Anda mungkin juga menyukai

- Qualifications and Qualities of A HR ManagerDokumen2 halamanQualifications and Qualities of A HR ManagernavreenBelum ada peringkat

- OBJECTIVE 1: "What Is A Price?" and Discuss The Importance of Pricing in Today's Fast Changing EnvironmentDokumen4 halamanOBJECTIVE 1: "What Is A Price?" and Discuss The Importance of Pricing in Today's Fast Changing EnvironmentRaphaela ArciagaBelum ada peringkat

- MARKETING Module 1 For StudentDokumen2 halamanMARKETING Module 1 For StudentJulianne VillanuevaBelum ada peringkat

- Types of Financial Decisions in Financial ManagementDokumen20 halamanTypes of Financial Decisions in Financial ManagementRahul Upadhayaya100% (1)

- The Nature and Importance of EntrepreneurshipDokumen18 halamanThe Nature and Importance of Entrepreneurshipsagar_nxBelum ada peringkat

- Risk and Rates of ReturnDokumen9 halamanRisk and Rates of ReturnMecyZ.GomezBelum ada peringkat

- Autocratic ModelDokumen5 halamanAutocratic ModelVenkatesh KesavanBelum ada peringkat

- Introduction To Credit ManagementDokumen48 halamanIntroduction To Credit ManagementHakdog KaBelum ada peringkat

- Chapter 2 The Nature of Small BusinessDokumen16 halamanChapter 2 The Nature of Small BusinessRoxanna Mhae Agarin VidamoBelum ada peringkat

- Characteristics of Organizational Change: Organizational Development Finals ReviewerDokumen4 halamanCharacteristics of Organizational Change: Organizational Development Finals ReviewerMarvin OngBelum ada peringkat

- The Theory and Practice of Corporate GovernanceDokumen25 halamanThe Theory and Practice of Corporate GovernanceMadihaBhatti100% (1)

- Unit-2 Security AnalysisDokumen26 halamanUnit-2 Security AnalysisJoshua JacksonBelum ada peringkat

- Features of Business PolicyDokumen2 halamanFeatures of Business PolicyjessaBelum ada peringkat

- Analyzing Resources and CapabilitiesDokumen50 halamanAnalyzing Resources and Capabilitiesfnazarov100% (1)

- Tools and Techniques of Financial AnalysisDokumen2 halamanTools and Techniques of Financial AnalysisAshis Kumar MohapatraBelum ada peringkat

- Analysis and Interpretation of Financial StatementDokumen30 halamanAnalysis and Interpretation of Financial StatementUgly DucklingBelum ada peringkat

- Cost of CapitalDokumen36 halamanCost of Capitalrambabu100% (1)

- Chapter 3Dokumen19 halamanChapter 3Amani Saeed100% (1)

- FABM 2 Module 4 Exercises Statement of Cash FlowDokumen3 halamanFABM 2 Module 4 Exercises Statement of Cash FlowJennifer NayveBelum ada peringkat

- Developing Pricing Strategies and ProgramsDokumen48 halamanDeveloping Pricing Strategies and Programsizdihar globalBelum ada peringkat

- Problems On LeverageDokumen2 halamanProblems On LeverageRituparna Nath100% (2)

- Chapter 1 Capital MarketsDokumen7 halamanChapter 1 Capital MarketssayBelum ada peringkat

- Risk and Return Chapter 5Dokumen55 halamanRisk and Return Chapter 5sundas younasBelum ada peringkat

- Bond Yield and Price PDFDokumen2 halamanBond Yield and Price PDFps12hayBelum ada peringkat

- Good Governance Chap 6 SlidesDokumen30 halamanGood Governance Chap 6 SlidesMaria Patrice MendozaBelum ada peringkat

- Samsung Mobile Devices: Running Head: Final Strategic Plan 1Dokumen21 halamanSamsung Mobile Devices: Running Head: Final Strategic Plan 1Darryn Urueta50% (2)

- Financial Management Chapter 4Dokumen16 halamanFinancial Management Chapter 4Muhammad Syanizam100% (1)

- 10 ReactionDokumen6 halaman10 ReactionKarl Jason Dolar CominBelum ada peringkat

- External Institutions of Corporate GovernanceDokumen3 halamanExternal Institutions of Corporate GovernanceJolina Ong100% (2)

- Operating Budget Garrison Chap009Dokumen81 halamanOperating Budget Garrison Chap009Malak Kinaan100% (2)

- 13corporate Social Responsibility in International BusinessDokumen23 halaman13corporate Social Responsibility in International BusinessShruti SharmaBelum ada peringkat

- Stages of Development of OrganizationsDokumen10 halamanStages of Development of OrganizationsXtin Ynot0% (1)

- Market StructureDokumen31 halamanMarket StructureAnuj SachdevBelum ada peringkat

- Stragic Management AssignmentDokumen37 halamanStragic Management Assignmentayub_balticBelum ada peringkat

- Marketing Management - Chapter 5Dokumen7 halamanMarketing Management - Chapter 5PRINTDESK by DanBelum ada peringkat

- What Is The Role of An Entrepreneur in Economic DevelopmentDokumen4 halamanWhat Is The Role of An Entrepreneur in Economic DevelopmentKapil VatsBelum ada peringkat

- C & B Module 1 - Introduction To CompensationDokumen15 halamanC & B Module 1 - Introduction To CompensationRuturaj patilBelum ada peringkat

- Capital Asset Pricing ModelDokumen4 halamanCapital Asset Pricing ModelGeorge Ayesa Sembereka Jr.Belum ada peringkat

- Case Study On BenefitsDokumen5 halamanCase Study On Benefits8130089011Belum ada peringkat

- Importance of Capital StructureDokumen2 halamanImportance of Capital StructureShruti JoseBelum ada peringkat

- Review QuestionsDokumen6 halamanReview QuestionsArjina Arji0% (1)

- Theory of FirmDokumen26 halamanTheory of FirmFahim JanBelum ada peringkat

- ST 303 Course PackDokumen54 halamanST 303 Course Packjaquelinesuperioridad lantajoBelum ada peringkat

- Solution To MBA Question 25Dokumen7 halamanSolution To MBA Question 25tallyho2906Belum ada peringkat

- Formation of Different Forms of Business OrganizationDokumen29 halamanFormation of Different Forms of Business OrganizationMiggy BambaBelum ada peringkat

- Porter Five Forces AnalysisDokumen6 halamanPorter Five Forces AnalysisadhilBelum ada peringkat

- Managerial Economics Unit 1 and 2Dokumen29 halamanManagerial Economics Unit 1 and 2Yash GargBelum ada peringkat

- Corporate, Business and Functional Level StrategyDokumen12 halamanCorporate, Business and Functional Level StrategyASK ME ANYTHING SMARTPHONEBelum ada peringkat

- Module 5 Production TheoryDokumen27 halamanModule 5 Production TheoryCharice Anne VillamarinBelum ada peringkat

- The Business Vision & Mission: Strategic Management: Concepts & Cases 12 Edition Fred DavidDokumen58 halamanThe Business Vision & Mission: Strategic Management: Concepts & Cases 12 Edition Fred DavidLsc LondonBelum ada peringkat

- Shagun Verma Attitude & Job SatisfactionDokumen56 halamanShagun Verma Attitude & Job SatisfactionShagun VermaBelum ada peringkat

- Business Policy & Strategic ManagementDokumen91 halamanBusiness Policy & Strategic ManagementAila Hope GeconcilloBelum ada peringkat

- PESTEL Analysis For Small BusinessesDokumen3 halamanPESTEL Analysis For Small BusinessesJohurul HoqueBelum ada peringkat

- Strategic Management ReviewerDokumen15 halamanStrategic Management ReviewersuperhoonieBelum ada peringkat

- Debate On Marketing ManagementDokumen3 halamanDebate On Marketing ManagementTang Zhen HaoBelum ada peringkat

- SWOT Analysis - Definition, Advantages and LimitationsDokumen4 halamanSWOT Analysis - Definition, Advantages and LimitationsMohd Aizuddin JerryBelum ada peringkat

- Leverage Chap 7 - PoliteknikDokumen83 halamanLeverage Chap 7 - PoliteknikShazwani AzmanBelum ada peringkat

- Analysis and Impact of LeverageDokumen88 halamanAnalysis and Impact of LeveragePuneet Sethi50% (2)

- C.A IPCC LeveragesDokumen3 halamanC.A IPCC LeveragesAkash GuptaBelum ada peringkat

- Analysis and Impact of Leverage: Operating Leverage Financial Leverage Combined LeverageDokumen98 halamanAnalysis and Impact of Leverage: Operating Leverage Financial Leverage Combined Leveragethella deva prasadBelum ada peringkat

- Chapter 1Dokumen26 halamanChapter 1Baby KhorBelum ada peringkat

- Chapter 4Dokumen42 halamanChapter 4Baby KhorBelum ada peringkat

- Chapter 5Dokumen7 halamanChapter 5Baby KhorBelum ada peringkat

- BWRR3123 AssignmentDokumen55 halamanBWRR3123 AssignmentBaby KhorBelum ada peringkat

- Case StudyDokumen32 halamanCase StudyBaby Khor100% (1)

- International Codes of Corporate GovernanceDokumen38 halamanInternational Codes of Corporate GovernanceBaby KhorBelum ada peringkat

- BWRR3103 Case GuideDokumen1 halamanBWRR3103 Case GuideBaby KhorBelum ada peringkat

- Trust 2Dokumen1 halamanTrust 2Baby KhorBelum ada peringkat

- Chapter 2 LatestDokumen24 halamanChapter 2 LatestBaby KhorBelum ada peringkat

- Bwrr3103 - Estate PlanningDokumen7 halamanBwrr3103 - Estate PlanningBaby KhorBelum ada peringkat

- Estate Planning 3 PDFDokumen2 halamanEstate Planning 3 PDFBaby KhorBelum ada peringkat

- Chap8 Cost of CapitalDokumen75 halamanChap8 Cost of CapitalBaby Khor50% (2)

- Chapter 1Dokumen33 halamanChapter 1Baby Khor100% (1)

- BWRR3103 EP SyllabusDokumen7 halamanBWRR3103 EP SyllabusBaby KhorBelum ada peringkat

- Topic 6-Cash Flow in Capital BudgetingDokumen61 halamanTopic 6-Cash Flow in Capital BudgetingBaby KhorBelum ada peringkat

- Chap10 Capital Budgeting TechniquesDokumen54 halamanChap10 Capital Budgeting TechniquesBaby KhorBelum ada peringkat

- Topic 9 Tax AdministrationDokumen31 halamanTopic 9 Tax AdministrationBaby KhorBelum ada peringkat

- Topic 3 - Stock ValuationDokumen50 halamanTopic 3 - Stock ValuationBaby KhorBelum ada peringkat

- Topic 1 - TVMDokumen61 halamanTopic 1 - TVMBaby KhorBelum ada peringkat

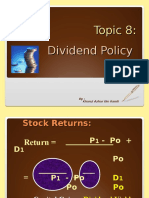

- Topic 8-Dividend PolicyDokumen46 halamanTopic 8-Dividend PolicyBaby KhorBelum ada peringkat

- Topic 7 - Financial Leverage - ExtraDokumen57 halamanTopic 7 - Financial Leverage - ExtraBaby KhorBelum ada peringkat

- Topic 5 Capital Budgeting TechniqueDokumen47 halamanTopic 5 Capital Budgeting TechniqueBaby KhorBelum ada peringkat

- Topic 7 - Financial Leverage - Part 2Dokumen35 halamanTopic 7 - Financial Leverage - Part 2Baby Khor100% (2)

- Chap13 Leverage and Capital StructureDokumen101 halamanChap13 Leverage and Capital StructureBaby KhorBelum ada peringkat

- Topic 4 Costofcapital NEW SLIDEDokumen60 halamanTopic 4 Costofcapital NEW SLIDEBaby KhorBelum ada peringkat

- Topic 4 AdditionalDokumen15 halamanTopic 4 AdditionalBaby KhorBelum ada peringkat

- Chap14 Dividend Payout PolicyDokumen62 halamanChap14 Dividend Payout PolicyBaby KhorBelum ada peringkat

- CHAPTER 1-Bank ManagementDokumen43 halamanCHAPTER 1-Bank ManagementBaby Khor90% (10)

- Topic 2 - Bond Valuation-A132Dokumen58 halamanTopic 2 - Bond Valuation-A132Baby KhorBelum ada peringkat

- CH.7 Plant Assets, Natural Resources, & IntangiblesDokumen98 halamanCH.7 Plant Assets, Natural Resources, & IntangiblesJuan Andres MarquezBelum ada peringkat

- (Studies in Finance and Accounting) Michael Firth (Auth.) - Management of Working Capital-Macmillan Education UK (1976)Dokumen156 halaman(Studies in Finance and Accounting) Michael Firth (Auth.) - Management of Working Capital-Macmillan Education UK (1976)Vignesh KathiresanBelum ada peringkat

- Simbol TradingDokumen25 halamanSimbol TradingEmman ElagoBelum ada peringkat

- Excel Professional Services, Inc.: Discussion QuestionsDokumen7 halamanExcel Professional Services, Inc.: Discussion QuestionskæsiiiBelum ada peringkat

- Capital Structure and Firm ValueDokumen22 halamanCapital Structure and Firm ValueGaurav gusaiBelum ada peringkat

- ELIZABETH TAILORING MATERIAL STORE (Horizontal&Vertical)Dokumen4 halamanELIZABETH TAILORING MATERIAL STORE (Horizontal&Vertical)Ann Ghie Solayao AlpasBelum ada peringkat

- Advanced Accounting ExamDokumen10 halamanAdvanced Accounting ExamMendoza Ron NixonBelum ada peringkat

- Marking Scheme Sample Question Paper Accountancy, Class XII Board Examination, March, 2015Dokumen13 halamanMarking Scheme Sample Question Paper Accountancy, Class XII Board Examination, March, 2015kamalBelum ada peringkat

- Laporan Keuangan Auditan 2020Dokumen219 halamanLaporan Keuangan Auditan 2020Muhammad Hasan SafariBelum ada peringkat

- Accounts Payable Process FlowchartDokumen4 halamanAccounts Payable Process FlowchartNarayan KulkarniBelum ada peringkat

- Acctg1205 - Chapter 8Dokumen48 halamanAcctg1205 - Chapter 8Elj Grace BaronBelum ada peringkat

- 40Chpt 12&13FINDokumen20 halaman40Chpt 12&13FINthe__wude8133Belum ada peringkat

- Chap 006Dokumen24 halamanChap 006Xeniya Morozova Kurmayeva100% (12)

- Financial Accounting and Reporting Learning ModulesDokumen126 halamanFinancial Accounting and Reporting Learning ModulesLovelyn Joy Solutan100% (2)

- Capital BudgetingDokumen108 halamanCapital Budgetingdhanraj_aartiBelum ada peringkat

- Julian EnterprisesDokumen62 halamanJulian EnterprisesMaryjane BatarinaBelum ada peringkat

- S2, 2018 Final Exam - Brief Suggested SolutionDokumen6 halamanS2, 2018 Final Exam - Brief Suggested SolutionShiv AchariBelum ada peringkat

- (FM02) - Chapter 7 The Valuation of Ordinary SharesDokumen12 halaman(FM02) - Chapter 7 The Valuation of Ordinary SharesKenneth John TomasBelum ada peringkat

- Notes ReceiDokumen2 halamanNotes ReceiDIANE EDRABelum ada peringkat

- Job Order Costing Exercises-Solved Problems-Home Work SolutionDokumen20 halamanJob Order Costing Exercises-Solved Problems-Home Work SolutionBasanta K Sahu100% (6)

- Lesson 2 - Advanced Financial Statement Analysis and ValuationDokumen66 halamanLesson 2 - Advanced Financial Statement Analysis and ValuationNoel Salazar JrBelum ada peringkat

- M4 Dividend Paying CapacityDokumen2 halamanM4 Dividend Paying CapacityReginald ValenciaBelum ada peringkat

- UplDokumen29 halamanUplvernaugBelum ada peringkat

- HB - Forex Midterm 2021Dokumen5 halamanHB - Forex Midterm 2021Allyssa Kassandra LucesBelum ada peringkat

- Accounting Q&ADokumen6 halamanAccounting Q&AIftikharBelum ada peringkat

- Inventory QuestionsDokumen2 halamanInventory QuestionsJoseph CameronBelum ada peringkat

- Management Accounting Notes1Dokumen170 halamanManagement Accounting Notes1Anish Gambhir100% (1)

- Group Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesDokumen28 halamanGroup Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesKeotshepile Esrom MputleBelum ada peringkat

- UTS AKL 2 - Resky Awaliah (A031181004)Dokumen3 halamanUTS AKL 2 - Resky Awaliah (A031181004)Resky AwaliahBelum ada peringkat

- Prop Class Method D. B Rate Year FactorDokumen9 halamanProp Class Method D. B Rate Year FactorracesapBelum ada peringkat