Anda mungkin juga menyukai

- Hard Money LendingDokumen16 halamanHard Money Lendingnikhilraheja100% (1)

- LCAR Unit 19 - Financing The Real Estate Transaction - 14th EditionDokumen66 halamanLCAR Unit 19 - Financing The Real Estate Transaction - 14th EditionTom BlefkoBelum ada peringkat

- The Advanced Guide To Equity Research Report WritingDokumen23 halamanThe Advanced Guide To Equity Research Report Writingsara_isarBelum ada peringkat

- Home Loans Project ReportDokumen105 halamanHome Loans Project Reportkaushal2442Belum ada peringkat

- PPT-Performance AppraisalDokumen56 halamanPPT-Performance Appraisalshiiba2287% (84)

- Pain Handout PDFDokumen7 halamanPain Handout PDFPatrick Snell100% (2)

- Let For Profit: A Guide for the Novice Buy to Let InvestorDari EverandLet For Profit: A Guide for the Novice Buy to Let InvestorBelum ada peringkat

- Chapter 15 Test Bank Partnerships - Formation, Operations, and Changes in Ownership InterestsDokumen22 halamanChapter 15 Test Bank Partnerships - Formation, Operations, and Changes in Ownership InterestsOBC LingayenBelum ada peringkat

- Pouring Concrete 1floorDokumen2 halamanPouring Concrete 1floorNimas AfinaBelum ada peringkat

- Mortgage Market (FINANCIAL MARKETS)Dokumen22 halamanMortgage Market (FINANCIAL MARKETS)Jasmin GubalaneBelum ada peringkat

- Sbi Reverse Mortgage LoanDokumen4 halamanSbi Reverse Mortgage LoanSukant Suku100% (1)

- Property Investment GuideDokumen16 halamanProperty Investment GuideakabasBelum ada peringkat

- Reverse Mortgage Project ReportDokumen54 halamanReverse Mortgage Project Reportkamdica86% (7)

- Islamic Housing FinanceDokumen26 halamanIslamic Housing FinanceAbdelnasir HaiderBelum ada peringkat

- IHF 18 19 Feb MUL 2013Dokumen44 halamanIHF 18 19 Feb MUL 2013Habib Sultan KhelBelum ada peringkat

- Diminishing MusharakahDokumen27 halamanDiminishing Musharakahsaif khanBelum ada peringkat

- Askari Islamic Bank PresentionDokumen39 halamanAskari Islamic Bank PresentionAatiqa100% (1)

- Chapter 7 Home OwnershipDokumen33 halamanChapter 7 Home OwnershipandymengBelum ada peringkat

- Rehmanwaheed 3180 17836 2 12. Diminishing MusharakahDokumen19 halamanRehmanwaheed 3180 17836 2 12. Diminishing MusharakahSadia AbidBelum ada peringkat

- #10 Lease Accounting Changes and The Bottom Line: What Corporate Real Estate Needs To KnowDokumen26 halaman#10 Lease Accounting Changes and The Bottom Line: What Corporate Real Estate Needs To Knowapi-26443227Belum ada peringkat

- Flame II - Jaideep 12th March 2022Dokumen25 halamanFlame II - Jaideep 12th March 2022Shreya TalujaBelum ada peringkat

- Loans Versus Leases: Business Aspects Loan Finance Lease Operating LeaseDokumen2 halamanLoans Versus Leases: Business Aspects Loan Finance Lease Operating LeaseRajesh KumarBelum ada peringkat

- MFRS123Dokumen23 halamanMFRS123Kelvin Leong100% (1)

- BAF Group-6Dokumen21 halamanBAF Group-6Amit Halder 2020-22Belum ada peringkat

- Residential Lending Guide: Natwest Intermediary SolutionsDokumen16 halamanResidential Lending Guide: Natwest Intermediary SolutionsSofia marisa fernandesBelum ada peringkat

- Pag Ibig Info - CIMBDokumen19 halamanPag Ibig Info - CIMBReynaldo PogzBelum ada peringkat

- ACTL5303Week6 2019 Property PE HedgeFundsDokumen46 halamanACTL5303Week6 2019 Property PE HedgeFundsZara KhanBelum ada peringkat

- Topic 4 BONDDokumen39 halamanTopic 4 BONDnurul shafifah bt ismailBelum ada peringkat

- Topic 4 BOND Merged CompressedDokumen109 halamanTopic 4 BOND Merged Compressednurul shafifah bt ismailBelum ada peringkat

- Chapter 7 Short Term FinancingDokumen41 halamanChapter 7 Short Term Financingzatty kimBelum ada peringkat

- Housing Finance Methods in IndiaDokumen23 halamanHousing Finance Methods in Indiaadhar_kashyapBelum ada peringkat

- Lecture 6Dokumen33 halamanLecture 6Karissa TanBelum ada peringkat

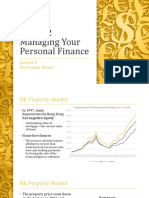

- GE1202 Managing Your Personal Finance: Purchasing HomesDokumen33 halamanGE1202 Managing Your Personal Finance: Purchasing HomesAiden LANBelum ada peringkat

- Borowing CostDokumen15 halamanBorowing CostmheronmBelum ada peringkat

- Fixed Income Portfolio Management: Mortgage-Backed SecuritiesDokumen65 halamanFixed Income Portfolio Management: Mortgage-Backed SecuritiesJingyi GuoBelum ada peringkat

- Principle of LendingDokumen29 halamanPrinciple of Lendingsonal yadavBelum ada peringkat

- IFC Advisory - HOUSING MICROFINANCE TOOLKITDokumen23 halamanIFC Advisory - HOUSING MICROFINANCE TOOLKITraj.raanaaBelum ada peringkat

- Credit DerivativesDokumen10 halamanCredit Derivativesmiku hrshBelum ada peringkat

- Strategic FinanceDokumen15 halamanStrategic FinanceSawaira QureshiBelum ada peringkat

- PFP-Workshop & Tutorial 7-April 2023-Suggested SolutionsDokumen17 halamanPFP-Workshop & Tutorial 7-April 2023-Suggested SolutionsChristine VunBelum ada peringkat

- Bridging Paper v16Dokumen39 halamanBridging Paper v16Jasmeet BhatiaBelum ada peringkat

- Project Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulDokumen99 halamanProject Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulSudhir WaghuleBelum ada peringkat

- Capital and Use of Credit - 2022Dokumen69 halamanCapital and Use of Credit - 2022Lucky GojeBelum ada peringkat

- Diminishing Musharakah ConceptDokumen26 halamanDiminishing Musharakah ConceptHasan Irfan SiddiquiBelum ada peringkat

- FRR-ALM Ch1Dokumen69 halamanFRR-ALM Ch1Marek KurzyńskiBelum ada peringkat

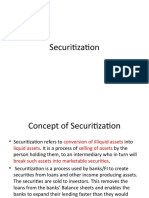

- SecuritizationDokumen23 halamanSecuritizationHarshit NagpalBelum ada peringkat

- Topic 8:: Principles of Lending & Credit FacilitiesDokumen35 halamanTopic 8:: Principles of Lending & Credit FacilitiesPremah BalasundramBelum ada peringkat

- Chapter 13: Commercial Bank Operations 3edDokumen26 halamanChapter 13: Commercial Bank Operations 3edMarwa HassanBelum ada peringkat

- FIN 102 Banking and Financial InstitutionsDokumen10 halamanFIN 102 Banking and Financial Institutionsron aviBelum ada peringkat

- Topic 5 Valuation of Bonds and Shares PDFDokumen32 halamanTopic 5 Valuation of Bonds and Shares PDFMoud KhalfaniBelum ada peringkat

- MFRS123 Borrowing CostDokumen15 halamanMFRS123 Borrowing CostintanBelum ada peringkat

- Fixed-Rate Mortgage, Monthly PaymentsDokumen41 halamanFixed-Rate Mortgage, Monthly Paymentslinda zyongweBelum ada peringkat

- RTO Programme Pitchbook 20191213Dokumen7 halamanRTO Programme Pitchbook 20191213Kung FooBelum ada peringkat

- Corporate Banking: Funded Services Lending /advances CB-CHPP07Dokumen40 halamanCorporate Banking: Funded Services Lending /advances CB-CHPP07Prakash SharmaBelum ada peringkat

- Securitization of Mortgages Voctober2019Dokumen64 halamanSecuritization of Mortgages Voctober2019Hins LeeBelum ada peringkat

- Bond ValuationDokumen36 halamanBond ValuationBhavesh RoheraBelum ada peringkat

- EC06Dokumen21 halamanEC06engrsaab51Belum ada peringkat

- Module 3 Real Estate Worksheet 5Yj89ZvoPADokumen12 halamanModule 3 Real Estate Worksheet 5Yj89ZvoPANAMAN JAINBelum ada peringkat

- 2 May 2023 INDIVIDUAL Investor PresentationDokumen22 halaman2 May 2023 INDIVIDUAL Investor PresentationAdetokunbo AdemolaBelum ada peringkat

- PDS Affin Home Fin I ENG 1Dokumen8 halamanPDS Affin Home Fin I ENG 1Iman KamalBelum ada peringkat

- Project Finance - Individual AssignmentDokumen2 halamanProject Finance - Individual AssignmentjitrapaBelum ada peringkat

- Credit Risk Analysis and InterpretationDokumen46 halamanCredit Risk Analysis and InterpretationComennius YayoBelum ada peringkat

- Individual Car Loan Agreement SampleDokumen32 halamanIndividual Car Loan Agreement Sampleey019.aaBelum ada peringkat

- Economic Evaluation AnalysisDokumen15 halamanEconomic Evaluation AnalysisNAYOMI LOIS CISNEROSBelum ada peringkat

- 3051 Revised DateDokumen1 halaman3051 Revised DateElla and MiraBelum ada peringkat

- Accounting 9 DCF ModelDokumen1 halamanAccounting 9 DCF ModelRica CatanguiBelum ada peringkat

- Ind Nifty BankDokumen2 halamanInd Nifty BankVishal GandhleBelum ada peringkat

- A Leadership Case Study - How HR Caused Toyota CrashDokumen6 halamanA Leadership Case Study - How HR Caused Toyota CrashLminith100% (1)

- Urban Development Policies in Developing Countries: Bertrand RenaudDokumen13 halamanUrban Development Policies in Developing Countries: Bertrand RenaudShahin Kauser ZiaudeenBelum ada peringkat

- Math IA 1Dokumen8 halamanMath IA 1Rabi SalujaBelum ada peringkat

- Financial DerivativesDokumen2 halamanFinancial Derivativesviveksharma51Belum ada peringkat

- Analisis Perbandingan Model Springate, Zmijewski, Dan Altman Dalam Memprediksi Yang Terdaftar Di Bursa Efek IndonesiaDokumen13 halamanAnalisis Perbandingan Model Springate, Zmijewski, Dan Altman Dalam Memprediksi Yang Terdaftar Di Bursa Efek IndonesiahanifBelum ada peringkat

- Supplier Acccreditation FormDokumen4 halamanSupplier Acccreditation FormLizanne GauranaBelum ada peringkat

- Workforce Utilization and Employment Practices Part - 2Dokumen13 halamanWorkforce Utilization and Employment Practices Part - 2HOD CommerceBelum ada peringkat

- 4 Commissioner - of - Internal - Revenue - v. - Court - ofDokumen8 halaman4 Commissioner - of - Internal - Revenue - v. - Court - ofClaire SantosBelum ada peringkat

- Market Plan of Lucky Cement FActoryDokumen20 halamanMarket Plan of Lucky Cement FActoryRehman RehoBelum ada peringkat

- JPMorgan Chase London Whale HDokumen12 halamanJPMorgan Chase London Whale HMaksym ShodaBelum ada peringkat

- Deficiency in Services Final DraftDokumen32 halamanDeficiency in Services Final DraftNaveen PandeyBelum ada peringkat

- Chapter 3 - Influential Digital Subcultures - USUDokumen14 halamanChapter 3 - Influential Digital Subcultures - USUbambang suwarnoBelum ada peringkat

- Long Quiz BSA 1st Yr 2023 2024Dokumen10 halamanLong Quiz BSA 1st Yr 2023 2024Kenneth Del RosarioBelum ada peringkat

- The Scope and Challenge of International MarketingDokumen24 halamanThe Scope and Challenge of International MarketingBetty NiamienBelum ada peringkat

- How To Add Money To Your Investment A/cDokumen2 halamanHow To Add Money To Your Investment A/cNarendra VinchurkarBelum ada peringkat

- Building and Construction General On Site Award Ma000020 Pay GuideDokumen130 halamanBuilding and Construction General On Site Award Ma000020 Pay Guidesudip sharmaBelum ada peringkat

- Crossing of ChequesDokumen22 halamanCrossing of ChequesNayan BhalotiaBelum ada peringkat

- AER Presentation On RAB MultiplesDokumen18 halamanAER Presentation On RAB MultiplesKGBelum ada peringkat

- WEF A Partner in Shaping HistoryDokumen190 halamanWEF A Partner in Shaping HistoryAbi SolaresBelum ada peringkat

- Quiz Chapter 1 - AnswersDokumen21 halamanQuiz Chapter 1 - Answersbobbybobsmith12345Belum ada peringkat

- Employment Law Outline PDFDokumen12 halamanEmployment Law Outline PDFkatelyn.elliot01Belum ada peringkat