj Bank StatementAmrit TejaniBelum ada peringkat

- Reporting Internal Audit ResultsDokumen5 halamanReporting Internal Audit Resultsannisa radiBelum ada peringkat

- Tips On Writing Internal Audit ReportsDokumen5 halamanTips On Writing Internal Audit ReportsSohail Iftikhar100% (1)

- Kedudukan DPRDDokumen14 halamanKedudukan DPRDDeni Budiani PermanaBelum ada peringkat

- Adjusting Entries for Diana MargalloDokumen37 halamanAdjusting Entries for Diana MargalloKyle Ronquillo50% (2)

- Forensic Accounting - Fraud Examination Sesi 1 Pengertian Akuntansi ForensikDokumen31 halamanForensic Accounting - Fraud Examination Sesi 1 Pengertian Akuntansi ForensikBaMbAng HartaDIBelum ada peringkat

- IAS 16 and IAS 38Dokumen84 halamanIAS 16 and IAS 38Danu DorinaBelum ada peringkat

- IC COSO dan 5 Pilar GCGDokumen159 halamanIC COSO dan 5 Pilar GCGIlham Ahmad RosyadiBelum ada peringkat

- Qia Practice QuestionDokumen0 halamanQia Practice QuestionZiaul HuqBelum ada peringkat

- Full DisclosureDokumen22 halamanFull DisclosurepanjiBelum ada peringkat

- Rizky Purwanti Akhmad Riduwan: Pengaruh Konservatisme Akuntansi Terhadap Nilai PerusahaanDokumen17 halamanRizky Purwanti Akhmad Riduwan: Pengaruh Konservatisme Akuntansi Terhadap Nilai PerusahaanRambu YanaBelum ada peringkat

- Jurnal Efektivitas Penggunaan Anggaran Pendapatan Dan Belanja Daerah (APBD) Dalam Program Pengentasan Kemiskinan Di Kecamatan Bantan KabupatenDokumen14 halamanJurnal Efektivitas Penggunaan Anggaran Pendapatan Dan Belanja Daerah (APBD) Dalam Program Pengentasan Kemiskinan Di Kecamatan Bantan Kabupatendhedi 2906Belum ada peringkat

- Peran Internal Auditor SBG Konsultan & Katalis V (1) .2Dokumen25 halamanPeran Internal Auditor SBG Konsultan & Katalis V (1) .2Retno Triwahyuni ManullangBelum ada peringkat

- Dana Desa Fraud HexagonDokumen24 halamanDana Desa Fraud Hexagoneko triyantoBelum ada peringkat

- Sosialisasi Perubahan Format Baru Ujian CA - 18 Nov 2021Dokumen47 halamanSosialisasi Perubahan Format Baru Ujian CA - 18 Nov 2021VerySonyIndraSurotoBelum ada peringkat

- Artikel Hukum Keuangan NegaraDokumen11 halamanArtikel Hukum Keuangan NegaraMuhammad Fadil SidqiBelum ada peringkat

- Peran Inspektorat Dalam Pelaksanaan Sistem PengawasanDokumen10 halamanPeran Inspektorat Dalam Pelaksanaan Sistem PengawasanChacand ChandraBelum ada peringkat

- M.A 1-Karakteristik Akuntansi Manajemen - NewDokumen27 halamanM.A 1-Karakteristik Akuntansi Manajemen - Newirsa100% (1)

- Sambutan Menteri PANRB November-DesemberDokumen43 halamanSambutan Menteri PANRB November-DesemberAmelia Henisyahputri100% (1)

- Forensic Auditing: The Audit of The Future, Today: Instructor: Ron Durkin, CFE, CPA/CFF, CIRADokumen54 halamanForensic Auditing: The Audit of The Future, Today: Instructor: Ron Durkin, CFE, CPA/CFF, CIRADINGDINGWALABelum ada peringkat

- Godfrey Hodgson Holmes TarcaDokumen27 halamanGodfrey Hodgson Holmes Tarcalala azzahraBelum ada peringkat

- Tutorial Letter 103/0/2023: FAC4862/NFA4862/ZFA4862Dokumen112 halamanTutorial Letter 103/0/2023: FAC4862/NFA4862/ZFA4862THABO CLARENCE MohleleBelum ada peringkat

- Efektifitas CSRDokumen12 halamanEfektifitas CSRMohamad ReezaBelum ada peringkat

- Effect of Strategic Planning on Hospital PerformanceDokumen10 halamanEffect of Strategic Planning on Hospital PerformanceIKA FADHILAH BEA100% (1)

- DJA - Paparan Dir SP TGL 12 April - NETDokumen36 halamanDJA - Paparan Dir SP TGL 12 April - NETFaslan Syam SajiahBelum ada peringkat

- ID Pengaruh Pengelolaan Barang Milik DaerahDokumen11 halamanID Pengaruh Pengelolaan Barang Milik DaerahAnonymous SaxoCY7vGR100% (1)

- Academic TranscriptDokumen1 halamanAcademic TranscriptYayan BeuweumBelum ada peringkat

- Jurnal Kemandirian Keuangan DaerahDokumen28 halamanJurnal Kemandirian Keuangan Daerahsaragih88100% (3)

- Optimasi Algoritma Naive Bayes Menggunakan Metode Cross Validation Untuk Meningkatkan Akurasi Prediksi Tingkat Kelulusan Tepat WaktuDokumen8 halamanOptimasi Algoritma Naive Bayes Menggunakan Metode Cross Validation Untuk Meningkatkan Akurasi Prediksi Tingkat Kelulusan Tepat WaktuAhmadKomarudinBelum ada peringkat

- Not Verified Yet: Agus DwiyantoDokumen3 halamanNot Verified Yet: Agus DwiyantoMardi OnoBelum ada peringkat

- Strategi Bisnis KorporasiDokumen41 halamanStrategi Bisnis KorporasiAliMu'minHarahapBelum ada peringkat

- Laporan SkripsiDokumen15 halamanLaporan SkripsiYokeSetiawanBelum ada peringkat

- Audit Sistem Informasi Manajemen Aset Berdasarkan Perspektif Proses Bisnis Internal Balanced Scorecard Dan Standar Cobit 4.1Dokumen8 halamanAudit Sistem Informasi Manajemen Aset Berdasarkan Perspektif Proses Bisnis Internal Balanced Scorecard Dan Standar Cobit 4.1Roro Asri IsmayaBelum ada peringkat

- CHAN, James L. Government Accounting - An Assessment of Theory, Purposes and StandardsDokumen9 halamanCHAN, James L. Government Accounting - An Assessment of Theory, Purposes and StandardsHeloisaBianquiniBelum ada peringkat

- Fiscal DecentralizationDokumen116 halamanFiscal DecentralizationRizky Dwi PutriBelum ada peringkat

- Demokrasi DeliberatifDokumen7 halamanDemokrasi Deliberatifnadifa salsabilaBelum ada peringkat

- Analisis Penerapan Digitalisasi Online Arsip (Doa) Pegawai Pada Pengelolaan Tata Naskah Aparatur Sipil Negara Badan Kepegawaian Dan Pengembangan Sumber Daya Manusia (BKPSDM) Kabupaten BoneDokumen8 halamanAnalisis Penerapan Digitalisasi Online Arsip (Doa) Pegawai Pada Pengelolaan Tata Naskah Aparatur Sipil Negara Badan Kepegawaian Dan Pengembangan Sumber Daya Manusia (BKPSDM) Kabupaten Boneramadi ramBelum ada peringkat

- Documenting Result Through Process Modeling and WorkpapersDokumen19 halamanDocumenting Result Through Process Modeling and Workpaperswulan ruhiyyihBelum ada peringkat

- Auditing Fair Value Measurements and DisclosuresDokumen93 halamanAuditing Fair Value Measurements and DisclosuresddeliuBelum ada peringkat

- Implementasi 5 S Inovasi Good Governance Dalam Pelayanan PublikDokumen15 halamanImplementasi 5 S Inovasi Good Governance Dalam Pelayanan PublikFabian Ande'WaBelum ada peringkat

- Kelompok 2 Professional StandardDokumen45 halamanKelompok 2 Professional StandardRevanty IryaniBelum ada peringkat

- Organizational Citizenship Behaviour (OCB)Dokumen19 halamanOrganizational Citizenship Behaviour (OCB)DandiwidanaaBelum ada peringkat

- Analisis Faktor-Faktor Yang Mempengaruhi Kualitas Hasil Audit Di Lingkungan Pemerintah DaerahDokumen23 halamanAnalisis Faktor-Faktor Yang Mempengaruhi Kualitas Hasil Audit Di Lingkungan Pemerintah DaerahDiditKurniawan100% (1)

- Pengawasan Internal, Pengawasan Eksternal Dan Kinerja PemerintahDokumen18 halamanPengawasan Internal, Pengawasan Eksternal Dan Kinerja PemerintahAditiya Nugraha JatiBelum ada peringkat

- Audit Sistem InformasiDokumen13 halamanAudit Sistem Informasiraisa.kirana14Belum ada peringkat

- Jeong-Big Six Auditors and Audit Quality-The Korean EvidenceDokumen22 halamanJeong-Big Six Auditors and Audit Quality-The Korean EvidenceLivia MarsaBelum ada peringkat

- Resume Chapter 4: TRANSACTIONAL PROCESSING AND INTERNAL CONTROL PROCESSDokumen4 halamanResume Chapter 4: TRANSACTIONAL PROCESSING AND INTERNAL CONTROL PROCESSaryantiyessyBelum ada peringkat

- Peran Chief Information Officer Dalam Kelembagaan PDFDokumen22 halamanPeran Chief Information Officer Dalam Kelembagaan PDFmacan meongBelum ada peringkat

- 2-Spreading The Gospel of EfficiencyDokumen18 halaman2-Spreading The Gospel of EfficiencythayumanavarkannanBelum ada peringkat

- RBIA Overview and PrinciplesDokumen58 halamanRBIA Overview and PrinciplesSiti Fatimah DBelum ada peringkat

- Proposal Tesis Harjun HatmaDokumen81 halamanProposal Tesis Harjun HatmaharjunBelum ada peringkat

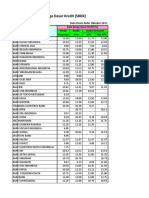

- Suku Bunga Dasar Kredit November 2011Dokumen284 halamanSuku Bunga Dasar Kredit November 2011Ida Ayu ChandrayaniiBelum ada peringkat

- Pengantar Paradigma Dan Teori Ilmu AdmDokumen50 halamanPengantar Paradigma Dan Teori Ilmu AdmDyah RahmayantiBelum ada peringkat

- Statistik DeskriptifDokumen33 halamanStatistik Deskriptifnurul shabrinaBelum ada peringkat

- ID Pengaruh Penggunaan Media Sosial Facebook Terhadap Perilaku Prososial Remaja DiDokumen15 halamanID Pengaruh Penggunaan Media Sosial Facebook Terhadap Perilaku Prososial Remaja DiM Saidi Azuhar Basri100% (1)

- Kajian Pengelolaan AsetDokumen21 halamanKajian Pengelolaan AsetEdi SetiawanBelum ada peringkat

- Analysis of Accounting Research Trends in Behavioral Journal (1998-2003Dokumen15 halamanAnalysis of Accounting Research Trends in Behavioral Journal (1998-2003Alhamdulillah HirrabbilngalaminBelum ada peringkat

- ID Kepemimpinan Transformasional Dalam KontDokumen26 halamanID Kepemimpinan Transformasional Dalam Kontnova aninsaBelum ada peringkat

- Jurnal Akuntansi PemerintahDokumen16 halamanJurnal Akuntansi PemerintahNastia Putri PertiwiBelum ada peringkat

- 127-Article Text-1077-1-10-20190930 PDFDokumen17 halaman127-Article Text-1077-1-10-20190930 PDFAldi WibawaBelum ada peringkat

- NestleDokumen3 halamanNestleArshad Baig MughalBelum ada peringkat

- E GovernanceDokumen18 halamanE GovernanceankituitBelum ada peringkat

- Introduction, Concepts and Overview of Financial Attest Audit ManualDokumen47 halamanIntroduction, Concepts and Overview of Financial Attest Audit ManualMayurdhvajsinh JadejaBelum ada peringkat

- Welcome TO A Talk ON Auditing StandardsDokumen36 halamanWelcome TO A Talk ON Auditing Standardssumit71sharmaBelum ada peringkat

- Tutor Statement Cash FlowDokumen3 halamanTutor Statement Cash Flowlavie nroseBelum ada peringkat

- KanchanDokumen84 halamanKanchanJyoti KumariBelum ada peringkat

- Completing The Accounting CycleDokumen3 halamanCompleting The Accounting CycleVia PacilunaBelum ada peringkat

- Closing Entries GuideDokumen9 halamanClosing Entries Guideapelina teresiaBelum ada peringkat

- Types of Accounts ExplainedDokumen25 halamanTypes of Accounts ExplainedSeung BatumbakalBelum ada peringkat

- Ahmed Dan Hossain 2010Dokumen8 halamanAhmed Dan Hossain 2010andrianyuniBelum ada peringkat

- Accounting Tutorial 2Dokumen6 halamanAccounting Tutorial 2Mega Pop LockerBelum ada peringkat

- PPM3023 Financial Services Semester 1 SESSION 2022/2023 Individual Assignment 1 E-BookDokumen10 halamanPPM3023 Financial Services Semester 1 SESSION 2022/2023 Individual Assignment 1 E-BookAqmar HarithBelum ada peringkat

- Abdc Journal ListDokumen192 halamanAbdc Journal ListRuwan Dileepa0% (1)

- Exercise Receivables 1Dokumen8 halamanExercise Receivables 1Asyraf AzharBelum ada peringkat

- Commission On Audit: Republic of The Philippines Regional Office No. VII Cebu CityDokumen31 halamanCommission On Audit: Republic of The Philippines Regional Office No. VII Cebu Citysandra bolokBelum ada peringkat

- University of The Western Cape Department of Accounting: Auditing 241 Test - 14 March 2020Dokumen4 halamanUniversity of The Western Cape Department of Accounting: Auditing 241 Test - 14 March 2020Hanifa OsmanBelum ada peringkat

- Chapter 2 AISDokumen3 halamanChapter 2 AISgailmissionBelum ada peringkat

- Intermediate Accounting (8th Edition) - Part 1 (Download Tai Tailieutuoi - Com)Dokumen10 halamanIntermediate Accounting (8th Edition) - Part 1 (Download Tai Tailieutuoi - Com)ABOLD 2021 LTVBelum ada peringkat

- Ratio Analysis of Orion Pharmaceuticals LimitedDokumen64 halamanRatio Analysis of Orion Pharmaceuticals Limitedrifat67% (3)

- Topic 1 - Audit - An OverviewDokumen22 halamanTopic 1 - Audit - An OverviewPara Sa PictureBelum ada peringkat

- CIE ANNUAL REPORT HIGHLIGHTSDokumen8 halamanCIE ANNUAL REPORT HIGHLIGHTSSana ZargarBelum ada peringkat

- Tally ERP 9 Shortcut Keys PDFDokumen6 halamanTally ERP 9 Shortcut Keys PDFDeepakKr79Belum ada peringkat

- Impact of IT on Accounting ProfessionDokumen11 halamanImpact of IT on Accounting ProfessionNBA EPICBelum ada peringkat

- Full Download Solution Manual For Intermediate Accounting Volume 1 12th Canadian by Kieso PDF Full ChapterDokumen36 halamanFull Download Solution Manual For Intermediate Accounting Volume 1 12th Canadian by Kieso PDF Full Chapterdribblerkickshawadoxw100% (17)

- Assignment IV Advanced Financial Accounting Chapter 4&5Dokumen6 halamanAssignment IV Advanced Financial Accounting Chapter 4&5Lidya AberaBelum ada peringkat

- Journals in ScopusDokumen119 halamanJournals in ScopusAmir Asraf0% (1)

- Chapter 5 PowerpointDokumen37 halamanChapter 5 Powerpointapi-248607804Belum ada peringkat

- 05 - ACC653 Questions WK1Dokumen5 halaman05 - ACC653 Questions WK1Camilo ToroBelum ada peringkat