Anda mungkin juga menyukai

- Concept and Meaning of Property by Roohika SehgalDokumen13 halamanConcept and Meaning of Property by Roohika SehgalRoohika SehgalBelum ada peringkat

- HyposDokumen2 halamanHyposLively Roamer100% (1)

- D Amodaram Sanjivayya National Law University, Visakhapatnam: Project On: - U.P. Land LawsDokumen24 halamanD Amodaram Sanjivayya National Law University, Visakhapatnam: Project On: - U.P. Land LawsHarshit MalviyaBelum ada peringkat

- Ilch M.P Jain Part1 PDFDokumen267 halamanIlch M.P Jain Part1 PDFchirag behlBelum ada peringkat

- Textbook On Transfer of Property Act 6nbsped 2Dokumen700 halamanTextbook On Transfer of Property Act 6nbsped 2Krupa ShanmugamBelum ada peringkat

- Development of Modern International Law and India R.P.anandDokumen77 halamanDevelopment of Modern International Law and India R.P.anandVeeramani ManiBelum ada peringkat

- Land Ceiling Act 1960 PDFDokumen22 halamanLand Ceiling Act 1960 PDFAnirudhBelum ada peringkat

- Indian Federalism: Examining The DebateDokumen8 halamanIndian Federalism: Examining The DebateAmartya Bag100% (1)

- TPADokumen13 halamanTPAYash TiwariBelum ada peringkat

- Condition Restraining EnjoymentDokumen21 halamanCondition Restraining EnjoymentTanushka shuklaBelum ada peringkat

- AKHIL Family CasesDokumen3 halamanAKHIL Family CasesSushrutBelum ada peringkat

- Article 16 (4) and 335Dokumen19 halamanArticle 16 (4) and 335husainBelum ada peringkat

- One Liner Case LawDokumen4 halamanOne Liner Case LawGautamBelum ada peringkat

- No. Amendments Enforced Since Objectives: Amendments To The Constitution of IndiaDokumen8 halamanNo. Amendments Enforced Since Objectives: Amendments To The Constitution of IndiaPrashant SuryawanshiBelum ada peringkat

- List of Applicant Applied in NRI NRI SponsoredDokumen2 halamanList of Applicant Applied in NRI NRI SponsoredAjit JaiswalBelum ada peringkat

- Contract NotesDokumen111 halamanContract NotesRiya RoyBelum ada peringkat

- Indian Legal SystemDokumen20 halamanIndian Legal SystemSAJAD MOHAMMEDBelum ada peringkat

- 036 - Public International Law (171-173)Dokumen3 halaman036 - Public International Law (171-173)durgesh4yadav-140230% (1)

- Adhunik Steels LTD VsDokumen5 halamanAdhunik Steels LTD VsAbhishek Premlata Kumar100% (1)

- 2ndSEM IRACDokumen6 halaman2ndSEM IRACAsham SharmaBelum ada peringkat

- Dissertation On Indian Environmental Laws and Global IssuesDokumen98 halamanDissertation On Indian Environmental Laws and Global IssuesPrashant VarshneyBelum ada peringkat

- Land LawsDokumen14 halamanLand LawsSarthak PageBelum ada peringkat

- Land Acquisition ActDokumen5 halamanLand Acquisition ActsahilkaushikBelum ada peringkat

- Law of SeaDokumen23 halamanLaw of SeaJatin Bakshi100% (1)

- Article 17-18 - Constitution of India - YG Notes - 5937298Dokumen3 halamanArticle 17-18 - Constitution of India - YG Notes - 5937298akhandBelum ada peringkat

- History of Land RevenueDokumen5 halamanHistory of Land RevenueAizaz AlamBelum ada peringkat

- Deeds, Notices and WillsDokumen21 halamanDeeds, Notices and WillsMansukh GargBelum ada peringkat

- File of Land Acquisition Act 1984Dokumen8 halamanFile of Land Acquisition Act 1984Asma Hashmi100% (1)

- Evidentiary Value of FIRDokumen12 halamanEvidentiary Value of FIRSiddharth soniBelum ada peringkat

- State Succession A Critical AnalysisDokumen12 halamanState Succession A Critical AnalysisArpita YadavBelum ada peringkat

- Chapter 2 Hindu Joint FamilyDokumen21 halamanChapter 2 Hindu Joint FamilySAMBIT KUMAR PATRIBelum ada peringkat

- Section 24Dokumen24 halamanSection 24Tanisha SolankiBelum ada peringkat

- 16land Laws Land LawsDokumen203 halaman16land Laws Land Lawsannpurna pathakBelum ada peringkat

- Significance of Formation Process of International Treaty Under International LawDokumen18 halamanSignificance of Formation Process of International Treaty Under International LawmishraavneeshBelum ada peringkat

- Family Law Project 2Dokumen17 halamanFamily Law Project 2Abhisek DashBelum ada peringkat

- Right To PrivacyDokumen6 halamanRight To PrivacyAbhishek KumarBelum ada peringkat

- Contract Course Outline - National Law University OdishaDokumen7 halamanContract Course Outline - National Law University OdishaUtsav DwivediBelum ada peringkat

- Bombay Tenancy and Agricultural Lands Act 1948Dokumen4 halamanBombay Tenancy and Agricultural Lands Act 1948Keith10w0% (1)

- History Superbbb EverythingDokumen18 halamanHistory Superbbb EverythingKistanna GKBelum ada peringkat

- Comparison Between Land Acquisition Act, 1894 and The Right To Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement ACT 2013Dokumen57 halamanComparison Between Land Acquisition Act, 1894 and The Right To Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement ACT 2013Dharminder Kumar100% (1)

- Nature, Origins and Basis of International LawDokumen16 halamanNature, Origins and Basis of International Lawmubzz_Belum ada peringkat

- Law and PovertyDokumen7 halamanLaw and PovertySinghBelum ada peringkat

- Tulk V MoxhayDokumen1 halamanTulk V MoxhayTiffany GrantBelum ada peringkat

- Profit A Prendre - AssignmentDokumen3 halamanProfit A Prendre - AssignmentNavaneeth NeonBelum ada peringkat

- University Institute of Legal Studies: Constitutional Law-IiDokumen19 halamanUniversity Institute of Legal Studies: Constitutional Law-IiJaskaranBelum ada peringkat

- Introductory Page S K K KapoorDokumen33 halamanIntroductory Page S K K KapoorKhadijaSaleem100% (1)

- Doctrine of Harmonious ConstructionDokumen5 halamanDoctrine of Harmonious Constructionjurumento367% (3)

- Civil ProcedureDokumen11 halamanCivil ProcedureGAUTAM BUCHHA100% (1)

- I R CoheloDokumen5 halamanI R CoheloHarsh PathakBelum ada peringkat

- President ElectionDokumen12 halamanPresident Electionsahil khanBelum ada peringkat

- Right To Information RTI Act 2005: Dr. Monika Dubey Faculty, MBA Program Rajasthan Technical University, KotaDokumen31 halamanRight To Information RTI Act 2005: Dr. Monika Dubey Faculty, MBA Program Rajasthan Technical University, Kotamani100% (1)

- Jurisprudence (Personality)Dokumen16 halamanJurisprudence (Personality)Madan JhaBelum ada peringkat

- SUTN Id2322609Dokumen177 halamanSUTN Id2322609Rishabh Goyal0% (1)

- Judicial Views On Conditional Legislation - Effects and Implication-An OverviewDokumen16 halamanJudicial Views On Conditional Legislation - Effects and Implication-An OverviewGaurav AryaBelum ada peringkat

- PREMPTIONDokumen33 halamanPREMPTIONgunjanjha11Belum ada peringkat

- Environmental-Governance-And-Role-Of-Judiciary-In-India Ebook & Lecture Notes PDF Download (Studynama - Com - India's Biggest Website For Law Study Material Downloads)Dokumen209 halamanEnvironmental-Governance-And-Role-Of-Judiciary-In-India Ebook & Lecture Notes PDF Download (Studynama - Com - India's Biggest Website For Law Study Material Downloads)Vinnie SinghBelum ada peringkat

- Case Laws Summary PDFDokumen18 halamanCase Laws Summary PDFvaibhav SharmaBelum ada peringkat

- Petron V NCBADokumen7 halamanPetron V NCBAAdelaide MabalotBelum ada peringkat

- TAÑADA v. TUVERA G.R. No. L-63915 April 24, 1985 PDFDokumen1 halamanTAÑADA v. TUVERA G.R. No. L-63915 April 24, 1985 PDFjmz_13Belum ada peringkat

- Chalos, Peter., Margaret C.C Poon. 2000. Participation and Performance in Capital Budgeting TeamsDokumen31 halamanChalos, Peter., Margaret C.C Poon. 2000. Participation and Performance in Capital Budgeting TeamsSarmanDGrezkoBelum ada peringkat

- 01) Philippine American General Insurance Co v. CA - AcabadoDokumen1 halaman01) Philippine American General Insurance Co v. CA - AcabadoRaymund CallejaBelum ada peringkat

- Court Order Denying Preliminary Injunction To Marcel July Over Octavius TowerDokumen5 halamanCourt Order Denying Preliminary Injunction To Marcel July Over Octavius TowerRyan Gile, Esq.Belum ada peringkat

- Lecture 5-Professional Ethics and Code of ConductDokumen29 halamanLecture 5-Professional Ethics and Code of ConductNatalia NaveedBelum ada peringkat

- Marquez Vs Disierto MATDokumen2 halamanMarquez Vs Disierto MATmarwantahsinBelum ada peringkat

- LoaDokumen1 halamanLoaRavula VenkateshBelum ada peringkat

- Trainee AgreementDokumen2 halamanTrainee AgreementAlexander Buere100% (2)

- Contract-Pet Sitting Agreement 2019Dokumen2 halamanContract-Pet Sitting Agreement 2019api-309526058Belum ada peringkat

- 5 Case Digest Cir Vs Estate of TodaDokumen2 halaman5 Case Digest Cir Vs Estate of TodaChrissy Sabella0% (1)

- Missionary Sisters of Our Lady of Fatima v. AlzonaDokumen4 halamanMissionary Sisters of Our Lady of Fatima v. AlzonaEcob ResurreccionBelum ada peringkat

- Simple MortgageDokumen10 halamanSimple MortgagesubramonianBelum ada peringkat

- NEGO Week 5 (July 5 and 6)Dokumen3 halamanNEGO Week 5 (July 5 and 6)larcia025Belum ada peringkat

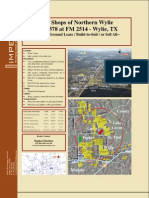

- Shops of Northern Wylie (Imperium Holdings)Dokumen3 halamanShops of Northern Wylie (Imperium Holdings)Imperium Holdings, LPBelum ada peringkat

- Agency and PartnershipDokumen164 halamanAgency and PartnershipDayday AbleBelum ada peringkat

- Bellis Vs BellisDokumen2 halamanBellis Vs BellisJulianne Ruth TanBelum ada peringkat

- Precedential: Circuit JudgesDokumen44 halamanPrecedential: Circuit JudgesScribd Government DocsBelum ada peringkat

- Alpha Insurance and Surety Co. Vs CastorDokumen2 halamanAlpha Insurance and Surety Co. Vs Castorabc defBelum ada peringkat

- Procedure For Investigation of Combinations - Competition Act - 2002 - Bare Acts - Law Library - AdvocateKhojDokumen1 halamanProcedure For Investigation of Combinations - Competition Act - 2002 - Bare Acts - Law Library - AdvocateKhojMishika PanditaBelum ada peringkat

- Superintending Engineer/Civil, Corporate Office, TSSPDCL, Mint Compound, HyderabadDokumen2 halamanSuperintending Engineer/Civil, Corporate Office, TSSPDCL, Mint Compound, HyderabadVikram Aditya ReddyBelum ada peringkat

- Substantive Vs Procedural LawDokumen2 halamanSubstantive Vs Procedural LawJade Manguera100% (1)

- Sample Memorandum of AgreementDokumen3 halamanSample Memorandum of AgreementCollinBelum ada peringkat

- Write A Pleading and Its Defense in A Civil SuitDokumen7 halamanWrite A Pleading and Its Defense in A Civil SuitAnonymous dLIq7U3DKz100% (7)

- PLM vs. IAC PDFDokumen17 halamanPLM vs. IAC PDFAivan Charles TorresBelum ada peringkat

- AIOTA Student MembershipDokumen4 halamanAIOTA Student MembershipMohit KumarBelum ada peringkat

- 10 BF Homes v. MeralcoDokumen1 halaman10 BF Homes v. MeralcoJill BagaoisanBelum ada peringkat

- Hofer Et Al v. Old Navy Inc. Et Al - Document No. 14Dokumen6 halamanHofer Et Al v. Old Navy Inc. Et Al - Document No. 14Justia.comBelum ada peringkat

- Powers Home EvictionDokumen12 halamanPowers Home EvictionGlen HellmanBelum ada peringkat

- Hold Harmless Form - Dallas ImpoundDokumen2 halamanHold Harmless Form - Dallas ImpoundTyler BealsBelum ada peringkat