Anda mungkin juga menyukai

- CHP 15Dokumen73 halamanCHP 15Khaled A. M. El-sherifBelum ada peringkat

- CHP 5Dokumen72 halamanCHP 5Khaled A. M. El-sherifBelum ada peringkat

- CHP 11Dokumen45 halamanCHP 11Khaled A. M. El-sherifBelum ada peringkat

- CHP 8Dokumen61 halamanCHP 8Khaled A. M. El-sherifBelum ada peringkat

- CHP 6Dokumen49 halamanCHP 6Khaled A. M. El-sherifBelum ada peringkat

- Ch1 TFDokumen17 halamanCh1 TFKhaled A. M. El-sherifBelum ada peringkat

- Test Bank For Global Marketing 6th Edition by KeeganDokumen19 halamanTest Bank For Global Marketing 6th Edition by KeeganKhaled A. M. El-sherifBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- TelekomDokumen2 halamanTelekomAnonymous eS7MLJvPZCBelum ada peringkat

- Lesson 1 - Basic Concept of DesignDokumen32 halamanLesson 1 - Basic Concept of DesignSithara BandaraBelum ada peringkat

- Data Sheet Speaker StrobeDokumen4 halamanData Sheet Speaker StrobeAneesh ConstantineBelum ada peringkat

- Standards For Pipes and FittingsDokumen11 halamanStandards For Pipes and FittingsMohammed sabatinBelum ada peringkat

- Catalogo AMF Herramientas para AtornillarDokumen76 halamanCatalogo AMF Herramientas para Atornillarabelmonte_geotecniaBelum ada peringkat

- BloodDokumen22 halamanBloodGodd LlikeBelum ada peringkat

- BIR Form 2307Dokumen20 halamanBIR Form 2307Lean Isidro0% (1)

- Nexys4-DDR RMDokumen29 halamanNexys4-DDR RMDocente Fede TecnologicoBelum ada peringkat

- Sustainable Project Management. The GPM Reference Guide: March 2018Dokumen26 halamanSustainable Project Management. The GPM Reference Guide: March 2018Carlos Andres PinzonBelum ada peringkat

- Geography Cba PowerpointDokumen10 halamanGeography Cba Powerpointapi-489088076Belum ada peringkat

- Geigermullerteller (Nuts and Volts 2004-01)Dokumen5 halamanGeigermullerteller (Nuts and Volts 2004-01)Peeters GuyBelum ada peringkat

- IT Quiz QuestionsDokumen10 halamanIT Quiz QuestionsbrittosabuBelum ada peringkat

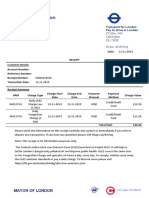

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDokumen1 halamanTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucBelum ada peringkat

- The Development of Silicone Breast Implants That Are Safe FoDokumen5 halamanThe Development of Silicone Breast Implants That Are Safe FomichelleflresmartinezBelum ada peringkat

- Executive Order No. 786, S. 1982Dokumen5 halamanExecutive Order No. 786, S. 1982Angela Igoy-Inac MoboBelum ada peringkat

- Disaster Management in Schools: Status ReportDokumen28 halamanDisaster Management in Schools: Status ReportRamalingam VaradarajuluBelum ada peringkat

- (E-Brochure) Ginza HillDokumen6 halaman(E-Brochure) Ginza HillRenald 'Renald' RenaldBelum ada peringkat

- Nyush Ds Cs Capstone Outline TemplateDokumen2 halamanNyush Ds Cs Capstone Outline TemplateFresh Prince Of NigeriaBelum ada peringkat

- SYLVANIA W6413tc - SMDokumen46 halamanSYLVANIA W6413tc - SMdreamyson1983100% (1)

- 3471A Renault EspaceDokumen116 halaman3471A Renault EspaceThe TrollBelum ada peringkat

- Instruction Manual Series 880 CIU Plus: July 2009 Part No.: 4416.526 Rev. 6Dokumen44 halamanInstruction Manual Series 880 CIU Plus: July 2009 Part No.: 4416.526 Rev. 6nknico100% (1)

- Nammcesa 000010 PDFDokumen1.543 halamanNammcesa 000010 PDFBasel Osama RaafatBelum ada peringkat

- Annex B Brochure Vector and ScorpionDokumen4 halamanAnnex B Brochure Vector and ScorpionomarhanandehBelum ada peringkat

- 20 X 70Dokumen102 halaman20 X 70MatAlengBelum ada peringkat

- Human Resource Information Systems 2nd Edition Kavanagh Test BankDokumen27 halamanHuman Resource Information Systems 2nd Edition Kavanagh Test BankteresamckenzieafvoBelum ada peringkat

- Questionnaire Exercise: Deals Desk Analyst Please Answer Below Questions and Email Your Responses Before First Technical Round of InterviewDokumen2 halamanQuestionnaire Exercise: Deals Desk Analyst Please Answer Below Questions and Email Your Responses Before First Technical Round of InterviewAbhinav SahaniBelum ada peringkat

- Sanction For TestDokumen1 halamanSanction For Testkarim karimBelum ada peringkat

- Design and Analysis of Intez Type Water Tank Using SAP 2000 SoftwareDokumen7 halamanDesign and Analysis of Intez Type Water Tank Using SAP 2000 SoftwareIJRASETPublicationsBelum ada peringkat

- G6Dokumen14 halamanG6Arinah RdhBelum ada peringkat

- Pumpkin Cultivation and PracticesDokumen11 halamanPumpkin Cultivation and PracticesGhorpade GsmBelum ada peringkat