Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Law Notice of DishonorDokumen13 halamanLaw Notice of DishonorLeah Hope Cedro100% (2)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Amazon's Revised Business Service Agreement With Its SellersDokumen38 halamanAmazon's Revised Business Service Agreement With Its SellersCynthia StineBelum ada peringkat

- Types of SwapsDokumen25 halamanTypes of SwapsBinal JasaniBelum ada peringkat

- Kinds of ObligationDokumen428 halamanKinds of ObligationMrcharming Jadraque82% (39)

- The Companies Act, 2013 - MCQ On Business Law With Answers - GST Guntur PDFDokumen6 halamanThe Companies Act, 2013 - MCQ On Business Law With Answers - GST Guntur PDFJITENDER KUMARBelum ada peringkat

- Law 1305 ReviewerDokumen22 halamanLaw 1305 ReviewerGERBGARCIA50% (2)

- Corporation Code ComparisonDokumen57 halamanCorporation Code ComparisonCherith MonteroBelum ada peringkat

- Events After Reporting Period: Chapter 3 - Notes To Financial StatementsDokumen8 halamanEvents After Reporting Period: Chapter 3 - Notes To Financial StatementsKimberly Claire AtienzaBelum ada peringkat

- Onapal Vs CA and Chua GR 90707Dokumen2 halamanOnapal Vs CA and Chua GR 90707Anne Laraga LuansingBelum ada peringkat

- Rights and Duties of Partners NotesDokumen3 halamanRights and Duties of Partners NotesLoveLyzaBelum ada peringkat

- Saura Import and Expert Co. Inc., Vs DBPDokumen2 halamanSaura Import and Expert Co. Inc., Vs DBPtheresaBelum ada peringkat

- Agency and Credit and TransactionsDokumen8 halamanAgency and Credit and TransactionsLUISA MARIE DELA CRUZBelum ada peringkat

- Bcoc 133 2022-23Dokumen13 halamanBcoc 133 2022-23icaibosinterBelum ada peringkat

- Law232 FFFDokumen32 halamanLaw232 FFFRonnel Villaceran SaysonBelum ada peringkat

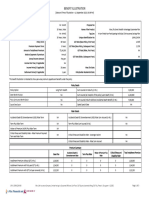

- Benefit Illustration: Death Benefit Multiple Policy Continuance Benefit Option Special Date OptionDokumen3 halamanBenefit Illustration: Death Benefit Multiple Policy Continuance Benefit Option Special Date OptionAlok .kBelum ada peringkat

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap016 PDFDokumen50 halamanSolution Manual Advanced Financial Accounting 8th Edition Baker Chap016 PDFYopie ChandraBelum ada peringkat

- Classification of AgentsDokumen3 halamanClassification of AgentsSrikanth SalvatoreBelum ada peringkat

- Contract Law DIFC Law No. 6 of 2004Dokumen48 halamanContract Law DIFC Law No. 6 of 2004KarthiktrichyBelum ada peringkat

- The Basel AccordsDokumen3 halamanThe Basel AccordsJagrataBelum ada peringkat

- Premium ChartDokumen2 halamanPremium Chartchaudharymeel0% (1)

- Deed of DissolutionDokumen3 halamanDeed of Dissolutionsuresh mahantiBelum ada peringkat

- Capacity of PartiesDokumen4 halamanCapacity of PartiesSuyash KulkarniBelum ada peringkat

- 1.1 Bordwell, D. and Thompson, K. 1997, Glossary', in Film Art: An Edn, Mcgraw Hill, New York, Pp. 477-480Dokumen7 halaman1.1 Bordwell, D. and Thompson, K. 1997, Glossary', in Film Art: An Edn, Mcgraw Hill, New York, Pp. 477-480Melanie SmithBelum ada peringkat

- Contract of Agency: Submitted ToDokumen3 halamanContract of Agency: Submitted ToTamim RahmanBelum ada peringkat

- PPTDokumen27 halamanPPTafeeraBelum ada peringkat

- GM06 A2Dokumen3 halamanGM06 A2JOB ROLEBelum ada peringkat

- Iv. Rights of The Unpaid Seller (Arts. 1525-1535)Dokumen5 halamanIv. Rights of The Unpaid Seller (Arts. 1525-1535)Kathleen Llacer PiczonBelum ada peringkat

- ABC BANKING CORPORATION LTD V H L C NG HA KWONG 2017 SCJ 245 PDFDokumen7 halamanABC BANKING CORPORATION LTD V H L C NG HA KWONG 2017 SCJ 245 PDFJonathan Bruneau0% (1)

- Exercise 5 Business Law Chu Ha GiangDokumen3 halamanExercise 5 Business Law Chu Ha GiangHà Giang ChuBelum ada peringkat

- Characteristics of DerivativesDokumen5 halamanCharacteristics of Derivativesdhirendra shuklaBelum ada peringkat