Anda mungkin juga menyukai

- FA - Financial Accounting: Chapter 2 - Regulatory FrameworkDokumen23 halamanFA - Financial Accounting: Chapter 2 - Regulatory FrameworkSumiya YousefBelum ada peringkat

- US GAAP Convergence and IFRSDokumen821 halamanUS GAAP Convergence and IFRSshilamvora100% (2)

- Accounting PDFDokumen16 halamanAccounting PDFHanifah Sekar0% (1)

- Dwnload Full Corporate Financial Accounting 15th Edition Warren Test Bank PDFDokumen27 halamanDwnload Full Corporate Financial Accounting 15th Edition Warren Test Bank PDFhofstadgypsyus100% (16)

- Spring 2022-23 BICA L6Dokumen18 halamanSpring 2022-23 BICA L6MJ jBelum ada peringkat

- IFRSDokumen34 halamanIFRSnav33nBelum ada peringkat

- INTRODUCTIONDokumen44 halamanINTRODUCTIONpadm0% (1)

- Accounting StandardsDokumen47 halamanAccounting StandardsManish SinghBelum ada peringkat

- Matching of Indian Accounting Standard With International AccountingDokumen21 halamanMatching of Indian Accounting Standard With International AccountingSwati Rawat25% (4)

- International Financial Reporting StandardsDokumen11 halamanInternational Financial Reporting Standardscreepy444Belum ada peringkat

- International Accounting and Auditing Standards: by Dr. Ayesha RehanDokumen22 halamanInternational Accounting and Auditing Standards: by Dr. Ayesha Rehanabubakr zulfiqarBelum ada peringkat

- Lux Gaap - Ifrs-Us GaapDokumen32 halamanLux Gaap - Ifrs-Us GaapPavel MochalinBelum ada peringkat

- 1 Ifrs Ias 1-AccaDokumen265 halaman1 Ifrs Ias 1-AccaSabrina Aeni100% (1)

- PS2Dokumen14 halamanPS2yulianaBelum ada peringkat

- International Financial Reporting Standards (IFRS)Dokumen74 halamanInternational Financial Reporting Standards (IFRS)Ashutosh GuptaBelum ada peringkat

- Harmonizing Financial Reporting A Study of International Financial Reporting Standards (IFRS)Dokumen57 halamanHarmonizing Financial Reporting A Study of International Financial Reporting Standards (IFRS)pomater270Belum ada peringkat

- Accounting For Manager Cat 3Dokumen12 halamanAccounting For Manager Cat 3Aviral UtkarshBelum ada peringkat

- Acc 101 Topic 1 2024 (Autosaved)Dokumen83 halamanAcc 101 Topic 1 2024 (Autosaved)severinmsangiBelum ada peringkat

- ICAP Chapter CPD KhobarDokumen75 halamanICAP Chapter CPD Khobarfarhantariq_89Belum ada peringkat

- Accounting For Managers: Leasing Concept Under IfrsDokumen9 halamanAccounting For Managers: Leasing Concept Under Ifrsvarshini sureshBelum ada peringkat

- International Accounting Standards 2007 NewDokumen48 halamanInternational Accounting Standards 2007 NewADITYA MAHAJAN100% (1)

- AcFn 511-Ch II Ppt-LK-2020 - Part One-2Dokumen110 halamanAcFn 511-Ch II Ppt-LK-2020 - Part One-2Chilot YihuneBelum ada peringkat

- Accounting Standards - E-Notes - Udesh Regular - Group 1Dokumen135 halamanAccounting Standards - E-Notes - Udesh Regular - Group 1Uday TomarBelum ada peringkat

- NFRS Convergences (Final) 21Dokumen71 halamanNFRS Convergences (Final) 21Menuka BaralBelum ada peringkat

- IFRSDokumen10 halamanIFRSjctfy8tmrfBelum ada peringkat

- Presented by Muhammad Shahbaz Tahir Bs Commerce-V 21BSCM018Dokumen16 halamanPresented by Muhammad Shahbaz Tahir Bs Commerce-V 21BSCM018Abdul RehmanBelum ada peringkat

- 5 Edch 06Dokumen24 halaman5 Edch 06Ahmed HajaliBelum ada peringkat

- The Financial Reporting Environment: Corporate Accounting & Reporting I Semester 1, 19/20 Hojun SeoDokumen78 halamanThe Financial Reporting Environment: Corporate Accounting & Reporting I Semester 1, 19/20 Hojun SeoLiu JiangBelum ada peringkat

- International Financial Reporting Standards (IFRS) : Lecture 1: Introduction To IFRSDokumen53 halamanInternational Financial Reporting Standards (IFRS) : Lecture 1: Introduction To IFRSegeyuece1996Belum ada peringkat

- 2 The Regulatory Framework - PPSXDokumen13 halaman2 The Regulatory Framework - PPSXAbdelwahab Ahmed IbrahimBelum ada peringkat

- A - Intro To IASBDokumen4 halamanA - Intro To IASBKaryl FailmaBelum ada peringkat

- 655eda81374b680018b844d6 ## E-Books Accounting StandardsDokumen376 halaman655eda81374b680018b844d6 ## E-Books Accounting Standardspavangaming2811Belum ada peringkat

- International Accounting Standards (IAS)Dokumen10 halamanInternational Accounting Standards (IAS)Om Prakash AgrawalBelum ada peringkat

- Conceptual Framework & Accounting StandardsDokumen4 halamanConceptual Framework & Accounting StandardsEila PBelum ada peringkat

- Overview of Financial Reporting Environment Environment: FRS Course DR Sudershan Kuntluru IIM KozhikodeDokumen35 halamanOverview of Financial Reporting Environment Environment: FRS Course DR Sudershan Kuntluru IIM KozhikodeKumar PrashantBelum ada peringkat

- Development of Financial Reporting Framework and Standard-Setting BodiesDokumen4 halamanDevelopment of Financial Reporting Framework and Standard-Setting BodiesJosua PagcaliwaganBelum ada peringkat

- Chapter 1: Financial Accounting and Accounting StandardsDokumen19 halamanChapter 1: Financial Accounting and Accounting StandardsDaniyal WahabBelum ada peringkat

- ACYFAR 1 - Unit 1 - Standard SettingDokumen10 halamanACYFAR 1 - Unit 1 - Standard SettingPaula Grace MedranoBelum ada peringkat

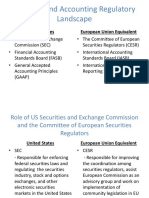

- Financial and Accounting Regulatory LandscapeDokumen7 halamanFinancial and Accounting Regulatory LandscapeDiana Mindru StrenerBelum ada peringkat

- IFRS BasicsDokumen86 halamanIFRS BasicsManisha DeyBelum ada peringkat

- Chapter 1: Financial Accounting and Accounting StandardsDokumen19 halamanChapter 1: Financial Accounting and Accounting StandardsjnfebrinaBelum ada peringkat

- IAS-01 and IAS-08 AsmatDokumen66 halamanIAS-01 and IAS-08 AsmatAli ZaidiBelum ada peringkat

- Nepal Accounting StandardDokumen47 halamanNepal Accounting StandardShreejan Bhandari100% (3)

- Accounting Standard 1: By: Manju Asht Lfbaa LPU PhagwaraDokumen19 halamanAccounting Standard 1: By: Manju Asht Lfbaa LPU PhagwaraanmoldeepsinghBelum ada peringkat

- Ifrs Unit 1Dokumen9 halamanIfrs Unit 1Deven LadBelum ada peringkat

- معايير CH1-IntroductionDokumen19 halamanمعايير CH1-IntroductionHamza MahmoudBelum ada peringkat

- 13A AS BasicsDokumen9 halaman13A AS BasicsrazorBelum ada peringkat

- IFRSDokumen11 halamanIFRSShekhar SinghBelum ada peringkat

- International Financial Reporting Standards and Philippine Financial Reporting StandardsDokumen12 halamanInternational Financial Reporting Standards and Philippine Financial Reporting StandardsLilian LagrimasBelum ada peringkat

- Accounting BasicsDokumen44 halamanAccounting BasicsHarsh GhaiBelum ada peringkat

- Accounting 1Dokumen16 halamanAccounting 1Praveen KewlaniBelum ada peringkat

- ACCT 860: Financial Accounting Week 1: NZ External Reporting EnvironmentDokumen36 halamanACCT 860: Financial Accounting Week 1: NZ External Reporting EnvironmentNam PhamBelum ada peringkat

- International Accounting StandardsDokumen10 halamanInternational Accounting StandardsRameshwar FundipalleBelum ada peringkat

- Lecture 3,4Dokumen21 halamanLecture 3,4shumailaBelum ada peringkat

- Lecture 1 FSADokumen26 halamanLecture 1 FSAvuthithuylinh9a007Belum ada peringkat

- F7-01 International Financial Reporting StandardsDokumen16 halamanF7-01 International Financial Reporting Standardssayedrushdi100% (1)

- ACCG835 International AccountingDokumen41 halamanACCG835 International AccountingSophie DaoBelum ada peringkat

- Propsed BooksDokumen8 halamanPropsed BooksOmer AwanBelum ada peringkat

- Ipev Versus IlpaDokumen5 halamanIpev Versus IlpaTarek MghBelum ada peringkat

- Accounting Standards in PakistanDokumen17 halamanAccounting Standards in PakistanMuneeb AliBelum ada peringkat

- Chapter 1 - The Accountancy ProfessionDokumen20 halamanChapter 1 - The Accountancy Professioncastleraven04Belum ada peringkat

- Ifrs 170120102142Dokumen10 halamanIfrs 170120102142ajayBelum ada peringkat

- Financial Accounting and Reporting Study Guide NotesDari EverandFinancial Accounting and Reporting Study Guide NotesPenilaian: 1 dari 5 bintang1/5 (1)

- Unit 9 Employee Safety and HealthDokumen28 halamanUnit 9 Employee Safety and Healthginish12Belum ada peringkat

- China Southern Internet Check-In Boarding Pass2Dokumen2 halamanChina Southern Internet Check-In Boarding Pass2ginish12Belum ada peringkat

- Presentation On Application Software and Software IssuesDokumen23 halamanPresentation On Application Software and Software Issuesginish12Belum ada peringkat

- ScholarDokumen1 halamanScholarginish12Belum ada peringkat

- 1 CoverpageDokumen4 halaman1 CoverpagePiyal HossainBelum ada peringkat

- ScholarDokumen1 halamanScholarginish12Belum ada peringkat

- Unit 3 Employee SelectionDokumen68 halamanUnit 3 Employee Selectionginish12Belum ada peringkat

- Unit 5 Performance Management and AppraisalDokumen63 halamanUnit 5 Performance Management and Appraisalginish12Belum ada peringkat

- Unit 7 Labor Relations and Collective BargainingDokumen79 halamanUnit 7 Labor Relations and Collective Bargainingginish12Belum ada peringkat

- Unit 2 Personnel Planning and RecruitmentDokumen70 halamanUnit 2 Personnel Planning and Recruitmentginish12Belum ada peringkat

- Unit 6 Employee CompensationDokumen48 halamanUnit 6 Employee Compensationginish12Belum ada peringkat

- Assignment - 1Dokumen4 halamanAssignment - 1ginish12Belum ada peringkat

- Unit 8 Ethics and Fair Treatment in Human Resources ManagementDokumen56 halamanUnit 8 Ethics and Fair Treatment in Human Resources Managementginish12Belum ada peringkat

- Unit 4 Employee Training and DevelopmentDokumen50 halamanUnit 4 Employee Training and Developmentginish12Belum ada peringkat

- Case Analysis FormatDokumen1 halamanCase Analysis Formatginish12Belum ada peringkat

- Dhankuta RESDokumen18 halamanDhankuta RESginish12Belum ada peringkat

- Unit 1 Overview of The FieldDokumen46 halamanUnit 1 Overview of The Fieldginish12Belum ada peringkat

- Path - Goal TheoryDokumen10 halamanPath - Goal Theoryginish12Belum ada peringkat

- Potato ChipsDokumen11 halamanPotato Chipsginish12Belum ada peringkat

- Potato ChipsDokumen11 halamanPotato Chipsginish12Belum ada peringkat

- Buddha Air CaseDokumen3 halamanBuddha Air Caseginish12Belum ada peringkat

- Broadly Defined and Team Based JobsDokumen13 halamanBroadly Defined and Team Based Jobsginish12Belum ada peringkat

- MBO DeviationDokumen1 halamanMBO Deviationginish12Belum ada peringkat

- Measurement Scale SlideDokumen40 halamanMeasurement Scale Slideginish12Belum ada peringkat

- Assignment 2Dokumen4 halamanAssignment 2ginish12Belum ada peringkat

- LeanDokumen1 halamanLeanginish12Belum ada peringkat

- Slide 4Dokumen15 halamanSlide 4ginish12Belum ada peringkat

- WP IHR PerformanceManagement 0319Dokumen7 halamanWP IHR PerformanceManagement 0319Archana PooniaBelum ada peringkat

- Demand Conditions Factor Conditions Related and Supporting Industries Firm Strategy, Structure, and RivalryDokumen5 halamanDemand Conditions Factor Conditions Related and Supporting Industries Firm Strategy, Structure, and Rivalryginish12Belum ada peringkat

- How Stressful Is Your LifeDokumen1 halamanHow Stressful Is Your Lifeginish12Belum ada peringkat

- Allen Stanford Criminal Trial Transcript Volume 9 Feb. 2, 2012Dokumen303 halamanAllen Stanford Criminal Trial Transcript Volume 9 Feb. 2, 2012Stanford Victims CoalitionBelum ada peringkat

- Solution Manual For Intermediate Accounting 17th by KiesoDokumen36 halamanSolution Manual For Intermediate Accounting 17th by Kiesozirconic.dzeron.8oyy100% (46)

- IP Valuation FinalDokumen46 halamanIP Valuation FinalNancy EkkaBelum ada peringkat

- Fair Value Measurement: Questions and AnswersDokumen162 halamanFair Value Measurement: Questions and AnswersNomanBelum ada peringkat

- International Accounting - SwiftDokumen7 halamanInternational Accounting - Swiftzhayang1129Belum ada peringkat

- Accounting PrinciplesDokumen1 halamanAccounting PrinciplesM Bilal Malik100% (1)

- Case 1 2Dokumen9 halamanCase 1 2rohanfyaz00Belum ada peringkat

- Acc Theory Question Assignment 3Dokumen13 halamanAcc Theory Question Assignment 3Stephanie HerlambangBelum ada peringkat

- Impact of Factors On Fair Value Accounting: Empirical Study in VietnamDokumen18 halamanImpact of Factors On Fair Value Accounting: Empirical Study in VietnamJulia NavarroBelum ada peringkat

- © 2009 Pearson Education, Inc Publishing As Prentice HallDokumen6 halaman© 2009 Pearson Education, Inc Publishing As Prentice Hallb-80815bBelum ada peringkat

- CONCEPTUAL FRAMEWORK LEVELS 1 and 2 AnswersDokumen4 halamanCONCEPTUAL FRAMEWORK LEVELS 1 and 2 AnswersPrincess ReyesBelum ada peringkat

- Foreclosure Affidavit Cog1Dokumen15 halamanForeclosure Affidavit Cog1Bhakta Prakash100% (7)

- GaapDokumen7 halamanGaapjoyceBelum ada peringkat

- Resume Albeiro Acosta - Accountant - Auditor and ControllerDokumen3 halamanResume Albeiro Acosta - Accountant - Auditor and ControllerALbeiro AcostaBelum ada peringkat

- ACCA F7int ATC Study Text 2012Dokumen562 halamanACCA F7int ATC Study Text 2012hamid2k30100% (4)

- Financial Accounting by DrummerDokumen48 halamanFinancial Accounting by DrummershabahatanwaraliBelum ada peringkat

- GAAP: Understanding It and The 10 Key Principles: U.S. Public Companies Must Follow GAAP For Their Financial StatementsDokumen1 halamanGAAP: Understanding It and The 10 Key Principles: U.S. Public Companies Must Follow GAAP For Their Financial StatementsThuraBelum ada peringkat

- Fasb 121 PDFDokumen2 halamanFasb 121 PDFTonyBelum ada peringkat

- Ifrs For Techn Com Closing The GaapDokumen40 halamanIfrs For Techn Com Closing The GaappipppopBelum ada peringkat

- Test Bank For Government and Not For Profit Accounting Concepts and Practices 5th Edition GranofDokumen15 halamanTest Bank For Government and Not For Profit Accounting Concepts and Practices 5th Edition GranofChristine TiceBelum ada peringkat

- Amsalu GelanehDokumen106 halamanAmsalu GelanehKalayu KirosBelum ada peringkat

- Busn 5 5th Edition Kelly Solutions ManualDokumen38 halamanBusn 5 5th Edition Kelly Solutions Manualkrystalsaunderss0on100% (17)

- Wey Ifrs 4e PPT ch01Dokumen38 halamanWey Ifrs 4e PPT ch01abudayahrubaBelum ada peringkat

- Accounting Concept and Practice: Accounting A Malaysian Perspective 5eDokumen63 halamanAccounting Concept and Practice: Accounting A Malaysian Perspective 5eCarmenn LouBelum ada peringkat

- Conceptual FW TestbankDokumen2 halamanConceptual FW Testbanktres gian de guzmanBelum ada peringkat

- GAAP vs. IFRS What's The DifferenceDokumen1 halamanGAAP vs. IFRS What's The DifferenceHafisMohammedSahibBelum ada peringkat

- Auditing Multiple ChoiceDokumen11 halamanAuditing Multiple Choiceunique_vn100% (1)