Anda mungkin juga menyukai

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokumen91 halamanPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBertoniBelum ada peringkat

- Pope Phft2015 Corp PP Stu 03Dokumen81 halamanPope Phft2015 Corp PP Stu 03yennhi22690Belum ada peringkat

- Issues in AccountingDokumen51 halamanIssues in AccountingKashif RaheemBelum ada peringkat

- Operating Decisions and The Income StatementDokumen39 halamanOperating Decisions and The Income StatementNahla Ali HassanBelum ada peringkat

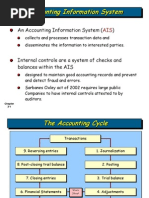

- The Accounting Information SystemDokumen12 halamanThe Accounting Information SystemIntelaCrosoftBelum ada peringkat

- 150 Harrison FAIFRS11e Inppt 03Dokumen55 halaman150 Harrison FAIFRS11e Inppt 03irma makharoblidzeBelum ada peringkat

- Acctg11e SM CH11Dokumen52 halamanAcctg11e SM CH11titirBelum ada peringkat

- Lecture 3 PDFDokumen64 halamanLecture 3 PDFRachel TamBelum ada peringkat

- Accounting Cycle (I) - : Recording Economic TransactionsDokumen49 halamanAccounting Cycle (I) - : Recording Economic TransactionsDevang BharaniaBelum ada peringkat

- CH 03Dokumen68 halamanCH 03Chang Chan Chong100% (1)

- Chapter 3 Adjusting The AccountsDokumen28 halamanChapter 3 Adjusting The AccountsfuriousTaherBelum ada peringkat

- Chapter 2Dokumen86 halamanChapter 2Allison StewartBelum ada peringkat

- Ethics and Standards Violations in Financial Advising SituationsDokumen7 halamanEthics and Standards Violations in Financial Advising SituationsPoojan ShahBelum ada peringkat

- Lecture 3 PDFDokumen47 halamanLecture 3 PDFdabudhabicozBelum ada peringkat

- CH3 Titman 12eDokumen84 halamanCH3 Titman 12elouise carinoBelum ada peringkat

- CH 03Dokumen57 halamanCH 03Sidra IqbalBelum ada peringkat

- ProblemC ch05Dokumen5 halamanProblemC ch05Adan FakihBelum ada peringkat

- ACC 305 Complete Course FilesDokumen16 halamanACC 305 Complete Course FileshomeworkbagsBelum ada peringkat

- ch11 SolutionsDokumen36 halamanch11 Solutionsaboodyuae2000Belum ada peringkat

- Australian Tax ObligationsDokumen17 halamanAustralian Tax Obligationshemant100% (2)

- Chapter 4Dokumen48 halamanChapter 4FadhilahAbdullahBelum ada peringkat

- 5.2. Specific ArrangementsDokumen51 halaman5.2. Specific ArrangementsPranjal pandeyBelum ada peringkat

- Harrison Fa11 STPPT 02Dokumen119 halamanHarrison Fa11 STPPT 02gizem akçaBelum ada peringkat

- Fin02 - Financial Statement and ReportsDokumen41 halamanFin02 - Financial Statement and ReportsGenieffer Kate Gulfo100% (1)

- Financial Accounting 4th Edition Spiceland Solutions Manual 1Dokumen132 halamanFinancial Accounting 4th Edition Spiceland Solutions Manual 1richard100% (32)

- Financial Accounting 4Th Edition Spiceland Solutions Manual Full Chapter PDFDokumen36 halamanFinancial Accounting 4Th Edition Spiceland Solutions Manual Full Chapter PDFphyllis.horan125100% (10)

- Recognition and MeasurementDokumen16 halamanRecognition and MeasurementajishBelum ada peringkat

- Chapter 2 PPT (To Students)Dokumen64 halamanChapter 2 PPT (To Students)歩美桜井Belum ada peringkat

- TBDokumen31 halamanTBBenj LadesmaBelum ada peringkat

- C4 Accrual Accounting ConceptDokumen72 halamanC4 Accrual Accounting ConceptAllen Allen100% (2)

- CAT - T3 FREE Online CBE Based Mock ExamDokumen6 halamanCAT - T3 FREE Online CBE Based Mock ExamACCALIVEBelum ada peringkat

- MBA SOP 2021 - Sessions 2 & 3Dokumen86 halamanMBA SOP 2021 - Sessions 2 & 3Bakht Yawer KirmaniBelum ada peringkat

- Lesson 2 Adjusting The Accounts Service TypeDokumen33 halamanLesson 2 Adjusting The Accounts Service TypeSofia Naraine OnilongoBelum ada peringkat

- SPPTChap 003Dokumen20 halamanSPPTChap 003Farhan Osman ahmedBelum ada peringkat

- Financial Accounting: Recording Business TransactionsDokumen64 halamanFinancial Accounting: Recording Business Transactionsirma makharoblidzeBelum ada peringkat

- Unit Two Accounting CycleDokumen59 halamanUnit Two Accounting CycleElias ZeynuBelum ada peringkat

- Financial Accounting, 3e: Weygandt, Kieso, & KimmelDokumen42 halamanFinancial Accounting, 3e: Weygandt, Kieso, & KimmelLili Al ShamisiBelum ada peringkat

- The Balance of Payments - 3_FinanceDokumen57 halamanThe Balance of Payments - 3_Financekfaslus1206Belum ada peringkat

- Accrual Basis vs Cash Basis AccountingDokumen58 halamanAccrual Basis vs Cash Basis AccountingSaadet Şahinyılmaz ÇehreliBelum ada peringkat

- Session 3+4 - Adjusting the AccountsDokumen40 halamanSession 3+4 - Adjusting the Accountshieucaiminh155Belum ada peringkat

- Slides CH 05 UpdatedDokumen44 halamanSlides CH 05 Updatedakshitnagpal9119Belum ada peringkat

- ch03 AdjustmentsDokumen69 halamanch03 Adjustmentsvioletlupin1204Belum ada peringkat

- Government GrantsDokumen9 halamanGovernment Grantssorin8488100% (1)

- Chapter 1 AccountingDokumen9 halamanChapter 1 Accountingmoon loverBelum ada peringkat

- Revenue Recognition 14th EditionDokumen77 halamanRevenue Recognition 14th Editiontafti_847122680100% (1)

- BSBFIM501Dokumen16 halamanBSBFIM501Paweena SaethaoBelum ada peringkat

- Ccounting Principles,: Weygandt, Kieso, & KimmelDokumen58 halamanCcounting Principles,: Weygandt, Kieso, & Kimmelpiash246100% (2)

- ACCT 504 Midterm Exam 2Dokumen7 halamanACCT 504 Midterm Exam 2DeVryHelpBelum ada peringkat

- Adjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinDokumen58 halamanAdjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonBelum ada peringkat

- CH 01Dokumen2 halamanCH 01Sandeep Kumar PalBelum ada peringkat

- f3 Ffa Examreport j15Dokumen4 halamanf3 Ffa Examreport j157777gracieBelum ada peringkat

- Wiley - Chapter 3: The Accounting Information SystemDokumen36 halamanWiley - Chapter 3: The Accounting Information SystemIvan BliminseBelum ada peringkat

- CH 03Dokumen58 halamanCH 03indahmuliasariBelum ada peringkat

- Day 4 Income Statement and Statement of Cash FlowDokumen31 halamanDay 4 Income Statement and Statement of Cash FlowSue-Allen Mardenborough100% (1)

- Basic Financial StatementsDokumen45 halamanBasic Financial StatementsparhBelum ada peringkat

- Module 10 QuestionsDokumen3 halamanModule 10 QuestionsRishi BhagatBelum ada peringkat

- IntAcc3 Final Departmental Examination 2nd Sem AY 2020 2021Dokumen39 halamanIntAcc3 Final Departmental Examination 2nd Sem AY 2020 2021Mika MolinaBelum ada peringkat

- Acct 504 Week 8 Final Exam All 4 Sets - DevryDokumen17 halamanAcct 504 Week 8 Final Exam All 4 Sets - Devrycoursehomework0% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionDari EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionBelum ada peringkat

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyDari EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyBelum ada peringkat

- Chapter 2 and Chapter 3 PowerPoint SlidesDokumen13 halamanChapter 2 and Chapter 3 PowerPoint SlidesnoblevermaBelum ada peringkat

- Pecha Kucha AmazonDokumen20 halamanPecha Kucha AmazonnoblevermaBelum ada peringkat

- Erp PresentationDokumen43 halamanErp PresentationKiran PuttaBelum ada peringkat

- Braun Ma4 SM 10Dokumen72 halamanBraun Ma4 SM 10noblevermaBelum ada peringkat

- E-27A Bond Amortization TableDokumen3 halamanE-27A Bond Amortization TablenoblevermaBelum ada peringkat

- Harley Davidson Case Study - Noble VermaDokumen4 halamanHarley Davidson Case Study - Noble Vermanobleverma100% (1)

- Braun Ma4 SM 09Dokumen55 halamanBraun Ma4 SM 09nobleverma100% (1)

- BernoulliDokumen39 halamanBernoullinoblevermaBelum ada peringkat

- Accrual Accounting and Income NotesDokumen13 halamanAccrual Accounting and Income NotesnoblevermaBelum ada peringkat

- TPMDokumen54 halamanTPMnoblevermaBelum ada peringkat

- Paper 2newDokumen328 halamanPaper 2newAnonymous 1ClGHbiT0JBelum ada peringkat

- Intermediate Accounting Vol 1 Canadian 2nd Edition Lo Test Bank 1Dokumen91 halamanIntermediate Accounting Vol 1 Canadian 2nd Edition Lo Test Bank 1anthony100% (44)

- FINAL Conceptual Framework and Accounting Standards PDFDokumen24 halamanFINAL Conceptual Framework and Accounting Standards PDFJotaro KujoBelum ada peringkat

- Tax Accounting ConceptsDokumen17 halamanTax Accounting ConceptsKathleenAlfaroDelosoBelum ada peringkat

- Financial Accounting ExamDokumen12 halamanFinancial Accounting Examjano_art21Belum ada peringkat

- 8963 25Dokumen42 halaman8963 25OSDocs2012Belum ada peringkat

- Bsbfim601 Manage FinancesDokumen27 halamanBsbfim601 Manage Financesmuhammad saqib jabbarBelum ada peringkat

- Computarised System ProjectDokumen30 halamanComputarised System ProjectChintamaniChoiceBelum ada peringkat

- Income Tax NotesDokumen265 halamanIncome Tax NotesSabin YadavBelum ada peringkat

- Notes in TaxationDokumen13 halamanNotes in Taxationjamaica_maglinteBelum ada peringkat

- Revenue Memorandum Circular No. 39-2007Dokumen6 halamanRevenue Memorandum Circular No. 39-2007Charmaine GraceBelum ada peringkat

- Income Tax Rates & ClassificationsDokumen216 halamanIncome Tax Rates & ClassificationsalicorpanaoBelum ada peringkat

- Cash and Accrual Basis & Single Entry - OUTLINEDokumen3 halamanCash and Accrual Basis & Single Entry - OUTLINESophia Marie VerdeflorBelum ada peringkat

- Cash Basis vs Accrual Basis AccountingDokumen3 halamanCash Basis vs Accrual Basis Accountingayushiridara kwonBelum ada peringkat

- CB Review Modules 3 and 4Dokumen175 halamanCB Review Modules 3 and 4Glemhar RodriguezBelum ada peringkat

- Handout No. 3 Accrev San BedaDokumen10 halamanHandout No. 3 Accrev San BedaJustine CruzBelum ada peringkat

- Tax II Case Digest on CFI Jurisdiction over Injunction PetitionDokumen23 halamanTax II Case Digest on CFI Jurisdiction over Injunction PetitionfaithimeeBelum ada peringkat

- Taxation of Individuals and Business Entities 2017 8th Edition Spilker Solutions ManualDokumen10 halamanTaxation of Individuals and Business Entities 2017 8th Edition Spilker Solutions Manualloanmaiyu28p7100% (22)

- SMChap 008Dokumen55 halamanSMChap 008Ine100% (2)

- Residential Rental Property GuideDokumen31 halamanResidential Rental Property GuideArnold GalvanBelum ada peringkat

- Chapter 3: Introduction To Income Taxation: Item of Gross Income Taxable IncomeDokumen39 halamanChapter 3: Introduction To Income Taxation: Item of Gross Income Taxable IncomeSheva Mae Suello0% (1)

- ErrorDokumen6 halamanErroranggandakonoh0% (1)

- Cash and AccrualDokumen3 halamanCash and AccrualHarvey Dienne Quiambao100% (2)

- UNHCR's Guide to IPSAS ImplementationDokumen43 halamanUNHCR's Guide to IPSAS ImplementationrafimaneBelum ada peringkat

- CIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Dokumen5 halamanCIR v. Isabela Cultural Corp GR No. 17223, 12 Feb 2007Marge OstanBelum ada peringkat

- Income Tax Schemes, Accounting Periods, Accounting Methods, and ReportingDokumen6 halamanIncome Tax Schemes, Accounting Periods, Accounting Methods, and ReportingAilene MendozaBelum ada peringkat

- Accounting ManualDokumen273 halamanAccounting Manualkailasasundaram100% (3)

- Fin 623 Quiz # 04 Mega File Solved by AfaaqDokumen35 halamanFin 623 Quiz # 04 Mega File Solved by AfaaqShahaan Zulfiqar100% (2)

- CIR Vs Lancaster CIRDokumen18 halamanCIR Vs Lancaster CIRAerith AlejandreBelum ada peringkat

- Taxation Situational ProblemsDokumen32 halamanTaxation Situational ProblemsMilo MilkBelum ada peringkat