Anda mungkin juga menyukai

- Schedule 1 For 2019 Form 1040Dokumen1 halamanSchedule 1 For 2019 Form 1040CNBC.comBelum ada peringkat

- Surface CatalogDokumen76 halamanSurface CatalogAnonymous KzJcjGCJbBelum ada peringkat

- Ivory: SIEGFRIED LTD - CIPAN-Companhia Industrial Productora de Antibioticos, SA, Lisboa - PortugalDokumen1 halamanIvory: SIEGFRIED LTD - CIPAN-Companhia Industrial Productora de Antibioticos, SA, Lisboa - PortugalnileshgjBelum ada peringkat

- Foundations Their Power and Influence by Rene A Wormser 438Dokumen438 halamanFoundations Their Power and Influence by Rene A Wormser 438Keith Knight100% (1)

- Micro Banking Sector Report Centrum 14072016Dokumen72 halamanMicro Banking Sector Report Centrum 14072016Ankur MittalBelum ada peringkat

- Tata Project ReportDokumen205 halamanTata Project Reporttanvisawal1079% (19)

- 2014 2 10 COSO Thought PaperDokumen32 halaman2014 2 10 COSO Thought PaperEsther OuBelum ada peringkat

- Easa-147-Uk Approved Basic Training OrganisationsDokumen17 halamanEasa-147-Uk Approved Basic Training OrganisationsPavlos TsitswnisBelum ada peringkat

- Credit Appraisal Techniques Od IdbiDokumen28 halamanCredit Appraisal Techniques Od Idbikamma175% (4)

- Tata MotorsDokumen66 halamanTata Motorsadityaraman84977% (13)

- Complete Project Commodity Market Commodity Market ModifiedDokumen57 halamanComplete Project Commodity Market Commodity Market ModifiedDid475% (20)

- Hindustan UnileverDokumen23 halamanHindustan UnileverMOHD.ARISHBelum ada peringkat

- Registered Delegates List UPIS 2018Dokumen241 halamanRegistered Delegates List UPIS 2018SheebaBelum ada peringkat

- Project On TATA Motors by Nilesh Manghwani, Sinhgad Institute of Business Administration and Research Pune 48Dokumen54 halamanProject On TATA Motors by Nilesh Manghwani, Sinhgad Institute of Business Administration and Research Pune 48nilesh SIBAR pune 4888% (17)

- Industrial Credit and Investment Corporation of IndiaDokumen31 halamanIndustrial Credit and Investment Corporation of IndiaBhadra PriyaBelum ada peringkat

- Icici Bank: CMP: INR502 Operating Performance Resilient Technology Remains Key Growth DriverDokumen14 halamanIcici Bank: CMP: INR502 Operating Performance Resilient Technology Remains Key Growth DriverRajat GroverBelum ada peringkat

- Institute of Management Studies: Devi Ahilya Vishwavidyalaya, IndoreDokumen22 halamanInstitute of Management Studies: Devi Ahilya Vishwavidyalaya, Indoreneelabh_singh_1Belum ada peringkat

- IDFC First Initial (Key Note)Dokumen26 halamanIDFC First Initial (Key Note)beza manojBelum ada peringkat

- Group - 4 Group - 4: - Bishnu - Ranjeet - Srinivas - Irannas - Bishnu - Ranjeet - Srinivas - IrannasDokumen29 halamanGroup - 4 Group - 4: - Bishnu - Ranjeet - Srinivas - Irannas - Bishnu - Ranjeet - Srinivas - IrannassrinivasatnccBelum ada peringkat

- JM IciciDokumen18 halamanJM IciciSanjay PatelBelum ada peringkat

- Investor Presentation: January 28, 2000Dokumen41 halamanInvestor Presentation: January 28, 2000ritushah05Belum ada peringkat

- Power Pack BankingDokumen26 halamanPower Pack BankingDev DugarBelum ada peringkat

- Asset Reconstruction CompanyDokumen55 halamanAsset Reconstruction Companyjitesh60% (5)

- Working Capital Management Related Report UtsavDokumen8 halamanWorking Capital Management Related Report UtsavPradip MehtaBelum ada peringkat

- MNCL Diwali PicksDokumen12 halamanMNCL Diwali PicksRick DasBelum ada peringkat

- New Banking License Catalyst For Consolidation 081010Dokumen3 halamanNew Banking License Catalyst For Consolidation 081010kotler_2006Belum ada peringkat

- A Comparative Study of Nationalized & Private Banks With Respect To Loan Process & Facilities For SmesDokumen37 halamanA Comparative Study of Nationalized & Private Banks With Respect To Loan Process & Facilities For SmeskhalidBelum ada peringkat

- Research Report On CRMDokumen20 halamanResearch Report On CRMKanta SharminBelum ada peringkat

- Bajaj FinanceDokumen19 halamanBajaj FinanceAmar50% (2)

- New Approaches To SME Finance Using Bank Account Information (Big Data)Dokumen19 halamanNew Approaches To SME Finance Using Bank Account Information (Big Data)ADBI EventsBelum ada peringkat

- Group 14: Meet Mehta Umang Kumar Ayushi Jaiswal Ayon DasDokumen12 halamanGroup 14: Meet Mehta Umang Kumar Ayushi Jaiswal Ayon DasUmang KBelum ada peringkat

- SBI AR 2019 English PDFDokumen260 halamanSBI AR 2019 English PDFprakash kambleBelum ada peringkat

- MBA (2020-22) Trimester-II, End-Term Exaination, Feruary 2021Dokumen6 halamanMBA (2020-22) Trimester-II, End-Term Exaination, Feruary 2021subhasis mahapatraBelum ada peringkat

- Sapm 4Dokumen12 halamanSapm 4Sweet tripathiBelum ada peringkat

- 2017 SMIC Lo PDFDokumen128 halaman2017 SMIC Lo PDFBjay AledonBelum ada peringkat

- Banking 3Dokumen33 halamanBanking 3Nikhitha ShettyBelum ada peringkat

- Supply Chain of IciciDokumen17 halamanSupply Chain of Icicishan birla100% (1)

- ISec Business Presentation Investor Conference August 2019Dokumen35 halamanISec Business Presentation Investor Conference August 2019Bhagwan BachaiBelum ada peringkat

- Channel ConnectDokumen24 halamanChannel ConnectJagadish LoganathanBelum ada peringkat

- GTB - Obc MergerDokumen5 halamanGTB - Obc MergermeetwithsanjayBelum ada peringkat

- Financial Sector Performance and System Stability: 8.1 OverviewDokumen52 halamanFinancial Sector Performance and System Stability: 8.1 OverviewdevBelum ada peringkat

- Project Report A Study On Performance Evaluation of Icici and Sbi Using Fundamental and Technical AnalysisDokumen49 halamanProject Report A Study On Performance Evaluation of Icici and Sbi Using Fundamental and Technical AnalysisNaga DeepuBelum ada peringkat

- SBI LTD Initiating Coverage 19062020Dokumen8 halamanSBI LTD Initiating Coverage 19062020Devendra rautBelum ada peringkat

- Industry Visit Group13Dokumen26 halamanIndustry Visit Group13ANUPAM ROYBelum ada peringkat

- Final Project Sbi (Niddhi)Dokumen32 halamanFinal Project Sbi (Niddhi)Shraddha GaikwadBelum ada peringkat

- Banking: Presented by Sonam DesaiDokumen33 halamanBanking: Presented by Sonam DesaiSonam DesaiBelum ada peringkat

- Bank Management: PGDM Iimc 2020 Praloy MajumderDokumen40 halamanBank Management: PGDM Iimc 2020 Praloy MajumderLiontiniBelum ada peringkat

- Group2 IndusInd Bank FinalDokumen13 halamanGroup2 IndusInd Bank FinalPragyna ThotaBelum ada peringkat

- IFB Ethiopia Report PDFDokumen3 halamanIFB Ethiopia Report PDFfeyselBelum ada peringkat

- SBI Bank Ratio AnalysisDokumen19 halamanSBI Bank Ratio AnalysisIshita TrivediBelum ada peringkat

- CMD 2022 PresentationDokumen130 halamanCMD 2022 Presentationvamsi.iitkBelum ada peringkat

- ICICI BANK - ResearchDokumen1 halamanICICI BANK - ResearchankitBelum ada peringkat

- IDirect Fino IPOReviewDokumen10 halamanIDirect Fino IPOReviewkesavan91Belum ada peringkat

- Growth Story & Successful Market EntryDokumen14 halamanGrowth Story & Successful Market Entryrajshekhar87Belum ada peringkat

- ICICI Securities Ltd. Campus Placement - FY 24Dokumen15 halamanICICI Securities Ltd. Campus Placement - FY 24Ritik vermaBelum ada peringkat

- 4Q 2020 - Analyst Meeting (LONG FORM)Dokumen80 halaman4Q 2020 - Analyst Meeting (LONG FORM)Giang NguyenBelum ada peringkat

- Equitas Small Finance Bank Company UpdateDokumen10 halamanEquitas Small Finance Bank Company Updatefinal bossuBelum ada peringkat

- SI PPT - Group 5Dokumen20 halamanSI PPT - Group 5Siddharth KumarBelum ada peringkat

- Bank Profitability in India Since Post Reform PeriodDokumen11 halamanBank Profitability in India Since Post Reform PeriodSubinay BiswasBelum ada peringkat

- Centrum On Jio Financial Services Fuel in Place, Engine About ToDokumen5 halamanCentrum On Jio Financial Services Fuel in Place, Engine About ToSantosh KumarBelum ada peringkat

- State Bank of India: Financial Analysis 2018-2019Dokumen9 halamanState Bank of India: Financial Analysis 2018-2019Mera Birthday 2021Belum ada peringkat

- Publikasi - PT Hasjrat Multifinance 20082019 01092020Dokumen1 halamanPublikasi - PT Hasjrat Multifinance 20082019 01092020Imam M DarwisBelum ada peringkat

- Banking SectorDokumen14 halamanBanking SectorVivek S MayinkarBelum ada peringkat

- FEL ReportDokumen14 halamanFEL ReportAteeque MohdBelum ada peringkat

- SyngeneDokumen12 halamanSyngeneIndraneel MahantiBelum ada peringkat

- Indiabulls ThesisDokumen5 halamanIndiabulls Thesisdivyanshu kumarBelum ada peringkat

- Neo BankingDokumen19 halamanNeo BankingVenkatesh YelnoorkarBelum ada peringkat

- L29-Shadow and NBFCDokumen20 halamanL29-Shadow and NBFCMrigankshi KapoorBelum ada peringkat

- IndusInd Bank Limited EP 2023-07-18 EnglishDokumen39 halamanIndusInd Bank Limited EP 2023-07-18 EnglishSubham JainBelum ada peringkat

- SBI Cards and Payments: Long-Term Outlook Remains IntactDokumen6 halamanSBI Cards and Payments: Long-Term Outlook Remains IntactRomelu MartialBelum ada peringkat

- SBI Cards and Payment Services LTD: SubscribeDokumen16 halamanSBI Cards and Payment Services LTD: Subscribejpsmu09Belum ada peringkat

- Summer Training Project Report: Banasthali University C-Scheme Jaipur Campus, RajasthanDokumen74 halamanSummer Training Project Report: Banasthali University C-Scheme Jaipur Campus, Rajasthandrdipin100% (3)

- Chapter 3 - MKTG of Industrial GoodsDokumen19 halamanChapter 3 - MKTG of Industrial Goodswasi28Belum ada peringkat

- Tata Motors Final ReportDokumen50 halamanTata Motors Final Reportwasi28Belum ada peringkat

- Tata Project ReportDokumen253 halamanTata Project Reportwasi28Belum ada peringkat

- 634356252737907500Dokumen45 halaman634356252737907500wasi28Belum ada peringkat

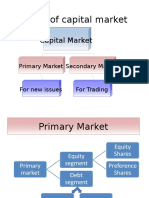

- 2 CHAPTER Primary MarketDokumen17 halaman2 CHAPTER Primary Marketwasi28Belum ada peringkat

- Mor Icici India EFfDDokumen33 halamanMor Icici India EFfDwasi28Belum ada peringkat

- Annual 030502Dokumen40 halamanAnnual 030502wasi28Belum ada peringkat

- Company Full NamesDokumen22 halamanCompany Full Nameswasi28Belum ada peringkat

- Project On Tata MotorsDokumen15 halamanProject On Tata Motorsayush kumar singh95% (37)

- Icici Bank: E-Finance For Development - An Indian PerspectiveDokumen33 halamanIcici Bank: E-Finance For Development - An Indian Perspectivewasi28Belum ada peringkat

- Juned Memon Project On 'Asp'Dokumen85 halamanJuned Memon Project On 'Asp'wasi28Belum ada peringkat

- Summer Project FormatDokumen30 halamanSummer Project Formattisraaa100% (1)

- Advanced Financial ServicesDokumen7 halamanAdvanced Financial Serviceswasi28Belum ada peringkat

- Icici Bank: E-Finance For Development - An Indian PerspectiveDokumen33 halamanIcici Bank: E-Finance For Development - An Indian Perspectivewasi28Belum ada peringkat

- 2 Chapter-Capital MarketDokumen17 halaman2 Chapter-Capital Marketwasi28Belum ada peringkat

- Introduction To Research Methods: Institute For International Management and TechnologyDokumen20 halamanIntroduction To Research Methods: Institute For International Management and Technologywasi28Belum ada peringkat

- 1 Chapter-IndianFinancial SystemDokumen21 halaman1 Chapter-IndianFinancial Systemwasi28Belum ada peringkat

- Prepared By: Dewasish GhoshalDokumen46 halamanPrepared By: Dewasish Ghoshalwasi28Belum ada peringkat

- Mor Icici India EFfDDokumen33 halamanMor Icici India EFfDwasi28Belum ada peringkat

- Annual 030502Dokumen40 halamanAnnual 030502wasi28Belum ada peringkat

- Stratified Random SamplingDokumen8 halamanStratified Random Samplingwasi28Belum ada peringkat

- FMCGPPT 090826130210 Phpapp02Dokumen22 halamanFMCGPPT 090826130210 Phpapp02Khyati MistryBelum ada peringkat

- China in Burma Update 2008 - BurmeseDokumen67 halamanChina in Burma Update 2008 - Burmese33koko97100% (1)

- Rangkuman Studi KasusDokumen5 halamanRangkuman Studi KasusCiao KumustáBelum ada peringkat

- The Timeline of The Apple Computer 1Dokumen29 halamanThe Timeline of The Apple Computer 1Nida MahmoodBelum ada peringkat

- 2000Dokumen48 halaman2000Mike YaunaBelum ada peringkat

- Etf Guide PDFDokumen2 halamanEtf Guide PDFFalconsBelum ada peringkat

- Presentation On Accounts: - Submitted To: Bhavik Sir - Prepared By: - Vipul Gohil (028) - Vishal PatelDokumen21 halamanPresentation On Accounts: - Submitted To: Bhavik Sir - Prepared By: - Vipul Gohil (028) - Vishal Patelrucha4478Belum ada peringkat

- Cengage Learning's Chapter 11 PetitionDokumen22 halamanCengage Learning's Chapter 11 PetitionDealBook50% (2)

- Beams 11 PPT 16 PartnershipsDokumen49 halamanBeams 11 PPT 16 PartnershipsNovriyanti Wahyu HapsariBelum ada peringkat

- WDC DemergerDokumen7 halamanWDC DemergerJTBelum ada peringkat

- Ranbaxy Daiichi Sankyo FinalDokumen42 halamanRanbaxy Daiichi Sankyo Finalarunrathore_28Belum ada peringkat

- Senior Tax Accountant in Orlando FL Resume Maria ClaudioDokumen3 halamanSenior Tax Accountant in Orlando FL Resume Maria ClaudioMariaClaudio2Belum ada peringkat

- Chapter7 TestbankDokumen10 halamanChapter7 TestbankKim Uyên Nguyen Ngoc100% (2)

- VA L SubaccountsDokumen2 halamanVA L SubaccountsSteve KravitzBelum ada peringkat

- Book 1Dokumen4 halamanBook 1Moneylife FoundationBelum ada peringkat

- Evaluation of Performance-Linked Remuneration of Small and Medium-Sized Enterprises (Smes) in Bacolod CityDokumen3 halamanEvaluation of Performance-Linked Remuneration of Small and Medium-Sized Enterprises (Smes) in Bacolod CityKhayceePadillaBelum ada peringkat

- Account Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen14 halamanAccount Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAartiBelum ada peringkat

- Lehman Brothers Motion To Pay SettlementDokumen123 halamanLehman Brothers Motion To Pay SettlementDealBookBelum ada peringkat

- SBI Interest Rates - Oct 2010Dokumen2 halamanSBI Interest Rates - Oct 2010Bharani SomasundaraBelum ada peringkat

- KFC SynopsisDokumen7 halamanKFC SynopsisBhanu SainiBelum ada peringkat

- Accounting For Partnerships-4Dokumen21 halamanAccounting For Partnerships-4DangCongKhoiBelum ada peringkat

- Capgemini:: Cap UkDokumen3 halamanCapgemini:: Cap UkAnonymous SaSHDMvLBelum ada peringkat

- Data Management Outsourcing Agreement - Allstate Insurance Co. and Acxiom CorpDokumen43 halamanData Management Outsourcing Agreement - Allstate Insurance Co. and Acxiom CorpBIPINBelum ada peringkat

- A Study On Financial Inclusion Initiation by State Bank of IndiaDokumen5 halamanA Study On Financial Inclusion Initiation by State Bank of IndiavmktptBelum ada peringkat