Anda mungkin juga menyukai

- Hardening by Auditing: A Handbook for Measurably and Immediately Improving the Security Management of Any OrganizationDari EverandHardening by Auditing: A Handbook for Measurably and Immediately Improving the Security Management of Any OrganizationBelum ada peringkat

- CHAPTER 1 Overview of Internal Auditing FazDokumen22 halamanCHAPTER 1 Overview of Internal Auditing FazHanis ZahiraBelum ada peringkat

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachDari EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachPenilaian: 4 dari 5 bintang4/5 (1)

- Ahmad Tariq Bhatti: Dubai, United Arab EmiratesDokumen54 halamanAhmad Tariq Bhatti: Dubai, United Arab EmiratesKhalidBelum ada peringkat

- Independence, Objectivity and Due CareDokumen38 halamanIndependence, Objectivity and Due CareDanica Austria DimalibotBelum ada peringkat

- L3 - Audit Planning, Types of Audit Tests and MaterialityDokumen47 halamanL3 - Audit Planning, Types of Audit Tests and MaterialityPriyankaBelum ada peringkat

- Topic 3, P1), S2, 2022-23Dokumen18 halamanTopic 3, P1), S2, 2022-23CarolBelum ada peringkat

- Internalfinancialcontrolaudit 170227104813Dokumen24 halamanInternalfinancialcontrolaudit 170227104813ShubhamJainBelum ada peringkat

- 15 JournalDokumen4 halaman15 JournalJane DizonBelum ada peringkat

- Risk Management and Internal AuditorDokumen58 halamanRisk Management and Internal AuditorAnanda rizky syifa nabilahBelum ada peringkat

- Best Practices For Internal Audit in Government DepartmentsDokumen15 halamanBest Practices For Internal Audit in Government DepartmentssabhardwajBelum ada peringkat

- Defining Internal Audit Lecture # 2Dokumen10 halamanDefining Internal Audit Lecture # 2Mustafa patel100% (1)

- Topic 6 (Part A)Dokumen34 halamanTopic 6 (Part A)Amanda GuanBelum ada peringkat

- Factsheet: Internal Audit Benefits: Connect Support AdvanceDokumen2 halamanFactsheet: Internal Audit Benefits: Connect Support AdvanceAsfa AsfiaBelum ada peringkat

- CIA P1 SII Independence and ObjectivityDokumen47 halamanCIA P1 SII Independence and ObjectivityJayAr Dela Rosa100% (1)

- Internal Control, Internal Auditor & Risk ManagementDokumen58 halamanInternal Control, Internal Auditor & Risk ManagementWagimin SendjajaBelum ada peringkat

- Chapter 1 - CISDokumen37 halamanChapter 1 - CISMaeNeth Gullan100% (1)

- Unit 1 Internal Audit RoleDokumen7 halamanUnit 1 Internal Audit RoleMark Andrew CabaleBelum ada peringkat

- Internal Audit CharterDokumen7 halamanInternal Audit CharterSritrusta Sukaridhoto100% (1)

- Internal Audit CharterDokumen6 halamanInternal Audit CharterManshu PoorviBelum ada peringkat

- Internal and External AuditorsDokumen19 halamanInternal and External AuditorsSHAMRAIZKHANBelum ada peringkat

- Financial AuditDokumen3 halamanFinancial AuditHenny FaustaBelum ada peringkat

- Chariza L. Colita Aud RPRDokumen20 halamanChariza L. Colita Aud RPRPritz Marc Bautista MorataBelum ada peringkat

- 13 Introduction To Internal AuditingDokumen6 halaman13 Introduction To Internal AuditingShailene DavidBelum ada peringkat

- Audit ProjectDokumen14 halamanAudit ProjectDhara MehtaBelum ada peringkat

- Kirk Report Adtng 422Dokumen21 halamanKirk Report Adtng 422Pritz Marc Bautista MorataBelum ada peringkat

- CIA Challenge Exam (Part 1)Dokumen116 halamanCIA Challenge Exam (Part 1)JohnBelum ada peringkat

- Chapter No.4 OkDokumen5 halamanChapter No.4 OkRajshahi BoardBelum ada peringkat

- Internal Audit Charter of CEMEX HOLDINGS PHILIPPINES, INC. 6 February 2018Dokumen3 halamanInternal Audit Charter of CEMEX HOLDINGS PHILIPPINES, INC. 6 February 2018Erica AndresBelum ada peringkat

- Journal 15: Internal Auditing (Auditing and Assurance Principles)Dokumen10 halamanJournal 15: Internal Auditing (Auditing and Assurance Principles)Daena NicodemusBelum ada peringkat

- Internal AuditingDokumen3 halamanInternal AuditingNhorelajne ManaogBelum ada peringkat

- Audit FrameworkDokumen8 halamanAudit FrameworkRosana PlancoBelum ada peringkat

- The Role of An Auditor in The Achievement of Organisational ObjectivesDokumen68 halamanThe Role of An Auditor in The Achievement of Organisational ObjectivesShuaib OLAJIREBelum ada peringkat

- Managing The IAFDokumen34 halamanManaging The IAFhziqhshahBelum ada peringkat

- Internal ControlDokumen30 halamanInternal ControlMarcel VelascoBelum ada peringkat

- Module 1 Definition Characteristics and GuidanceDokumen28 halamanModule 1 Definition Characteristics and GuidanceJerma Dela CruzBelum ada peringkat

- Handout 1.1-Intro To Internal AuditingDokumen18 halamanHandout 1.1-Intro To Internal AuditingJhon Ray RabaraBelum ada peringkat

- Post Test: Lesson 1: Introduction To AuditingDokumen2 halamanPost Test: Lesson 1: Introduction To AuditingShaira UntalanBelum ada peringkat

- Revision Week: Auditing and Assurance 2 21 Mar 2019Dokumen56 halamanRevision Week: Auditing and Assurance 2 21 Mar 2019Fatimah AzzahraBelum ada peringkat

- Internal Audit Charter: February 2021Dokumen7 halamanInternal Audit Charter: February 2021Seyfeddine SahliBelum ada peringkat

- Auditing and Internal ControlDokumen73 halamanAuditing and Internal ControlArjeune Victoria BulaonBelum ada peringkat

- OM and CourseMaterial of CertificateProgramme On Internal AuditDokumen404 halamanOM and CourseMaterial of CertificateProgramme On Internal AuditMRL AccountsBelum ada peringkat

- Solution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingDokumen9 halamanSolution Manual For Internal Auditing Assurance and Consulting Services 2nd Edition by RedingBrianWelchxqdm100% (38)

- Intosai Gov 9120 eDokumen10 halamanIntosai Gov 9120 eCarlos David Lopez NoriegaBelum ada peringkat

- Chapter 2 Internal AuditDokumen11 halamanChapter 2 Internal AuditSaurabh GogawaleBelum ada peringkat

- CH01 Illustrative Solutions v.4Dokumen8 halamanCH01 Illustrative Solutions v.4BrandonBelum ada peringkat

- Audit: Quality System Quality Management System ISO ISO 9001Dokumen6 halamanAudit: Quality System Quality Management System ISO ISO 9001Sherwin MosomosBelum ada peringkat

- Internal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiaDokumen86 halamanInternal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiacuixiBelum ada peringkat

- 2017 Model Internal Audit Activity Charter PDFDokumen9 halaman2017 Model Internal Audit Activity Charter PDFChristen CastilloBelum ada peringkat

- Internal Audit: Best Practices For Community BanksDokumen13 halamanInternal Audit: Best Practices For Community BanksRed WaneBelum ada peringkat

- Chapter1Dokumen4 halamanChapter1Keanne Armstrong100% (1)

- Acctg. Major 6 - Auditing and Internal ControlDokumen12 halamanAcctg. Major 6 - Auditing and Internal ControlTrayle HeartBelum ada peringkat

- Slides - Chapter 9Dokumen7 halamanSlides - Chapter 9Thu TrangBelum ada peringkat

- Chapter 4 - Internal ControlDokumen60 halamanChapter 4 - Internal Controlyebegashet100% (1)

- Corporate Governance TM6Dokumen26 halamanCorporate Governance TM611210000015Belum ada peringkat

- ITAudit - Internal AuditingDokumen16 halamanITAudit - Internal AuditingDharmawan SalimBelum ada peringkat

- Internal AuditDokumen54 halamanInternal AuditAhmad Tariq Bhatti100% (1)

- Audit InternalDokumen49 halamanAudit InternalMaya Amellia RosfitrianiBelum ada peringkat

- Chapter 1 - Introduction To IA STDTDokumen21 halamanChapter 1 - Introduction To IA STDTNor Syahra AjinimBelum ada peringkat

- Chapter 1 Illustrative SolutionsDokumen6 halamanChapter 1 Illustrative Solutionsnemokiller07100% (2)

- Nahid Mahmud Firoz 1935409660 Term Paper Mkt625.1Dokumen14 halamanNahid Mahmud Firoz 1935409660 Term Paper Mkt625.1Nahid Mahmud Firoz 1935409660Belum ada peringkat

- CH 11 MasteryDokumen11 halamanCH 11 Mastery1anthonyanthony7Belum ada peringkat

- For Emergencies and Complaints Please CallDokumen1 halamanFor Emergencies and Complaints Please CallUmar FarooqBelum ada peringkat

- Audit Case StudyDokumen3 halamanAudit Case StudyTaha AhmedBelum ada peringkat

- Adjusting EntriesDokumen2 halamanAdjusting Entriesitsayuhthing100% (1)

- Other Trade Exporters DatabaseDokumen126 halamanOther Trade Exporters DatabaseKunwar SaigalBelum ada peringkat

- Crane NIT 065Dokumen45 halamanCrane NIT 065rizwan hassanBelum ada peringkat

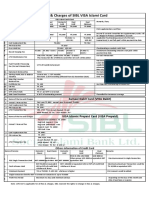

- Fees and Charges of SIBL Islami CardDokumen1 halamanFees and Charges of SIBL Islami CardMd YusufBelum ada peringkat

- BBMF2814 Week 5Dokumen6 halamanBBMF2814 Week 5CHIA MIN LIEWBelum ada peringkat

- BOOKLET N3 Appendix MORE INTERVIEW QUESTIONS p104 108Dokumen5 halamanBOOKLET N3 Appendix MORE INTERVIEW QUESTIONS p104 108DamianBelum ada peringkat

- EVIDENCIA 2 Cafe SenaDokumen5 halamanEVIDENCIA 2 Cafe SenaDayana AmaroBelum ada peringkat

- RPC MT 4Dokumen3 halamanRPC MT 4Lasitha MuhandiramgeBelum ada peringkat

- 3rd Periodical Examination - Computer 8Dokumen3 halaman3rd Periodical Examination - Computer 8Jayjay TorresBelum ada peringkat

- 144 A1 Eng - 31 August 2022Dokumen13 halaman144 A1 Eng - 31 August 2022DRACCBelum ada peringkat

- Centrale À Cycle Combiné Bi-Arbres Rades C 1 X 450MW: GT Control Oil Jib Crane Installation ProcedureDokumen3 halamanCentrale À Cycle Combiné Bi-Arbres Rades C 1 X 450MW: GT Control Oil Jib Crane Installation ProcedureWajdi MansourBelum ada peringkat

- Aditya Vikram Birla FinalDokumen12 halamanAditya Vikram Birla FinalPooja_Shah020186Belum ada peringkat

- Pivot Point Indicator (HowToTrade Cheat Sheet)Dokumen4 halamanPivot Point Indicator (HowToTrade Cheat Sheet)Med Ayman AyoubBelum ada peringkat

- MGT312-Assignment 1-1st-2022-23Dokumen8 halamanMGT312-Assignment 1-1st-2022-23saidBelum ada peringkat

- Unit Ii Life InsuranceDokumen12 halamanUnit Ii Life InsuranceNice NameBelum ada peringkat

- Social Media MarketingDokumen6 halamanSocial Media MarketingS YuvashriBelum ada peringkat

- Fundamentals of Accounting II AssignmentDokumen2 halamanFundamentals of Accounting II Assignmentbirukandualem946Belum ada peringkat

- CoTM Thesis - Engida EjiguDokumen125 halamanCoTM Thesis - Engida EjiguAddis GetahunBelum ada peringkat

- Op Transaction History UX527!05!2023Dokumen8 halamanOp Transaction History UX527!05!2023srm finservBelum ada peringkat

- Financial Management SyllabusDokumen7 halamanFinancial Management SyllabusAireen Rose Rabino Manguiran0% (1)

- Strategic Management: Corporate Strategy: Vertical Integration and DiversificationDokumen37 halamanStrategic Management: Corporate Strategy: Vertical Integration and DiversificationSyed MujtabaBelum ada peringkat

- BG PST 115-1200-2023Dokumen1 halamanBG PST 115-1200-2023arieznavalBelum ada peringkat

- CottonKing CaseDokumen2 halamanCottonKing CaseBhavikBelum ada peringkat

- Operation Project Report For MBADokumen4 halamanOperation Project Report For MBAcharlieBelum ada peringkat

- Business FinanceDokumen221 halamanBusiness FinanceMatthew GonzalesBelum ada peringkat

- Law of Financial Institutions and Securities BLO3405: Vu - Edu.auDokumen35 halamanLaw of Financial Institutions and Securities BLO3405: Vu - Edu.auYuting WangBelum ada peringkat