Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Banking 101 - Large Cap Bank Primer - Deutsche Bank (2011) PDFDokumen112 halamanBanking 101 - Large Cap Bank Primer - Deutsche Bank (2011) PDFJcove100% (2)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- MKT 320F Exam 2 Review Lecture NotesDokumen33 halamanMKT 320F Exam 2 Review Lecture NotesJordan DurraniBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- E-Commerce at Williams Sonoma NewDokumen20 halamanE-Commerce at Williams Sonoma NewMuhammad Amjad AkmalBelum ada peringkat

- Marketing Management Case 2 DHL Worldwide Express: Master of Management Universitas Gadjah Mada 2009Dokumen9 halamanMarketing Management Case 2 DHL Worldwide Express: Master of Management Universitas Gadjah Mada 2009noradwiyah86Belum ada peringkat

- TB 04Dokumen39 halamanTB 04Nashwa Saad100% (1)

- 2016 04 1420161336unit3Dokumen8 halaman2016 04 1420161336unit3Matías E. PhilippBelum ada peringkat

- BP MidtermDokumen4 halamanBP MidtermGelyn CruzBelum ada peringkat

- Chapter 12Dokumen27 halamanChapter 12Gelyn CruzBelum ada peringkat

- A. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsDokumen1 halamanA. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsGelyn CruzBelum ada peringkat

- Ais 1Dokumen48 halamanAis 1Gelyn CruzBelum ada peringkat

- Chapter 8Dokumen6 halamanChapter 8Gelyn CruzBelum ada peringkat

- CRC-ACE PW-TaxDokumen14 halamanCRC-ACE PW-TaxGelyn CruzBelum ada peringkat

- Decision MakingDokumen28 halamanDecision MakingGelyn CruzBelum ada peringkat

- Research Questionnaire: TH TH THDokumen4 halamanResearch Questionnaire: TH TH THGelyn CruzBelum ada peringkat

- Accounting Information SystemDokumen48 halamanAccounting Information SystemGelyn CruzBelum ada peringkat

- Chapter 24Dokumen20 halamanChapter 24Gelyn CruzBelum ada peringkat

- Phase I-Risk Assessment Planning The AudDokumen21 halamanPhase I-Risk Assessment Planning The AudGelyn CruzBelum ada peringkat

- Bsa 1Dokumen110 halamanBsa 1Gelyn CruzBelum ada peringkat

- Reaction PaperDokumen3 halamanReaction PaperGelyn CruzBelum ada peringkat

- Responsibility Acctg, Transfer Pricing & GP AnalysisDokumen21 halamanResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzBelum ada peringkat

- Test Bank Chapter 1 Managerial AccountingDokumen9 halamanTest Bank Chapter 1 Managerial AccountingGelyn CruzBelum ada peringkat

- MS - EconomicsDokumen16 halamanMS - EconomicsGelyn CruzBelum ada peringkat

- Auditing Theory TEST BANKDokumen23 halamanAuditing Theory TEST BANKGelyn CruzBelum ada peringkat

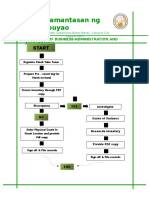

- Pamantasan NG Cabuyao: College of Business Administration and AccountancyDokumen1 halamanPamantasan NG Cabuyao: College of Business Administration and AccountancyGelyn CruzBelum ada peringkat

- John Gokongwei1Dokumen4 halamanJohn Gokongwei1Gelyn CruzBelum ada peringkat

- 1iab SampleDokumen52 halaman1iab SampleGelyn CruzBelum ada peringkat

- Chapter 11 Cash Flow Estimation and Risk Analysis PDFDokumen80 halamanChapter 11 Cash Flow Estimation and Risk Analysis PDFGelyn Cruz100% (1)

- Thesis It To Be FinalizeDokumen29 halamanThesis It To Be FinalizeGelyn CruzBelum ada peringkat

- Thesis Pattern ItDokumen1 halamanThesis Pattern ItGelyn CruzBelum ada peringkat

- 5 ForcesDokumen4 halaman5 ForcesSue S100% (1)

- Lecture 4dssfdDokumen12 halamanLecture 4dssfdChristelle Marie Aquino Beroña0% (2)

- Group Assignment AccountingDokumen3 halamanGroup Assignment Accountingkow kai lynnBelum ada peringkat

- Marketing PlanDokumen21 halamanMarketing PlanUyen VuBelum ada peringkat

- 1Bdc Cpa Review Institute: Cost AccountingDokumen8 halaman1Bdc Cpa Review Institute: Cost AccountingJason BautistaBelum ada peringkat

- ASSIGNMENT 407 - Audit of InvestmentsDokumen3 halamanASSIGNMENT 407 - Audit of InvestmentsWam OwnBelum ada peringkat

- Working Capital Management - by Krishnamachari SrinivasanDokumen71 halamanWorking Capital Management - by Krishnamachari SrinivasanKrishnamachari Srinivasan100% (3)

- Additional Paid in CapitalDokumen2 halamanAdditional Paid in Capitalrt2222Belum ada peringkat

- Asian PaintDokumen12 halamanAsian PaintAnkit DubeyBelum ada peringkat

- Production Processes: Learning ObjectivesDokumen7 halamanProduction Processes: Learning ObjectivesAriani AmaliaBelum ada peringkat

- Marketing StrategyDokumen7 halamanMarketing StrategyAngira dasBelum ada peringkat

- GIANAN Thesis Final Gab and Shanley JANUARY 7 2024 1Dokumen41 halamanGIANAN Thesis Final Gab and Shanley JANUARY 7 2024 1Marco Antonio IIBelum ada peringkat

- ACMM Group Assignment Ceat TyresDokumen27 halamanACMM Group Assignment Ceat TyresGaurang SaxenaBelum ada peringkat

- Checklist For Applications For Registration Under BOOK 1 of E.O. 226Dokumen3 halamanChecklist For Applications For Registration Under BOOK 1 of E.O. 226Grace RenonBelum ada peringkat

- Reliance Capital: Reliance Home Finance: A Deep Dive Into Business ModelDokumen15 halamanReliance Capital: Reliance Home Finance: A Deep Dive Into Business Modelsharkl123Belum ada peringkat

- The Process of FinancingDokumen3 halamanThe Process of FinancingAjit Kumar RoyBelum ada peringkat

- Fundamentals of Cost Accounting 5th Edition Lanen Solutions ManualDokumen35 halamanFundamentals of Cost Accounting 5th Edition Lanen Solutions Manualphelandieuz7n100% (29)

- Market Segmentation of Bata Shoe Company LTD PDFDokumen1 halamanMarket Segmentation of Bata Shoe Company LTD PDFkhanzakirahmad10Belum ada peringkat

- PPTDokumen2 halamanPPTKhushi GuptaBelum ada peringkat

- Wilkerson - Case Study1 PDFDokumen2 halamanWilkerson - Case Study1 PDFPavanBelum ada peringkat

- CAMELS Project of Axis BankDokumen47 halamanCAMELS Project of Axis Bankjatinmakwana90Belum ada peringkat

- Today: - Marketing Orientated Business - Competitive Advantage - Tayto Crisps Case-StudyDokumen6 halamanToday: - Marketing Orientated Business - Competitive Advantage - Tayto Crisps Case-StudyIja Ribakova OguamaBelum ada peringkat

- Capital BudgetingDokumen4 halamanCapital BudgetingSatish Kumar SonwaniBelum ada peringkat

- COGS1 ExampleDokumen30 halamanCOGS1 ExamplePritesh MoganeBelum ada peringkat