Anda mungkin juga menyukai

- A Delectable Tale of Odishas Architectural JourneyDokumen4 halamanA Delectable Tale of Odishas Architectural JourneySudhansuSekharBelum ada peringkat

- Canara Robeco Mutual Fund Additional Purchase Switch Redemption Systematic Transfer Plan Systematic Withdrawal Plan SIP Registration Application FormDokumen2 halamanCanara Robeco Mutual Fund Additional Purchase Switch Redemption Systematic Transfer Plan Systematic Withdrawal Plan SIP Registration Application FormSudhansuSekharBelum ada peringkat

- Retailing Management NewsletterDokumen14 halamanRetailing Management NewsletterSudhansuSekharBelum ada peringkat

- CLRMDokumen28 halamanCLRMSudhansuSekharBelum ada peringkat

- Regression With Panel DataDokumen16 halamanRegression With Panel DataSudhansuSekharBelum ada peringkat

- WWST Side StoryDokumen38 halamanWWST Side StorySudhansuSekharBelum ada peringkat

- IT Strategy For XIMB (XUB) : Group 11Dokumen24 halamanIT Strategy For XIMB (XUB) : Group 11SudhansuSekharBelum ada peringkat

- Cloud PDFDokumen2 halamanCloud PDFSudhansuSekharBelum ada peringkat

- It SdiDokumen16 halamanIt SdiSudhansuSekharBelum ada peringkat

- Implementing The ERP Solutions in Arvind MillsDokumen18 halamanImplementing The ERP Solutions in Arvind MillsSudhansuSekharBelum ada peringkat

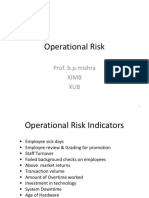

- Operational Risk: Prof. B.p.mishra Ximb XUBDokumen37 halamanOperational Risk: Prof. B.p.mishra Ximb XUBSudhansuSekharBelum ada peringkat

- NotesDokumen22 halamanNotesSudhansuSekharBelum ada peringkat

- Banking in Other CountriesDokumen37 halamanBanking in Other CountriesSudhansuSekharBelum ada peringkat

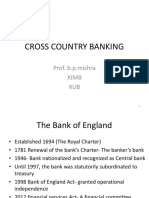

- Cross Country Banking: Prof. B.p.mishra Ximb XUBDokumen49 halamanCross Country Banking: Prof. B.p.mishra Ximb XUBSudhansuSekharBelum ada peringkat

- Loan PricingDokumen57 halamanLoan PricingSudhansuSekharBelum ada peringkat

- Exposure NormsDokumen30 halamanExposure NormsSudhansuSekharBelum ada peringkat

- Profit & Loss: Prof.b.p.mshra XimbDokumen28 halamanProfit & Loss: Prof.b.p.mshra XimbSudhansuSekharBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Share Khan Share ManualDokumen358 halamanShare Khan Share Manualkushal1985Belum ada peringkat

- EVCA Reporting GuidelinesDokumen39 halamanEVCA Reporting GuidelinesZaphod BeeblebroxBelum ada peringkat

- 05 Fisher Account 5e v1 PPT ch05Dokumen60 halaman05 Fisher Account 5e v1 PPT ch05yuqi liuBelum ada peringkat

- Relative ValuationDokumen90 halamanRelative ValuationParvesh AghiBelum ada peringkat

- Chapter 6 Intangible AssetsDokumen28 halamanChapter 6 Intangible Assetsswarna dasBelum ada peringkat

- Innovation PortfoliosDokumen13 halamanInnovation PortfoliosMichael Kaufman100% (1)

- Which of The Following Statements Are CorrectDokumen18 halamanWhich of The Following Statements Are CorrectkaktosjaazBelum ada peringkat

- Sam Unreval: Quantity Survey, Estimation An ValuationDokumen152 halamanSam Unreval: Quantity Survey, Estimation An ValuationRahul Gupta0% (1)

- Full Download Derivatives Markets 3rd Edition Ebook PDFDokumen41 halamanFull Download Derivatives Markets 3rd Edition Ebook PDFmary.abernathy960100% (39)

- Partnership AccountsDokumen4 halamanPartnership AccountsnathanrengaBelum ada peringkat

- Test Bank For International Accounting 4Th Edition Doupnik Perera 0077862201 9780077862206 Full Chapter PDFDokumen36 halamanTest Bank For International Accounting 4Th Edition Doupnik Perera 0077862201 9780077862206 Full Chapter PDFryan.boyd506100% (12)

- Valuation Workbook QuestionsDokumen200 halamanValuation Workbook Questionsprafulvg100% (1)

- Empire East: Q2/H1 Financial StatementDokumen34 halamanEmpire East: Q2/H1 Financial StatementBusinessWorldBelum ada peringkat

- AC305 SAP Key NotesDokumen48 halamanAC305 SAP Key NotesJamesYacoBelum ada peringkat

- HBS Introduction To Bonds and Bond Math 5170-PDF-ENG (1) (01-30) (16-30)Dokumen15 halamanHBS Introduction To Bonds and Bond Math 5170-PDF-ENG (1) (01-30) (16-30)LorennarBelum ada peringkat

- Final Report - Wal-MartDokumen20 halamanFinal Report - Wal-MartaliBelum ada peringkat

- FIN201 CF T3 2021 BBUS Unit Guide V2 07092021Dokumen11 halamanFIN201 CF T3 2021 BBUS Unit Guide V2 07092021Nguyen Quynh AnhBelum ada peringkat

- Economics of Strategy 6th Edition Besanko Test BankDokumen9 halamanEconomics of Strategy 6th Edition Besanko Test Banka726606156Belum ada peringkat

- UGBA 131 Syllabus Spring 2016Dokumen6 halamanUGBA 131 Syllabus Spring 2016Rushil SurapaneniBelum ada peringkat

- Technical Analysis TutorialDokumen34 halamanTechnical Analysis TutorialFahimBelum ada peringkat

- CaseDokumen68 halamanCaseDharini Raje SisodiaBelum ada peringkat

- PWC Loyalty Analytics ExposedDokumen13 halamanPWC Loyalty Analytics ExposedUmang GuptaBelum ada peringkat

- Valuation Q&A McKinseyDokumen4 halamanValuation Q&A McKinseyZi Sheng NeohBelum ada peringkat

- Blackrock Sample Financial ReportingDokumen497 halamanBlackrock Sample Financial Reportingduc anhBelum ada peringkat

- AFAR Notes by Dr. FerrerDokumen21 halamanAFAR Notes by Dr. FerrerAko C Marz100% (1)

- Principles of Managerial Finance Chapters 1Dokumen50 halamanPrinciples of Managerial Finance Chapters 1sacey20.hbBelum ada peringkat

- Bloomberg Assignment Example 2Dokumen16 halamanBloomberg Assignment Example 2Babes WadieBelum ada peringkat

- Corporate Finance CheatsheetDokumen4 halamanCorporate Finance CheatsheetLynetteBelum ada peringkat

- Chapter 20Dokumen19 halamanChapter 20Leen AlnussayanBelum ada peringkat

- MFC Corporate Brochure 2013-14Dokumen56 halamanMFC Corporate Brochure 2013-14Harshavardhan TummaBelum ada peringkat