Anda mungkin juga menyukai

- Effective Leadership Skills in The 21ST CenturyDokumen67 halamanEffective Leadership Skills in The 21ST CenturySam ONi100% (1)

- Yellow King - Black Star MagicDokumen186 halamanYellow King - Black Star Magicwijeesf797100% (1)

- Nation of Islam Timeline and Fact Sheet (Brief)Dokumen6 halamanNation of Islam Timeline and Fact Sheet (Brief)salaamwestnBelum ada peringkat

- SAMPLE Information On RapeDokumen2 halamanSAMPLE Information On RapeMay May100% (2)

- Ballotpedia Writing Style Guide (Spring 2016)Dokumen54 halamanBallotpedia Writing Style Guide (Spring 2016)Ballotpedia67% (3)

- Henry Kissinger On The Establishment of A New World Order PDFDokumen4 halamanHenry Kissinger On The Establishment of A New World Order PDFGoran Djokic100% (1)

- Business Writing GuideDokumen22 halamanBusiness Writing GuideNene Taps100% (1)

- Philippine Budget CycleDokumen67 halamanPhilippine Budget CycleJessa Dela CruzBelum ada peringkat

- Jcpoa Infograph 020218Dokumen1 halamanJcpoa Infograph 020218The Iran ProjectBelum ada peringkat

- The Marcos DynastyDokumen19 halamanThe Marcos DynastyRyan AntipordaBelum ada peringkat

- Doctor Prescription PadDokumen1 halamanDoctor Prescription PadDOH RO X RLEDBelum ada peringkat

- Maximizing LGPMS Data Reports for LGU OperationsDokumen13 halamanMaximizing LGPMS Data Reports for LGU OperationsRonz RoganBelum ada peringkat

- To The Women of MalolosDokumen21 halamanTo The Women of MalolosNamoc, LeninBelum ada peringkat

- Gender and Social Policy in A Global Context: Shahra Razavi and Shireen HassimDokumen367 halamanGender and Social Policy in A Global Context: Shahra Razavi and Shireen HassimMauro KnovaBelum ada peringkat

- Phases in The Evolution of Public AdministrationDokumen104 halamanPhases in The Evolution of Public Administrationaubrey rodriguezBelum ada peringkat

- China's Political and Economical Reforms: Lessons and LimitationsDokumen24 halamanChina's Political and Economical Reforms: Lessons and LimitationsTavian HunterBelum ada peringkat

- Business Writing For Soon-To-Be Professionals: Presented By: Algene Malte de Guzman, CPHDDokumen17 halamanBusiness Writing For Soon-To-Be Professionals: Presented By: Algene Malte de Guzman, CPHDamdeguzmanBelum ada peringkat

- 3+Minute+Sales+Multiplier - PDF Jho Benson TopppDokumen6 halaman3+Minute+Sales+Multiplier - PDF Jho Benson TopppAndressa Nunes BatistaBelum ada peringkat

- Affidavit of Discrepancy in GenderDokumen2 halamanAffidavit of Discrepancy in GenderrogerBelum ada peringkat

- Functions of International OrganizationsDokumen31 halamanFunctions of International OrganizationsJonas Anciano100% (1)

- Diplomacy .1Dokumen19 halamanDiplomacy .1Sadia SaeedBelum ada peringkat

- Foreign Policy Analysis 2Dokumen8 halamanForeign Policy Analysis 2Arya Filoza PermadiBelum ada peringkat

- Cocept of Economic Growth and DevelopmentDokumen11 halamanCocept of Economic Growth and DevelopmentPrerna JhaBelum ada peringkat

- The Philippine Administrative System ModuleDokumen16 halamanThe Philippine Administrative System ModuleCerado AviertoBelum ada peringkat

- Ir PresentationDokumen25 halamanIr Presentationhayat hanimBelum ada peringkat

- Diplomacy's Nature & Wilson's 14 PointsDokumen40 halamanDiplomacy's Nature & Wilson's 14 PointsTrix BermosaBelum ada peringkat

- Intro To Public Administration 1 1Dokumen71 halamanIntro To Public Administration 1 1Bea PaghubasanBelum ada peringkat

- Israel's Economy March 2011Dokumen38 halamanIsrael's Economy March 2011Economic Mission, Embassy of IsraelBelum ada peringkat

- Immediate Flood Report Final Hurricane Harvey 2017Dokumen32 halamanImmediate Flood Report Final Hurricane Harvey 2017KHOU100% (1)

- CyberDokumen29 halamanCyberBhanubhakta lamsalBelum ada peringkat

- DiplomacyDokumen9 halamanDiplomacyHarshit Singh67% (3)

- Classical Management TheoriesDokumen23 halamanClassical Management TheorieszhrBelum ada peringkat

- U.S.-China Relations: Great Power Politics: Nguyen Thanh Trung, PH.DDokumen38 halamanU.S.-China Relations: Great Power Politics: Nguyen Thanh Trung, PH.DLoc HuynhBelum ada peringkat

- Lecture - Chapter 2Dokumen2 halamanLecture - Chapter 2maria ronoraBelum ada peringkat

- The National Budget and Local BudgetDokumen42 halamanThe National Budget and Local BudgetCherry Virtucio100% (1)

- Ao2020 0031 PDFDokumen38 halamanAo2020 0031 PDFJohn Jill T. Villamor100% (1)

- Canons of ST Basil The GreatDokumen67 halamanCanons of ST Basil The Greatparintelemaxim100% (1)

- Peoples Republic of ChinaDokumen3 halamanPeoples Republic of ChinaBenTingBelum ada peringkat

- Global Media Giants: Bajmc VDokumen35 halamanGlobal Media Giants: Bajmc VSrinivas KumarBelum ada peringkat

- Group 01.barmmDokumen50 halamanGroup 01.barmmBon Carlo MelocotonBelum ada peringkat

- Philippine Administrative System: Its Components & Power BaseDokumen30 halamanPhilippine Administrative System: Its Components & Power BaseJesus PauliteBelum ada peringkat

- Economic Growth and ProductivityDokumen68 halamanEconomic Growth and Productivityankujai88Belum ada peringkat

- Common Law MarriageDokumen3 halamanCommon Law MarriageTerique Alexander100% (1)

- The Global Media Giants: The Nine Firms That Dominate The WorldDokumen9 halamanThe Global Media Giants: The Nine Firms That Dominate The WorldM Irfan AdityaBelum ada peringkat

- Executive-Legislative Agenda Formulation and Capacity Development Agenda HarmonizationDokumen85 halamanExecutive-Legislative Agenda Formulation and Capacity Development Agenda Harmonizationaeron antonioBelum ada peringkat

- Economic Growth and DevelopmentDokumen39 halamanEconomic Growth and DevelopmentSmileCaturasBelum ada peringkat

- To The Young Women of MalolosDokumen14 halamanTo The Young Women of MalolosAMVERLY MAE OBUGAN BERGADO100% (1)

- Local Government UnitsDokumen15 halamanLocal Government UnitsNicole Reyes100% (1)

- Instructional Materials in Philippine Administrative Thoughts and InstitutionsDokumen59 halamanInstructional Materials in Philippine Administrative Thoughts and InstitutionsSharlotte Ga-asBelum ada peringkat

- International Environmental LAWDokumen22 halamanInternational Environmental LAWDave AlberoBelum ada peringkat

- Indonesia, Cyber Security, DiplomacyDokumen19 halamanIndonesia, Cyber Security, Diplomacyihsan nasihinBelum ada peringkat

- Productivity and Performance of Barangays The Case of The Heritage City of Vigan PhilippinesDokumen13 halamanProductivity and Performance of Barangays The Case of The Heritage City of Vigan PhilippinesAbigail Faye RoxasBelum ada peringkat

- Myanmar: The Politics of Rakhine StateDokumen48 halamanMyanmar: The Politics of Rakhine StaterohingyabloggerBelum ada peringkat

- Book 1 The Republic by PlatoDokumen1 halamanBook 1 The Republic by PlatoHershey Delos SantosBelum ada peringkat

- The Importance of Human Relations in The Workplace: By: Matt PetryniDokumen10 halamanThe Importance of Human Relations in The Workplace: By: Matt Petryniangel janine brojasBelum ada peringkat

- JEF Training Explores Federalism's BenefitsDokumen21 halamanJEF Training Explores Federalism's BenefitsriadelectroBelum ada peringkat

- Government Bureaucracy GovernanceDokumen41 halamanGovernment Bureaucracy GovernanceExia SevenBelum ada peringkat

- Ministry of Finance Strategic Plan: 2012 - 2016Dokumen51 halamanMinistry of Finance Strategic Plan: 2012 - 2016Chola Mukanga100% (2)

- History and Structure of The United Nati PDFDokumen69 halamanHistory and Structure of The United Nati PDFsatyam kumarBelum ada peringkat

- Updates On COA Rules and Regulations and Criteria For Selection of Outstanding Accounting OfficesDokumen42 halamanUpdates On COA Rules and Regulations and Criteria For Selection of Outstanding Accounting OfficessaverjaneBelum ada peringkat

- Critical Review of Public Participation InitiativesDokumen26 halamanCritical Review of Public Participation InitiativesBrian MutieBelum ada peringkat

- Natl. Budget Processing - EconDokumen17 halamanNatl. Budget Processing - EconAli Mark P JauganBelum ada peringkat

- Government Budgeting Process PDFDokumen21 halamanGovernment Budgeting Process PDFKathleen Ebilane PulangcoBelum ada peringkat

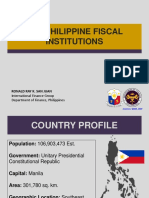

- 06 - (San Juan) Philippines - Fiscal InstitutionsDokumen20 halaman06 - (San Juan) Philippines - Fiscal InstitutionsSharmaine LopezBelum ada peringkat

- Public Fiscal Administration Budgeting ProcessDokumen14 halamanPublic Fiscal Administration Budgeting ProcessKarenina Victoria100% (1)

- Scope of Government Accounting: Congress of The Philippines President of The PhilsDokumen59 halamanScope of Government Accounting: Congress of The Philippines President of The PhilsRed YuBelum ada peringkat

- Budget ProcessDokumen35 halamanBudget ProcessVerena RagaBelum ada peringkat

- The Philippine Fiscal InstitutionsDokumen20 halamanThe Philippine Fiscal InstitutionsADBI EventsBelum ada peringkat

- Presentation Budget Process v3Dokumen33 halamanPresentation Budget Process v3Khym Morales CosepBelum ada peringkat

- Session-4 Corpuz PFADokumen11 halamanSession-4 Corpuz PFAElaiza ReyesBelum ada peringkat

- Narrative ReportDokumen79 halamanNarrative ReportJerald Kim VasquezBelum ada peringkat

- Module 12 The Budgetary ProcessDokumen28 halamanModule 12 The Budgetary ProcessEdward Joseph CaronanBelum ada peringkat

- Public Budget SystemsDokumen38 halamanPublic Budget SystemsMetoo ChyBelum ada peringkat

- Function: Agouti-Signaling Protein Is ADokumen4 halamanFunction: Agouti-Signaling Protein Is ADOH RO X RLEDBelum ada peringkat

- Special Report: Carlos Dominguez's Latest Investment Has Experts in Awe and Big Banks TerrifiedDokumen8 halamanSpecial Report: Carlos Dominguez's Latest Investment Has Experts in Awe and Big Banks TerrifiedDOH RO X RLEDBelum ada peringkat

- Milwaukee Bucks Giannis Antetokounmpo Eastern Conference Semifinal Series Miami HeatDokumen1 halamanMilwaukee Bucks Giannis Antetokounmpo Eastern Conference Semifinal Series Miami HeatDOH RO X RLEDBelum ada peringkat

- Ao2019 0026 PDFDokumen5 halamanAo2019 0026 PDFSAMUEL AUSTRIABelum ada peringkat

- WashDokumen1 halamanWashDOH RO X RLEDBelum ada peringkat

- Alaybalay CityDokumen3 halamanAlaybalay CityDOH RO X RLEDBelum ada peringkat

- dm2019 0112Dokumen6 halamandm2019 0112DOH RO X RLEDBelum ada peringkat

- dm2019 0112Dokumen6 halamandm2019 0112DOH RO X RLEDBelum ada peringkat

- dm2019 0056 1Dokumen33 halamandm2019 0056 1DOH RO X RLEDBelum ada peringkat

- Health Facility Geographic FormDokumen3 halamanHealth Facility Geographic FormquesterBelum ada peringkat

- Boscastle Family Book SeriesDokumen4 halamanBoscastle Family Book SeriesChingirl89100% (1)

- Ja Shooting ClubDokumen6 halamanJa Shooting ClubLeah0% (1)

- Group 2 - Liham Na Sinulat Sa Taong 2070 - SanggunianDokumen5 halamanGroup 2 - Liham Na Sinulat Sa Taong 2070 - SanggunianDominador RomuloBelum ada peringkat

- 502647F 2018Dokumen2 halaman502647F 2018Tilak RajBelum ada peringkat

- By Omar Mustafa Ansari and Faizan Ahmed Memon - Islamic Finance NewsDokumen5 halamanBy Omar Mustafa Ansari and Faizan Ahmed Memon - Islamic Finance Newshumasd453Belum ada peringkat

- Power Plant Cooling IBDokumen11 halamanPower Plant Cooling IBSujeet GhorpadeBelum ada peringkat

- Punjab's Domestic Electrical Appliances Cluster Diagnostic StudyDokumen82 halamanPunjab's Domestic Electrical Appliances Cluster Diagnostic StudyShahzaib HussainBelum ada peringkat

- GE15 ULOcDokumen5 halamanGE15 ULOcKyle Adrian MartinezBelum ada peringkat

- Web Design Wordpress - Hosting Services ListDokumen1 halamanWeb Design Wordpress - Hosting Services ListMotivatioNetBelum ada peringkat

- Tso C139Dokumen5 halamanTso C139Russell GouldenBelum ada peringkat

- UntitledDokumen259 halamanUntitledAnurag KandariBelum ada peringkat

- KPK Progress in PTI's Government (Badar Chaudhry)Dokumen16 halamanKPK Progress in PTI's Government (Badar Chaudhry)badarBelum ada peringkat

- Debate Motions SparringDokumen45 halamanDebate Motions SparringJayden Christian BudimanBelum ada peringkat

- The Impact of E-Commerce in BangladeshDokumen12 halamanThe Impact of E-Commerce in BangladeshMd Ruhul AminBelum ada peringkat

- Mba Dissertation Employee RetentionDokumen8 halamanMba Dissertation Employee RetentionCustomPaperWritingUK100% (1)

- 420jjpb2wmtfx0 PDFDokumen19 halaman420jjpb2wmtfx0 PDFDaudSutrisnoBelum ada peringkat

- Contemporary Management Education: Piet NaudéDokumen147 halamanContemporary Management Education: Piet Naudérolorot958Belum ada peringkat

- Maintain Aircraft Records & Remove Liens Before SaleDokumen1 halamanMaintain Aircraft Records & Remove Liens Before SaleDebs MaxBelum ada peringkat

- Rules For SopeDokumen21 halamanRules For Sopearif zamanBelum ada peringkat