Anda mungkin juga menyukai

- 162 005Dokumen1 halaman162 005Angelli LamiqueBelum ada peringkat

- Report of The Technical Group On Money Market: Reserve Bank of India May 2005Dokumen29 halamanReport of The Technical Group On Money Market: Reserve Bank of India May 2005api-27174321Belum ada peringkat

- P4 Chapter 04 Risk Adjusted WACC and Adjusted Present Value PDFDokumen45 halamanP4 Chapter 04 Risk Adjusted WACC and Adjusted Present Value PDFasim tariqBelum ada peringkat

- Professional Ethics - , Accountancy For Lawyers and Bench-BarDokumen27 halamanProfessional Ethics - , Accountancy For Lawyers and Bench-BarArpan Kamal100% (6)

- Statement of Account: No 15 Jalan Awana 12 Taman Cheras Awana 43200 Batu 9 Cheras, SelangorDokumen5 halamanStatement of Account: No 15 Jalan Awana 12 Taman Cheras Awana 43200 Batu 9 Cheras, Selangorputri nurishaBelum ada peringkat

- Oracle Database 11g OverviewDokumen46 halamanOracle Database 11g OverviewEddie Awad91% (11)

- Inv NDokumen124 halamanInv NharyhunterBelum ada peringkat

- J.C. Parets, CMTDokumen25 halamanJ.C. Parets, CMTPunit TewaniBelum ada peringkat

- FMG China Fund - PresentationDokumen15 halamanFMG China Fund - PresentationSusan AllenBelum ada peringkat

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Dokumen71 halaman"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkBelum ada peringkat

- Get The Power of Equity and Debt With Sbi Dual Advantage Fund - Series XxiiDokumen4 halamanGet The Power of Equity and Debt With Sbi Dual Advantage Fund - Series Xxiiarghya000Belum ada peringkat

- Why Choose The IASDokumen6 halamanWhy Choose The IASPeter UrbaniBelum ada peringkat

- Netra Early Warnings Signals Through Charts Oct 2022Dokumen20 halamanNetra Early Warnings Signals Through Charts Oct 2022kishore13Belum ada peringkat

- Update On IDFC Arbitrage FundDokumen6 halamanUpdate On IDFC Arbitrage FundGBelum ada peringkat

- Part 2.4 InvestmentDokumen8 halamanPart 2.4 InvestmentSara MohamedBelum ada peringkat

- November 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?Dokumen8 halamanNovember 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?RobertMcCulloughBelum ada peringkat

- Presentation To Macquarie Corporate Day in Singapore & Hong KongDokumen54 halamanPresentation To Macquarie Corporate Day in Singapore & Hong KongnigelburkeBelum ada peringkat

- Southeast Texas Labor StatisticsDokumen1 halamanSoutheast Texas Labor StatisticsCharlie FoxworthBelum ada peringkat

- Derivatives in IndiaDokumen21 halamanDerivatives in IndiaShajupaulBelum ada peringkat

- SSRN Id2337709Dokumen13 halamanSSRN Id2337709Anonymous pb0lJ4n5jBelum ada peringkat

- Innovation and The Financial CrisisDokumen20 halamanInnovation and The Financial Crisisttunguz100% (3)

- Gerald CorcoranDokumen9 halamanGerald CorcoranMarketsWikiBelum ada peringkat

- Gmo - For Whom The Bond TollsDokumen8 halamanGmo - For Whom The Bond Tollsfreemind3682Belum ada peringkat

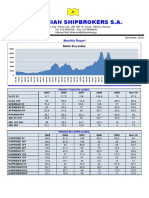

- athenian-shipbrokers-NOV 2010Dokumen17 halamanathenian-shipbrokers-NOV 2010Nguyen Le Thu HaBelum ada peringkat

- in Our View,: Vrddhi Capital Investment AdvisorsDokumen5 halamanin Our View,: Vrddhi Capital Investment AdvisorsMohit AgarwalBelum ada peringkat

- HDFC Mutual FundDokumen25 halamanHDFC Mutual Fundapi-25886395Belum ada peringkat

- Baltimore Metropolitan Area: Market ReportDokumen21 halamanBaltimore Metropolitan Area: Market ReportAnonymous Feglbx5Belum ada peringkat

- Ideas & InsightsDokumen2 halamanIdeas & Insightsag rBelum ada peringkat

- Spotlight 2006-10 3 enDokumen3 halamanSpotlight 2006-10 3 enarunkn01Belum ada peringkat

- HCMF Investor Letter October 2009 FINALDokumen24 halamanHCMF Investor Letter October 2009 FINALAbsolute Return100% (1)

- Research Speak - 16-04-2010Dokumen12 halamanResearch Speak - 16-04-2010A_KinshukBelum ada peringkat

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDokumen16 halamanGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaBelum ada peringkat

- Accommodation Supply Analysis in Launceston Part 1Dokumen34 halamanAccommodation Supply Analysis in Launceston Part 1The ExaminerBelum ada peringkat

- MEF Analysis UI Claims - March 2020Dokumen2 halamanMEF Analysis UI Claims - March 2020Dave AllenBelum ada peringkat

- By David Harding and Georgia Nakou, Winton Capital ManagementDokumen5 halamanBy David Harding and Georgia Nakou, Winton Capital ManagementCoco BungbingBelum ada peringkat

- Baltics RevisitedDokumen12 halamanBaltics RevisitedideanoiseBelum ada peringkat

- SSRNDokumen7 halamanSSRNjoystocks777Belum ada peringkat

- What Is Really Killing The Irish EconomyDokumen1 halamanWhat Is Really Killing The Irish EconomyLuis Riestra Delgado100% (1)

- CME - Comparing E-Minis and ETFs - Sep2012 PDFDokumen8 halamanCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqBelum ada peringkat

- South Korean Energy Outlook 2015Dokumen13 halamanSouth Korean Energy Outlook 2015Afifa KamilaBelum ada peringkat

- September 2010Dokumen1 halamanSeptember 2010Stephanie Miller HofmanBelum ada peringkat

- .Phexportsitesprudential PH - galleriesPDFPru Life UK December 2019 PDFDokumen24 halaman.Phexportsitesprudential PH - galleriesPDFPru Life UK December 2019 PDFHarold Q. GardonBelum ada peringkat

- Module III: Derivatives: Chapter 5: Interest Rate Futures ContractDokumen27 halamanModule III: Derivatives: Chapter 5: Interest Rate Futures Contractsantucan1Belum ada peringkat

- Growth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Dokumen15 halamanGrowth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Ricardo GutierrezBelum ada peringkat

- Shipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Dokumen22 halamanShipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Luis Enrique LavayenBelum ada peringkat

- Correlation and Diversification 1Dokumen3 halamanCorrelation and Diversification 1Poonam BathijaBelum ada peringkat

- Lecture 1 2019Dokumen58 halamanLecture 1 2019yitong zhangBelum ada peringkat

- Equity Debt Strategy For Mar20Dokumen25 halamanEquity Debt Strategy For Mar20Saad KhanBelum ada peringkat

- Florida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoDokumen16 halamanFlorida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenBelum ada peringkat

- (Buzzmetrics) BuzzSpeak - Preparations For Tet 2022Dokumen20 halaman(Buzzmetrics) BuzzSpeak - Preparations For Tet 2022Tố Đoan Lê NgọcBelum ada peringkat

- Beaumont Port Arthur Labor StatisticsDokumen1 halamanBeaumont Port Arthur Labor StatisticsCharlie FoxworthBelum ada peringkat

- CH 7 Diminishing MusharakaDokumen32 halamanCH 7 Diminishing Musharakasaadullah98.sk.skBelum ada peringkat

- Florida's November Employment Figures ReleasedDokumen16 halamanFlorida's November Employment Figures ReleasedMichael AllenBelum ada peringkat

- HLA Venture Income Fund Apr 22Dokumen3 halamanHLA Venture Income Fund Apr 22ivyBelum ada peringkat

- Florida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoDokumen16 halamanFlorida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenBelum ada peringkat

- NTDOP One Pager Jun'22Dokumen3 halamanNTDOP One Pager Jun'22Deepak GoyalBelum ada peringkat

- Athenian-Shipbrokers-March 2013Dokumen19 halamanAthenian-Shipbrokers-March 2013Nguyen Le Thu HaBelum ada peringkat

- 2007 GPS Pricing Trends ReportDokumen3 halaman2007 GPS Pricing Trends Reportlili_pumaBelum ada peringkat

- Should My Asset Allocation Include My Pension and Social Security?Dari EverandShould My Asset Allocation Include My Pension and Social Security?Belum ada peringkat

- JBT's Filling & Sterilization Technology For Baby Food in Glass JarsDokumen11 halamanJBT's Filling & Sterilization Technology For Baby Food in Glass Jarsyadavmihir63Belum ada peringkat

- Estimating Discount Rates: DCF ValuationDokumen60 halamanEstimating Discount Rates: DCF Valuationyadavmihir63Belum ada peringkat

- FAQs - World Instant Noodles Association Desribe - 1234Dokumen5 halamanFAQs - World Instant Noodles Association Desribe - 1234yadavmihir63Belum ada peringkat

- Cash Credit SystemDokumen6 halamanCash Credit Systemyadavmihir63Belum ada peringkat

- Overview of Mutual FundsDokumen28 halamanOverview of Mutual Fundsyadavmihir63Belum ada peringkat

- Raw Milk From Silo To Feed Balance Tank 1500-3016-PP01: Pump Application: Pump Tag NoDokumen1 halamanRaw Milk From Silo To Feed Balance Tank 1500-3016-PP01: Pump Application: Pump Tag Noyadavmihir63Belum ada peringkat

- Finotex ChemcialDokumen43 halamanFinotex Chemcialyadavmihir63Belum ada peringkat

- Collective Investment Vehicle Formed With The Specific Objective of Raising Money From Large Number of IndividualsDokumen120 halamanCollective Investment Vehicle Formed With The Specific Objective of Raising Money From Large Number of Individualsyadavmihir63Belum ada peringkat

- SPMAT EffectiveMaterialsManagement WhitePaperDokumen12 halamanSPMAT EffectiveMaterialsManagement WhitePaperyadavmihir63Belum ada peringkat

- Originate Industries ProfileDokumen4 halamanOriginate Industries Profileyadavmihir63Belum ada peringkat

- Diaphragm Pump NOVADOS - H3Dokumen2 halamanDiaphragm Pump NOVADOS - H3yadavmihir63Belum ada peringkat

- Swedbank: A Corporate PresentationDokumen32 halamanSwedbank: A Corporate PresentationmeluojuBelum ada peringkat

- L.D BankDokumen33 halamanL.D BankSuhail88038Belum ada peringkat

- Attendee List As of 4-22-19.Dokumen7 halamanAttendee List As of 4-22-19.karthik83.v209Belum ada peringkat

- Quiz 2 Audtheo PDFDokumen4 halamanQuiz 2 Audtheo PDFCharlen Relos GermanBelum ada peringkat

- Requirement 1 Total Per Unit: Banitog, Brigitte C. BSA 211 Exercise 1 (Contribution Format Income Statement)Dokumen4 halamanRequirement 1 Total Per Unit: Banitog, Brigitte C. BSA 211 Exercise 1 (Contribution Format Income Statement)MyunimintBelum ada peringkat

- Fin Midterm 1 PDFDokumen6 halamanFin Midterm 1 PDFIshan DebnathBelum ada peringkat

- FinalDokumen31 halamanFinalAniruddha RantuBelum ada peringkat

- Tutorial 7 Chapter 6&7Dokumen2 halamanTutorial 7 Chapter 6&7Renee WongBelum ada peringkat

- Survey and Thought of Financial Management and EduDokumen4 halamanSurvey and Thought of Financial Management and EduDENMARKBelum ada peringkat

- Financial Statement ANALYSIS 2014-2015: ObjectiveDokumen15 halamanFinancial Statement ANALYSIS 2014-2015: ObjectiveMahmoud ZizoBelum ada peringkat

- Abba Application FormDokumen1 halamanAbba Application FormAbbaBelum ada peringkat

- Finance and Accounts - Business Management IBDokumen6 halamanFinance and Accounts - Business Management IBJUNIORBelum ada peringkat

- Chapter 15Dokumen117 halamanChapter 15Karla Selman100% (1)

- CFAS.100 - Diagnostic Test Part 1Dokumen4 halamanCFAS.100 - Diagnostic Test Part 1Mika MolinaBelum ada peringkat

- Risk Management in ONGCDokumen9 halamanRisk Management in ONGCAdithya BangaloreBelum ada peringkat

- Buyback Letter of OfferDokumen3 halamanBuyback Letter of OfferNarBelum ada peringkat

- A.Income Statement: Pre-Operation Year 1Dokumen5 halamanA.Income Statement: Pre-Operation Year 1Benjie MariBelum ada peringkat

- FIS Treasury and Risk Manager Quantum Edition Product SheetDokumen2 halamanFIS Treasury and Risk Manager Quantum Edition Product SheetMohdBelum ada peringkat

- Delgado - Forex: How To Build Your Trading Watch List.Dokumen13 halamanDelgado - Forex: How To Build Your Trading Watch List.Franklin Delgado VerasBelum ada peringkat

- Change Management@iciciDokumen3 halamanChange Management@icicisanthiya balaraman100% (1)

- Class Notes Redemption of Preference Share - PDFDokumen4 halamanClass Notes Redemption of Preference Share - PDFBhavya MehtaBelum ada peringkat

- Cityam 2010-11-09Dokumen36 halamanCityam 2010-11-09City A.M.Belum ada peringkat

- Solved Cosimo Enterprises Issues A 260 000 45 Day 5 Note To DixonDokumen1 halamanSolved Cosimo Enterprises Issues A 260 000 45 Day 5 Note To DixonAnbu jaromiaBelum ada peringkat

- Evaluation CriteriaDokumen6 halamanEvaluation Criteriabahaman417Belum ada peringkat

- 04.09.2022 - 14.06.1401Dokumen14 halaman04.09.2022 - 14.06.1401Sarajuddin IbrahimzadaBelum ada peringkat

- SKC Consulting Private LimitedDokumen29 halamanSKC Consulting Private LimitedChetan DabasBelum ada peringkat