Anda mungkin juga menyukai

- US Economic Briefing: High Frequency Indicators: Yardeni Research, IncDokumen28 halamanUS Economic Briefing: High Frequency Indicators: Yardeni Research, IncmaxBelum ada peringkat

- Revenues & Expenses by Business Unit (A4 Portrait)Dokumen5 halamanRevenues & Expenses by Business Unit (A4 Portrait)umeshsoni166Belum ada peringkat

- 2009-09-15 SN EUL eDokumen1 halaman2009-09-15 SN EUL erogerbaettigBelum ada peringkat

- QC Printing Technology User GuideDokumen28 halamanQC Printing Technology User Guideecdtcenter100% (1)

- Us Charts CondDokumen8 halamanUs Charts CondJonathan NixonBelum ada peringkat

- Lecture 03Dokumen66 halamanLecture 03Thi NtdBelum ada peringkat

- The India Advantage After The Comprehensive Economic Partnership AgreementDokumen51 halamanThe India Advantage After The Comprehensive Economic Partnership Agreementrohitgupta11288Belum ada peringkat

- Chapter 1 - 3Dokumen45 halamanChapter 1 - 3Hana YukiBelum ada peringkat

- Sokkelaret 2017 Engelsk PresentasjonDokumen25 halamanSokkelaret 2017 Engelsk PresentasjonHải Thân NgọcBelum ada peringkat

- GEP June 2020 Chapter3 Box1Dokumen41 halamanGEP June 2020 Chapter3 Box1Anonymous ZIMIwJWgABelum ada peringkat

- Catalysts: Brookite, The Least Known Tio PhotocatalystDokumen38 halamanCatalysts: Brookite, The Least Known Tio PhotocatalystElizael De Jesus GonçalvesBelum ada peringkat

- Manual ECC 230V-07.2015Dokumen16 halamanManual ECC 230V-07.2015Mohammed Qaid Alathwary100% (1)

- Manual ECC 230V-07.2015Dokumen16 halamanManual ECC 230V-07.2015coco MP100% (1)

- M&A Finance TrendsDokumen51 halamanM&A Finance TrendsPaul GhanimehBelum ada peringkat

- Watershed Modelling: Lecture 0: IntroductionDokumen9 halamanWatershed Modelling: Lecture 0: IntroductionAcademic RhydroBelum ada peringkat

- Steel beam dimension and installation guideDokumen1 halamanSteel beam dimension and installation guideAlen Dundi KurticBelum ada peringkat

- Financial Structure and Macroeconomic Volatility: A Panel Data AnalysisDokumen34 halamanFinancial Structure and Macroeconomic Volatility: A Panel Data AnalysisNizar HezziBelum ada peringkat

- Total Foodgrains - All India Production: Million TonnesDokumen1 halamanTotal Foodgrains - All India Production: Million TonnesHirak BiswasBelum ada peringkat

- Unit 1 - Introduction To Economics TestDokumen5 halamanUnit 1 - Introduction To Economics TestTodd FedanBelum ada peringkat

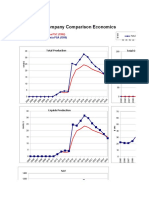

- Company Comparison Economics: Merak ®Dokumen13 halamanCompany Comparison Economics: Merak ®Tripoli ManoBelum ada peringkat

- Jindal Steel and Power LTD: 1.1 Fundamentalanalysis (Company Analysis by Financial Ratio'S)Dokumen3 halamanJindal Steel and Power LTD: 1.1 Fundamentalanalysis (Company Analysis by Financial Ratio'S)yash chauhanBelum ada peringkat

- Disbursing Cash To Shareholders: Frequently Asked Questions About Buybacks and DividendsDokumen21 halamanDisbursing Cash To Shareholders: Frequently Asked Questions About Buybacks and DividendsDQBelum ada peringkat

- Session 14 - Balasubramanyam, V N and Virmani, Swati - The Enigmatic Services Sector of IndiaDokumen26 halamanSession 14 - Balasubramanyam, V N and Virmani, Swati - The Enigmatic Services Sector of IndiaChahat NegiBelum ada peringkat

- China, Global Imbalances and Global Restructurings: Andrew M. Fischer Institute of Social StudiesDokumen11 halamanChina, Global Imbalances and Global Restructurings: Andrew M. Fischer Institute of Social StudiesmontagesBelum ada peringkat

- Mail Eley 1 Foundation DetailDokumen1 halamanMail Eley 1 Foundation DetailManu S KashyapBelum ada peringkat

- 01_Commodity_price_volatilityDokumen12 halaman01_Commodity_price_volatilityjoeBelum ada peringkat

- Return period for maximum values in years - Normal distribution scaleDokumen1 halamanReturn period for maximum values in years - Normal distribution scaleAdrian MirandaBelum ada peringkat

- Sheiko Modified Hypertrophy v4.0Dokumen24 halamanSheiko Modified Hypertrophy v4.0gersaBelum ada peringkat

- A.2 Norway: Volumes of Associated Gas Flared On Norwegian Continental ShelfDokumen5 halamanA.2 Norway: Volumes of Associated Gas Flared On Norwegian Continental Shelfzubair1950Belum ada peringkat

- Behind the Food Crisis in India and the Global SouthDokumen26 halamanBehind the Food Crisis in India and the Global SouthAnqur1984Belum ada peringkat

- Research PaperDokumen23 halamanResearch PaperbhaskkarBelum ada peringkat

- 6-Part 1 PDFDokumen14 halaman6-Part 1 PDFAswani B RajBelum ada peringkat

- Height For AgeDokumen10 halamanHeight For AgeSuwenitaBelum ada peringkat

- Robin Nandy PresentationDokumen25 halamanRobin Nandy Presentationnancy bautistaBelum ada peringkat

- MB 17 Redmond 0419Dokumen4 halamanMB 17 Redmond 0419TBP_Think_TankBelum ada peringkat

- Sheiko Modified Hypertrophy v4.0Dokumen20 halamanSheiko Modified Hypertrophy v4.0visam14083Belum ada peringkat

- CMO April 2021 Special FocusDokumen15 halamanCMO April 2021 Special FocusabdulazizBelum ada peringkat

- 1 2 " Pa - 7 5 1 2 M F A B U L O U S Aplikasi Pemakaian: Respon Frekuensi ImpedansiDokumen2 halaman1 2 " Pa - 7 5 1 2 M F A B U L O U S Aplikasi Pemakaian: Respon Frekuensi ImpedansifahrilBelum ada peringkat

- RBA Discusses Strong Commodity Prices and Household Spending RestraintDokumen13 halamanRBA Discusses Strong Commodity Prices and Household Spending Restraintron22Belum ada peringkat

- Calculator Instructions: Casio fx-9860G PLUSDokumen9 halamanCalculator Instructions: Casio fx-9860G PLUSyouri hanafiahBelum ada peringkat

- Enrollment by Gender: OA CH ES D SE MI NA R ES EM IN ARDokumen4 halamanEnrollment by Gender: OA CH ES D SE MI NA R ES EM IN ARKaren Delos Santos ToledoBelum ada peringkat

- Growth charts for boys aged 2-5 yearsDokumen3 halamanGrowth charts for boys aged 2-5 yearstiarapuspa23Belum ada peringkat

- Sheet 1Dokumen2 halamanSheet 1sagarBelum ada peringkat

- Globalization Trends - Guest Lecture May 2023Dokumen23 halamanGlobalization Trends - Guest Lecture May 2023Spare Email AccountBelum ada peringkat

- BEAM 300X600: Country Garden BSDDokumen1 halamanBEAM 300X600: Country Garden BSDhendriBelum ada peringkat

- Inf - Ten-Q2 2017Dokumen14 halamanInf - Ten-Q2 2017rocioBelum ada peringkat

- 3a. Prestige PatternsDokumen60 halaman3a. Prestige PatternsNhat Quang Nguyen MyBelum ada peringkat

- MIB0900510 UpdateDokumen2 halamanMIB0900510 Updatebackup655Belum ada peringkat

- WP 1382Dokumen27 halamanWP 1382quynhhuynh.31211027045Belum ada peringkat

- The Mexican Economy in 2022: Outlook and Challenges: Información ConfidencialDokumen22 halamanThe Mexican Economy in 2022: Outlook and Challenges: Información ConfidencialDaniel RamirezBelum ada peringkat

- 환공 솔루션Dokumen119 halaman환공 솔루션김채원Belum ada peringkat

- Capital Flows: Issues and PoliciesDokumen39 halamanCapital Flows: Issues and PoliciesRefatBelum ada peringkat

- Tallow As FuelDokumen3 halamanTallow As FuelMartin mtawaliBelum ada peringkat

- Bridgewater Presentation 2017-10 San JoaquinDokumen28 halamanBridgewater Presentation 2017-10 San Joaquinrdarty100% (2)

- Optimization Modelling For Business AnalysisDokumen3 halamanOptimization Modelling For Business AnalysispranavBelum ada peringkat

- General Notes:: LNG Canada ProjectDokumen1 halamanGeneral Notes:: LNG Canada ProjectChiều TànBelum ada peringkat

- 2017 Annual Housing Market Survey WebinarDokumen62 halaman2017 Annual Housing Market Survey WebinarC.A.R. Research & EconomicsBelum ada peringkat

- The Impact of Sovereign Credit Risk On Bank Funding ConditionsDokumen52 halamanThe Impact of Sovereign Credit Risk On Bank Funding Conditionscreditplumber100% (1)

- Building Resilient Financial Systems: Macroprudential Regimes and Securities Market RegulationDokumen15 halamanBuilding Resilient Financial Systems: Macroprudential Regimes and Securities Market Regulationcreditplumber100% (1)

- IMF: Possible Unintended Consequences of Basel III & Solvency IIDokumen71 halamanIMF: Possible Unintended Consequences of Basel III & Solvency IIcreditplumber100% (1)

- BP's Failure To Debias: Underscoring The Importance of Behavioral Corporate FinanceDokumen49 halamanBP's Failure To Debias: Underscoring The Importance of Behavioral Corporate FinancecreditplumberBelum ada peringkat

- Financial Protectionism: The First TestsDokumen30 halamanFinancial Protectionism: The First TestscreditplumberBelum ada peringkat

- IFRS Illustrative Financial Statements Banks June 2011: KPMGDokumen244 halamanIFRS Illustrative Financial Statements Banks June 2011: KPMGcreditplumber100% (1)

- McKinsey's Mapping Global Capital Markets 2011Dokumen38 halamanMcKinsey's Mapping Global Capital Markets 2011creditplumber100% (1)

- Compelxity, Concentration and ContagionDokumen34 halamanCompelxity, Concentration and Contagioncreditplumber100% (1)

- HaircutsDokumen6 halamanHaircutscreditplumber100% (1)

- Complexity As A Catalyst of Market Failure: A Law and Engineering InquiryDokumen50 halamanComplexity As A Catalyst of Market Failure: A Law and Engineering Inquirycreditplumber100% (1)

- Regulating The Off Balance Sheet Exposure of BanksDokumen43 halamanRegulating The Off Balance Sheet Exposure of Bankscreditplumber100% (1)

- The Bank of England, Prudential Regulation Auhority: Our Approach To Banking SupervisionDokumen27 halamanThe Bank of England, Prudential Regulation Auhority: Our Approach To Banking SupervisioncreditplumberBelum ada peringkat

- UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK in Re: LEHMAN BROTHERS SECURITIES AND ERISA LITIGATIONDokumen110 halamanUNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK in Re: LEHMAN BROTHERS SECURITIES AND ERISA LITIGATIONcreditplumber100% (1)

- The Race To Zero: Speech by Andrew HaldaneDokumen25 halamanThe Race To Zero: Speech by Andrew HaldanecreditplumberBelum ada peringkat

- The Biggest Idea in Development That No-One Really Tried.Dokumen26 halamanThe Biggest Idea in Development That No-One Really Tried.creditplumberBelum ada peringkat

- Global Imbalances and The Financial Crisis: Link or No Link?Dokumen43 halamanGlobal Imbalances and The Financial Crisis: Link or No Link?creditplumberBelum ada peringkat

- The Bank Lending Channel: Lessons From The Crisis: BIS Working PaperDokumen36 halamanThe Bank Lending Channel: Lessons From The Crisis: BIS Working PapercreditplumberBelum ada peringkat

- Optimal Collective Action Clause ThresholdsDokumen31 halamanOptimal Collective Action Clause ThresholdscreditplumberBelum ada peringkat

- Bank of Englands Agents Summary of Business Conditions: April 2011Dokumen5 halamanBank of Englands Agents Summary of Business Conditions: April 2011creditplumberBelum ada peringkat

- Key Issues For UK Monetary Policy: Andrew Sentance, External Member of BofE MPCDokumen20 halamanKey Issues For UK Monetary Policy: Andrew Sentance, External Member of BofE MPCcreditplumberBelum ada peringkat

- Institute of International Finance :addressing Priority Issues in Cross-Border ResolutionDokumen44 halamanInstitute of International Finance :addressing Priority Issues in Cross-Border ResolutioncreditplumberBelum ada peringkat

- This Time Is The Same: Using Bank Performance in 1998 To Explain Bank Performance During The Recent Financial CrisisDokumen51 halamanThis Time Is The Same: Using Bank Performance in 1998 To Explain Bank Performance During The Recent Financial CrisiscreditplumberBelum ada peringkat

- The Short LongDokumen19 halamanThe Short Longcreditplumber100% (1)

- Macroprudential Policy: Building Financial Stability Institutions: Paul Tucker, Deputy Governor, Financial Stability, Bank of EnglandDokumen16 halamanMacroprudential Policy: Building Financial Stability Institutions: Paul Tucker, Deputy Governor, Financial Stability, Bank of EnglandcreditplumberBelum ada peringkat

- Banking Vulnerability Indicators - IMF April '11 GFSRDokumen1 halamanBanking Vulnerability Indicators - IMF April '11 GFSRcreditplumberBelum ada peringkat

- OECD Paper: Risk Management & Corporate Governance - Richard AndersonDokumen49 halamanOECD Paper: Risk Management & Corporate Governance - Richard AndersoncreditplumberBelum ada peringkat

- Indebtedness & Leverage in Selected Advanced Economies - IMF April 2011Dokumen1 halamanIndebtedness & Leverage in Selected Advanced Economies - IMF April 2011creditplumberBelum ada peringkat

- The Big Fish Small Pond Problem: Andrew Haldane, Bank of EnglandDokumen24 halamanThe Big Fish Small Pond Problem: Andrew Haldane, Bank of EnglandcreditplumberBelum ada peringkat

- ICB Interim Report Full VersionDokumen214 halamanICB Interim Report Full VersionJonathan RosenthalBelum ada peringkat

- Basel III: Stronger Banks and A More Resilient Financial System: Stefan Walter, Sec-Gnrl of Basel Committee of Banking SupervisionDokumen12 halamanBasel III: Stronger Banks and A More Resilient Financial System: Stefan Walter, Sec-Gnrl of Basel Committee of Banking SupervisioncreditplumberBelum ada peringkat

- Chapter 19 Foreign Exchange Risk: 1. ObjectivesDokumen31 halamanChapter 19 Foreign Exchange Risk: 1. ObjectivesDerickBrownThe-Gentleman100% (1)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDokumen42 halamanInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownRaja GoharBelum ada peringkat

- Term Paper For MicroeconomicsDokumen8 halamanTerm Paper For Microeconomicsafdtbbhtz100% (1)

- Marketing Management ProjectDokumen6 halamanMarketing Management ProjectEduard MagurianuBelum ada peringkat

- Describing A GraphDokumen16 halamanDescribing A GraphBudi PrakosoBelum ada peringkat

- Kenya Economic Survey 2009Dokumen55 halamanKenya Economic Survey 2009odongochrisBelum ada peringkat

- Republic Act No. 9829 An Act Establishing The Pre-Need Code of The PhillpplnesDokumen19 halamanRepublic Act No. 9829 An Act Establishing The Pre-Need Code of The PhillpplnesKhalee SiBelum ada peringkat

- Tutorial 3 AnswersDokumen5 halamanTutorial 3 Answers杰克 l孙Belum ada peringkat

- Fomc Proj Tabl 20240320Dokumen17 halamanFomc Proj Tabl 20240320Dinheirama.comBelum ada peringkat

- Paper 1 Essay QuestionsDokumen26 halamanPaper 1 Essay QuestionsSteve0% (2)

- Kbuzz: Sector InsightsDokumen42 halamanKbuzz: Sector InsightsvivekanandsBelum ada peringkat

- Court Pick Parries Questions On Abortion and Health Law: What's NewsDokumen48 halamanCourt Pick Parries Questions On Abortion and Health Law: What's News233701Belum ada peringkat

- Inflation Dynamics in Transition Economy of Lao PDR.Dokumen31 halamanInflation Dynamics in Transition Economy of Lao PDR.Kongpasa Sengsourivong100% (1)

- Test Bank Econ 212 Ch5Dokumen23 halamanTest Bank Econ 212 Ch5arati.kundu.1943Belum ada peringkat

- Marketing Mix Magazine Jan Feb 08Dokumen60 halamanMarketing Mix Magazine Jan Feb 08marketing mix magazineBelum ada peringkat

- PESTEL Analysis of McdonaldsDokumen9 halamanPESTEL Analysis of McdonaldsHimank Gupta88% (17)

- Prelims 2020 Crux of Indian Economy PDFDokumen274 halamanPrelims 2020 Crux of Indian Economy PDFAngad KumarBelum ada peringkat

- Journal of Regulation & Risk - North Asia Volume II, Summer/Fall Edition 2010Dokumen270 halamanJournal of Regulation & Risk - North Asia Volume II, Summer/Fall Edition 2010Christopher Dale RogersBelum ada peringkat

- Company Analysis On Pacific Jeans LTDDokumen84 halamanCompany Analysis On Pacific Jeans LTDKeya BiswasBelum ada peringkat

- GS - Outlook For 2023Dokumen56 halamanGS - Outlook For 2023Aaron WangBelum ada peringkat

- Rethinking Monetary Policy After the CrisisDokumen23 halamanRethinking Monetary Policy After the CrisisAlexDuarteVelasquezBelum ada peringkat

- Attempt Ant Four Case Study CASE - 1 Power For All: Myth or Reality?Dokumen9 halamanAttempt Ant Four Case Study CASE - 1 Power For All: Myth or Reality?Jay KrishnaBelum ada peringkat

- 5945-Article Text-17391-1-10-20181019 PDFDokumen32 halaman5945-Article Text-17391-1-10-20181019 PDFfk tubeBelum ada peringkat

- Central Bank of IndiaDokumen70 halamanCentral Bank of Indianandini_mba4870100% (6)

- Lecture 1-SOB 2215 March 2023Dokumen98 halamanLecture 1-SOB 2215 March 2023zulufelix029Belum ada peringkat

- Factors Affecting Stock Markets in South AsiaDokumen15 halamanFactors Affecting Stock Markets in South AsiaAli MohammedBelum ada peringkat

- Mastering-the-Market-Cycle-Notes-and-Takeaways.docxDokumen12 halamanMastering-the-Market-Cycle-Notes-and-Takeaways.docxGeneralmailBelum ada peringkat

- Liam Mescall Swaption ProjectDokumen20 halamanLiam Mescall Swaption ProjectLiam MescallBelum ada peringkat

- PEST (EL) Analysis - Https://kfknowledgebank - Kaplan.co - Uk/business-Strategy/strategic-Analysis/pestelDokumen2 halamanPEST (EL) Analysis - Https://kfknowledgebank - Kaplan.co - Uk/business-Strategy/strategic-Analysis/pestelSalah UddinBelum ada peringkat

- Economics Marking - Scheme - PB - Ii - 2022-23Dokumen9 halamanEconomics Marking - Scheme - PB - Ii - 2022-23TRAP GAMINGBelum ada peringkat