Anda mungkin juga menyukai

- Understanding Working Capital Needs and Financing OptionsDokumen66 halamanUnderstanding Working Capital Needs and Financing OptionsAamit KumarBelum ada peringkat

- Capital Budgeting Decisions ExplainedDokumen21 halamanCapital Budgeting Decisions ExplainedSureshArigelaBelum ada peringkat

- Advanced Financial Managment FinalDokumen9 halamanAdvanced Financial Managment FinalMohit BBelum ada peringkat

- IFM Transfer PricingDokumen9 halamanIFM Transfer PricingPooja Ujjwal JainBelum ada peringkat

- Cost of CapitalDokumen19 halamanCost of CapitalADITYA KUMARBelum ada peringkat

- Guide to Assignment Submission (39Dokumen3 halamanGuide to Assignment Submission (39Muhammad Safiuddin KhanBelum ada peringkat

- Accounting For Groups of CompaniesDokumen9 halamanAccounting For Groups of CompaniesEmmanuel MwapeBelum ada peringkat

- ICMAB's Intro to Cost AuditDokumen144 halamanICMAB's Intro to Cost AuditHasanur RaselBelum ada peringkat

- Chapter 6 (CF)Dokumen51 halamanChapter 6 (CF)Hossain BelalBelum ada peringkat

- Dividend Policy ExplainedDokumen13 halamanDividend Policy ExplainedMohammad MoosaBelum ada peringkat

- Strategic Cost Management Concepts ExplainedDokumen6 halamanStrategic Cost Management Concepts ExplainedCA Mohit SharmaBelum ada peringkat

- SMA NotesDokumen129 halamanSMA Notessanu sayedBelum ada peringkat

- Chapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)Dokumen8 halamanChapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)NasrinTonni AhmedBelum ada peringkat

- Letter of Credit: Give Assurance To Your Sellers With ICICI Bank's Letter of CreditDokumen2 halamanLetter of Credit: Give Assurance To Your Sellers With ICICI Bank's Letter of CreditSanjay ShingalaBelum ada peringkat

- 35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc MsDokumen90 halaman35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc Msmysorevishnu75% (8)

- Chapter-21 (Web Chapter)Dokumen27 halamanChapter-21 (Web Chapter)g23111Belum ada peringkat

- Acca F9 Business ValuationsDokumen6 halamanAcca F9 Business ValuationsHaseeb SethyBelum ada peringkat

- Lease financing types and rationaleDokumen13 halamanLease financing types and rationaleJay KishanBelum ada peringkat

- Synopsis of Corporate GovernanceDokumen14 halamanSynopsis of Corporate GovernanceApoorv SrivastavaBelum ada peringkat

- Auditing Ethics: Lecture # 2 Fundamental PrinciplesDokumen3 halamanAuditing Ethics: Lecture # 2 Fundamental PrinciplessiddiqueicmaBelum ada peringkat

- What Is Strategic Financial ManagementDokumen10 halamanWhat Is Strategic Financial Managementpra leshBelum ada peringkat

- Throughput Accounting-AccaDokumen25 halamanThroughput Accounting-AccaDamalai YansanehBelum ada peringkat

- Chapter 6 - Review of Capital Budgeting Techniques - Part 1Dokumen10 halamanChapter 6 - Review of Capital Budgeting Techniques - Part 1Abdelrahman Maged0% (1)

- Capital Structure TheoriesDokumen47 halamanCapital Structure Theoriesamol_more37Belum ada peringkat

- YTMDokumen1 halamanYTMMadhavKishoreBelum ada peringkat

- KOCH6Dokumen63 halamanKOCH6Swati SoniBelum ada peringkat

- Introduction of Corporate GovernanceDokumen8 halamanIntroduction of Corporate GovernanceHasanur RaselBelum ada peringkat

- Financial Management Chapter 09 IM 10th EdDokumen24 halamanFinancial Management Chapter 09 IM 10th EdDr Rushen SinghBelum ada peringkat

- Fair Value Adjustment and Consolidation Adjustment Week 2Dokumen9 halamanFair Value Adjustment and Consolidation Adjustment Week 2Omolaja IbukunBelum ada peringkat

- Ratio Analysis Notes (Theory)Dokumen3 halamanRatio Analysis Notes (Theory)Karishma KatiyarBelum ada peringkat

- Chapter 6 Discounted Cash Flow ValuationDokumen27 halamanChapter 6 Discounted Cash Flow ValuationAhmed Fathelbab100% (1)

- Cost of CapitalDokumen34 halamanCost of CapitalShubham SinghBelum ada peringkat

- Chapter 18 Explains Key Aspects of LeasingDokumen4 halamanChapter 18 Explains Key Aspects of LeasingTham Ru JieBelum ada peringkat

- UNIZIM ACCN Business Accounting Course OutlineDokumen7 halamanUNIZIM ACCN Business Accounting Course OutlineEverjoice Chatora100% (1)

- IFS Unit-1 Notes - 20200717114457Dokumen9 halamanIFS Unit-1 Notes - 20200717114457Vignesh C100% (1)

- Cost of Capital Lecture Slides in PDF FormatDokumen18 halamanCost of Capital Lecture Slides in PDF FormatLucy UnBelum ada peringkat

- Portfolio ManagementDokumen40 halamanPortfolio ManagementSayaliRewaleBelum ada peringkat

- Workbook On Derivatives PDFDokumen84 halamanWorkbook On Derivatives PDFsapnaofsnehBelum ada peringkat

- Balanced Scorecard and Benchmarking StrategiesDokumen12 halamanBalanced Scorecard and Benchmarking StrategiesGaurav Sharma100% (1)

- Islamic Banking in Pakistan: Past, Present and FutureDokumen27 halamanIslamic Banking in Pakistan: Past, Present and FutureafeeraBelum ada peringkat

- Chapter 7Dokumen5 halamanChapter 7Saleemah Msskinnyfiber0% (1)

- Chapter - 5 Long Term FinancingDokumen6 halamanChapter - 5 Long Term FinancingmuzgunniBelum ada peringkat

- Cost of CapitalDokumen23 halamanCost of CapitalAsad AliBelum ada peringkat

- Cost of Capital NotesDokumen9 halamanCost of Capital NotesSoumendra RoyBelum ada peringkat

- Cost of Capital ExplainedDokumen18 halamanCost of Capital ExplainedzewdieBelum ada peringkat

- Learning Curves and ApplicationsDokumen10 halamanLearning Curves and ApplicationsDarshan N GangolliBelum ada peringkat

- Chapter 2Dokumen16 halamanChapter 2Ismael SamsonBelum ada peringkat

- Approaches in Portfolio ConstructionDokumen2 halamanApproaches in Portfolio Constructionnayakrajesh89Belum ada peringkat

- Calculating IRR Through Fake Payback Period MethodDokumen9 halamanCalculating IRR Through Fake Payback Period Methodakshit_vij0% (1)

- Chapter 3 Valuation and Cost of CapitalDokumen92 halamanChapter 3 Valuation and Cost of Capitalyemisrach fikiruBelum ada peringkat

- Intro To Leasing NoteDokumen5 halamanIntro To Leasing NoteZain FaheemBelum ada peringkat

- Security Analysis: Chapter - 1Dokumen47 halamanSecurity Analysis: Chapter - 1Harsh GuptaBelum ada peringkat

- Auditing: Lecture # 7Dokumen3 halamanAuditing: Lecture # 7siddiqueicmaBelum ada peringkat

- Corporate governance practices in BangladeshDokumen5 halamanCorporate governance practices in BangladeshTahmina AfrozBelum ada peringkat

- An Overview of Financial ManagementDokumen28 halamanAn Overview of Financial Managementrprems6Belum ada peringkat

- 5 - Bond and Stock Valuation (Compatibility Mode)Dokumen58 halaman5 - Bond and Stock Valuation (Compatibility Mode)Ái Mỹ DuyênBelum ada peringkat

- Bond ValuationDokumen58 halamanBond Valuationpassinet100% (1)

- CH 4Dokumen23 halamanCH 4Gizaw BelayBelum ada peringkat

- Understanding Bond Valuation and Key ConceptsDokumen59 halamanUnderstanding Bond Valuation and Key ConceptsHawraa AlabbasBelum ada peringkat

- The Effect of Working Capital Management On The Manufacturing Firms' ProfitabilityDokumen20 halamanThe Effect of Working Capital Management On The Manufacturing Firms' ProfitabilityAbdii DhufeeraBelum ada peringkat

- Assessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Dokumen25 halamanAssessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Abdii Dhufeera50% (2)

- Effects of CG on Manufacturing Firms' PerformanceDokumen22 halamanEffects of CG on Manufacturing Firms' PerformanceAbdii DhufeeraBelum ada peringkat

- Effects of Corporate Governance Practices On Financial Performance of Manufacturing Sharecompanies in AdamaDokumen17 halamanEffects of Corporate Governance Practices On Financial Performance of Manufacturing Sharecompanies in AdamaAbdii DhufeeraBelum ada peringkat

- Factors Influencing The Adoption of Mobile Banking Service"Dokumen42 halamanFactors Influencing The Adoption of Mobile Banking Service"Abdii Dhufeera100% (1)

- Performance Analysis of Microfinance Institution and Its Sustainability and Outreach (Case Study in Huruta Town, Oromia, Ethiopia)Dokumen19 halamanPerformance Analysis of Microfinance Institution and Its Sustainability and Outreach (Case Study in Huruta Town, Oromia, Ethiopia)Abdii DhufeeraBelum ada peringkat

- Assessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Dokumen25 halamanAssessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Abdii Dhufeera50% (2)

- Factors Influencing The Adoption of Mobile Banking Service"Dokumen42 halamanFactors Influencing The Adoption of Mobile Banking Service"Abdii Dhufeera100% (1)

- Factors Influencing The Adoption of Mobile Banking Service"Dokumen42 halamanFactors Influencing The Adoption of Mobile Banking Service"Abdii Dhufeera100% (1)

- Jiksa 1Dokumen34 halamanJiksa 1Abdii DhufeeraBelum ada peringkat

- Assessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Dokumen25 halamanAssessment of Credit Management Practice of Dashen Bank S.C in Ethiopia (In The Case of Adama District)Abdii Dhufeera50% (2)

- (Case Study Boset Woreda Finance Office) : Adama, EthiopiaDokumen28 halaman(Case Study Boset Woreda Finance Office) : Adama, EthiopiaAbdii DhufeeraBelum ada peringkat

- Cost Accounting II Syllabus and UnitsDokumen1 halamanCost Accounting II Syllabus and UnitsAbdii DhufeeraBelum ada peringkat

- Performance Analysis of Microfinance Institution and Its Sustainability and Outreach (Case Study in Huruta Town, Oromia, Ethiopia)Dokumen23 halamanPerformance Analysis of Microfinance Institution and Its Sustainability and Outreach (Case Study in Huruta Town, Oromia, Ethiopia)Abdii DhufeeraBelum ada peringkat

- Jiksa Ayana Proposal 2Dokumen35 halamanJiksa Ayana Proposal 2Abdii DhufeeraBelum ada peringkat

- File1688 PDFDokumen26 halamanFile1688 PDFShahab UdinBelum ada peringkat

- Credit Risk Management On Ethiopian Commercial Banks": Case of Selected Commercial Banks in Adama TownDokumen36 halamanCredit Risk Management On Ethiopian Commercial Banks": Case of Selected Commercial Banks in Adama TownAbdii Dhufeera100% (2)

- TaxationDokumen56 halamanTaxationAbdii DhufeeraBelum ada peringkat

- Tax Assessment and Collection Challenges in Lode Hetosa District: Arsi, Oromia, Ethiopia Evidence From Category "B'' Tax-PayersDokumen22 halamanTax Assessment and Collection Challenges in Lode Hetosa District: Arsi, Oromia, Ethiopia Evidence From Category "B'' Tax-PayersAbdii Dhufeera100% (3)

- Herambe University Faculty of Business and Economics Department of Mba - ProgramDokumen34 halamanHerambe University Faculty of Business and Economics Department of Mba - ProgramAbdii Dhufeera100% (2)

- Budgeting Basics for BeginnersDokumen29 halamanBudgeting Basics for BeginnersAbdii DhufeeraBelum ada peringkat

- Unit 3Dokumen34 halamanUnit 3Abdii DhufeeraBelum ada peringkat

- Unit 4Dokumen27 halamanUnit 4Abdii DhufeeraBelum ada peringkat

- Unit 2Dokumen34 halamanUnit 2Abdii DhufeeraBelum ada peringkat

- Worksheet For Cost Accounting11Dokumen3 halamanWorksheet For Cost Accounting11Abdii Dhufeera100% (1)

- Table of ContentsDokumen1 halamanTable of ContentsAbdii DhufeeraBelum ada peringkat

- Accounting For ManagersDokumen286 halamanAccounting For ManagersSatyam Rastogi100% (1)

- Budgeting Basics for BeginnersDokumen29 halamanBudgeting Basics for BeginnersAbdii DhufeeraBelum ada peringkat

- Analysis of The Contributionof Vat For Economic Development and Social Spending in EthiopiaDokumen108 halamanAnalysis of The Contributionof Vat For Economic Development and Social Spending in EthiopiaAbdii DhufeeraBelum ada peringkat

- Analysis of The Contributionof Vat For Economic Development and Social Spending in EthiopiaDokumen108 halamanAnalysis of The Contributionof Vat For Economic Development and Social Spending in EthiopiaAbdii DhufeeraBelum ada peringkat

- Gutierrez Corporation’s department A should sell component C to department B at P96 per unitDokumen4 halamanGutierrez Corporation’s department A should sell component C to department B at P96 per unitRoseann KimBelum ada peringkat

- OHS Monthly Report - C.O.T MARCHDokumen6 halamanOHS Monthly Report - C.O.T MARCHvicBelum ada peringkat

- Market Factor That Affect PriceDokumen18 halamanMarket Factor That Affect PriceMazharul KarimBelum ada peringkat

- Segmentacija, Targetiranje, PozicioniranjeDokumen14 halamanSegmentacija, Targetiranje, Pozicioniranjecarina1983Belum ada peringkat

- Case RecruitingDokumen2 halamanCase RecruitingSalsabilaBelum ada peringkat

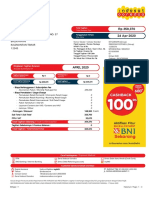

- RP 359,370 24 Apr 2020: Merlin Rahnawaty Kel. Batu Ampar Kalimantan Timur 12345 Perum Ramayana Gg. Rahayu No. 57Dokumen3 halamanRP 359,370 24 Apr 2020: Merlin Rahnawaty Kel. Batu Ampar Kalimantan Timur 12345 Perum Ramayana Gg. Rahayu No. 57Muhammad ardanBelum ada peringkat

- ch03 Comparative International Financial Accounting IDokumen14 halamanch03 Comparative International Financial Accounting INadiaBelum ada peringkat

- Group 4Dokumen9 halamanGroup 4Nurul AinBelum ada peringkat

- Australia Personal Care and Cosmetics Country Guide FINAL PDFDokumen10 halamanAustralia Personal Care and Cosmetics Country Guide FINAL PDFCharmaine GabrielBelum ada peringkat

- ParCor NotesDokumen12 halamanParCor NotesMerrie Rainelle Delos ReyesBelum ada peringkat

- Zoom: An Analysis in Covid PandemicDokumen2 halamanZoom: An Analysis in Covid PandemicPoda PattiBelum ada peringkat

- Decoding Digital Transformation in Construction VF PDFDokumen7 halamanDecoding Digital Transformation in Construction VF PDFArgon UsmanBelum ada peringkat

- Digital Marketing Strategy and Marketing MixDokumen39 halamanDigital Marketing Strategy and Marketing MixAmisha LalBelum ada peringkat

- Systems IntegrationDokumen76 halamanSystems IntegrationChaim Taylor100% (1)

- Maxicare v. CIRDokumen11 halamanMaxicare v. CIRHazel SegoviaBelum ada peringkat

- CAF Azure Partner Day v1.0Dokumen44 halamanCAF Azure Partner Day v1.0estudio estudioBelum ada peringkat

- Chapter-10 C-Quality of Work LifeDokumen17 halamanChapter-10 C-Quality of Work LifeJoginder GrewalBelum ada peringkat

- 6.debt Market and Forex Market-TheoriticalDokumen27 halaman6.debt Market and Forex Market-TheoriticaljashuramuBelum ada peringkat

- ManagementDokumen12 halamanManagementFatima Batool0% (1)

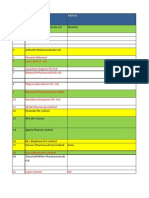

- Mumbai Pharma CompanyDokumen8 halamanMumbai Pharma CompanyPankaj BaghBelum ada peringkat

- 2011 Toyota RAV 4Dokumen1 halaman2011 Toyota RAV 4michaeledem_royalBelum ada peringkat

- Chapter 6 Audit Planning Understanding The Client and AsseDokumen44 halamanChapter 6 Audit Planning Understanding The Client and Asseindra83100% (1)

- Arrow Electronics Case Study on Distribution Partnership with Express PartsDokumen25 halamanArrow Electronics Case Study on Distribution Partnership with Express PartsMuskan Soni75% (4)

- Cultural Times: The First Global Map of Cultural and Creative IndustriesDokumen120 halamanCultural Times: The First Global Map of Cultural and Creative IndustriesFacundo AlvarezBelum ada peringkat

- Business ReportDokumen17 halamanBusiness ReportHazem ElseifyBelum ada peringkat

- Amazon Pathways Interview QuestionsDokumen8 halamanAmazon Pathways Interview Questionssitanshu guptaBelum ada peringkat

- International Trade TheoriesDokumen10 halamanInternational Trade TheoriesAntonio MoralesBelum ada peringkat

- Nike FootwearDokumen8 halamanNike FootwearMaruthi TechnologiesBelum ada peringkat

- SAP MM Interview Questions and Answers For Freshers - Experienced - Top Companies - MNC Job FAQ - STechiesDokumen6 halamanSAP MM Interview Questions and Answers For Freshers - Experienced - Top Companies - MNC Job FAQ - STechiesManas Kumar SahooBelum ada peringkat

- Thomson Reuters Top 100 Global Tech Leaders ReportDokumen20 halamanThomson Reuters Top 100 Global Tech Leaders ReportEric DesportesBelum ada peringkat