Anda mungkin juga menyukai

- Job Compatibility QuestionnaireDokumen4 halamanJob Compatibility QuestionnaireHardik Sharma0% (1)

- Engineering Graphics - I 2003Dokumen4 halamanEngineering Graphics - I 2003Hardik SharmaBelum ada peringkat

- Engineering Graphics 2002Dokumen2 halamanEngineering Graphics 2002Hardik SharmaBelum ada peringkat

- Engineering Graphics 2004Dokumen3 halamanEngineering Graphics 2004Hardik SharmaBelum ada peringkat

- Engineering Graphics 2002 PDFDokumen2 halamanEngineering Graphics 2002 PDFHardik SharmaBelum ada peringkat

- Term Loan ProcedureDokumen5 halamanTerm Loan ProcedureHardik Sharma100% (1)

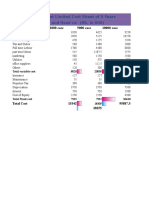

- Ashank Winer Privet Limited Cost Sheet of 5 Years Total Variable Cost and Fixed Cos (RS. in 000)Dokumen4 halamanAshank Winer Privet Limited Cost Sheet of 5 Years Total Variable Cost and Fixed Cos (RS. in 000)Hardik SharmaBelum ada peringkat

- Prototypin G: Gattani Neha Brijmohan ROLL NO.14081 MBA-1Dokumen11 halamanPrototypin G: Gattani Neha Brijmohan ROLL NO.14081 MBA-1Hardik SharmaBelum ada peringkat

- Financial ManagementDokumen48 halamanFinancial ManagementHardik SharmaBelum ada peringkat

- French BenifitsDokumen63 halamanFrench BenifitsHardik SharmaBelum ada peringkat

- Law 1Dokumen73 halamanLaw 1Hardik SharmaBelum ada peringkat

- Mechanics of A-B-C AnalysisDokumen4 halamanMechanics of A-B-C AnalysisHardik SharmaBelum ada peringkat

- Inventory Software: Application Software On Inventory of Textile Trading CompanyDokumen9 halamanInventory Software: Application Software On Inventory of Textile Trading CompanyHardik SharmaBelum ada peringkat

- RegressionDokumen87 halamanRegressionHardik Sharma100% (1)

- 16793theory of CostDokumen54 halaman16793theory of CostHardik SharmaBelum ada peringkat

- 104-Me 1443017742071Dokumen82 halaman104-Me 1443017742071Hardik SharmaBelum ada peringkat

- Data vs. InformationDokumen72 halamanData vs. InformationHardik SharmaBelum ada peringkat

- B-Sale of GoodsDokumen21 halamanB-Sale of GoodsHardik SharmaBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Gas Station Plaridel BypassDokumen19 halamanGas Station Plaridel BypassEladio AbquinaBelum ada peringkat

- Build A Brilliant Bookkeeping Business - WarbellaDokumen47 halamanBuild A Brilliant Bookkeeping Business - WarbellaMeiliana Anggelia100% (1)

- Direct and Indirect Tax CourseDokumen10 halamanDirect and Indirect Tax CourseKASHISH GUPTABelum ada peringkat

- Human Resource Management Journal Volume 28 Issue 1 2018 (Doi 10.1111 - 1748-8583.12185) - Issue Information PDFDokumen4 halamanHuman Resource Management Journal Volume 28 Issue 1 2018 (Doi 10.1111 - 1748-8583.12185) - Issue Information PDFHediar Handito SyahputraBelum ada peringkat

- Headline Verdana Bold: Operationalizing Transfer Pricing From Theory To PracticeDokumen55 halamanHeadline Verdana Bold: Operationalizing Transfer Pricing From Theory To PracticeArif Khan NabilBelum ada peringkat

- Substantial EvidenceDokumen15 halamanSubstantial EvidenceArahbells100% (1)

- BIR Sample Receipts and Invoices - V9 - OpsMemoDokumen7 halamanBIR Sample Receipts and Invoices - V9 - OpsMemoYunit M Stariray100% (1)

- Xxont So Ack PrintDokumen3 halamanXxont So Ack Printanon_357846910Belum ada peringkat

- ABSS Qualification Test: SINGLE CURRENCY (ABSS Accounting v25)Dokumen8 halamanABSS Qualification Test: SINGLE CURRENCY (ABSS Accounting v25)Ricky WahyudiBelum ada peringkat

- Print 8Dokumen1 halamanPrint 8babar aliBelum ada peringkat

- RENATO V. DIAZ and AURORA MA. F. TIMBOL Vs THE SECRETARY OF FINANCE G.R. No. 193007 July 19, 2011Dokumen10 halamanRENATO V. DIAZ and AURORA MA. F. TIMBOL Vs THE SECRETARY OF FINANCE G.R. No. 193007 July 19, 2011sherwin pulidoBelum ada peringkat

- Profit & Loss Statement: PT AlkindiDokumen4 halamanProfit & Loss Statement: PT AlkindiKiky SrBelum ada peringkat

- (Tax) CPAR Preweek2Dokumen7 halaman(Tax) CPAR Preweek2Nor-janisah PundaodayaBelum ada peringkat

- Salon and Wellness Business PlanDokumen43 halamanSalon and Wellness Business PlanShanu MehtaBelum ada peringkat

- GST Scanner of CA Final May 2019 by DG Sir PDFDokumen17 halamanGST Scanner of CA Final May 2019 by DG Sir PDFSurekha BonagiriBelum ada peringkat

- HBC 2211 TaxationDokumen105 halamanHBC 2211 TaxationMAYENDE ALBERTBelum ada peringkat

- GFC - Payment - Schedule - Phase 2-MergedDokumen4 halamanGFC - Payment - Schedule - Phase 2-MergedVasundhara GuptaBelum ada peringkat

- Sale Tax ReportDokumen10 halamanSale Tax ReportRENJITH K NAIRBelum ada peringkat

- GST AssignmentDokumen16 halamanGST AssignmentDroupathyBelum ada peringkat

- Model Test 8 Userupload - in PDFDokumen54 halamanModel Test 8 Userupload - in PDFMani mechBelum ada peringkat

- Goods and Service Tax - Mba ProjectDokumen10 halamanGoods and Service Tax - Mba Projectsangeetha jBelum ada peringkat

- Deduction & Head of DepositDokumen26 halamanDeduction & Head of DepositAntora HoqueBelum ada peringkat

- FTA VAT Audit FileDokumen2 halamanFTA VAT Audit Filekashif1905Belum ada peringkat

- trắc nghiệm part 2Dokumen39 halamantrắc nghiệm part 2HankhnilBelum ada peringkat

- TAXATIONDokumen3 halamanTAXATIONcherry blossomBelum ada peringkat

- CARELIFT - BIR Form 2550Q VAT RETURN - 4Q 2021Dokumen1 halamanCARELIFT - BIR Form 2550Q VAT RETURN - 4Q 2021Jay Mark DimaanoBelum ada peringkat

- 94-01 General Principles QuestionnaireDokumen12 halaman94-01 General Principles QuestionnaireEpfie SanchesBelum ada peringkat

- Neopost Franking Machines Cut CostsDokumen3 halamanNeopost Franking Machines Cut CostsNeopostUKBelum ada peringkat

- BLock Management System For Enhancement of Revenue CollectionDokumen60 halamanBLock Management System For Enhancement of Revenue CollectionHija S Yange80% (10)

- Taxation Reviewerdocx PDF FreeDokumen17 halamanTaxation Reviewerdocx PDF FreeAlexis Kaye DayagBelum ada peringkat