Anda mungkin juga menyukai

- Mercer Expat BestDokumen127 halamanMercer Expat BestShreyoshi ChatterjeeBelum ada peringkat

- Human Resource ManagementDokumen17 halamanHuman Resource ManagementJoynul Abedin100% (1)

- Vendor Statutory Compliance Checklist-KarnatakaDokumen1 halamanVendor Statutory Compliance Checklist-Karnatakamanishdg50% (6)

- Starbucks Audit HR CLASSDokumen13 halamanStarbucks Audit HR CLASSbiomedph22100% (3)

- Chapter 7-Dealing With Management and Operation Issues (Strategy Implementation)Dokumen78 halamanChapter 7-Dealing With Management and Operation Issues (Strategy Implementation)Maria Cassandra O. Ramos0% (2)

- Example Formal Report Methods For Motivating EmployeesDokumen15 halamanExample Formal Report Methods For Motivating EmployeesnrljnnhBelum ada peringkat

- Sip Project SailDokumen68 halamanSip Project SailRavi Kant RajBelum ada peringkat

- ESI & PF Brief InformationDokumen8 halamanESI & PF Brief InformationPrashant Dhangar0% (1)

- Labour and Industrial Law - October 15-16,2022Dokumen208 halamanLabour and Industrial Law - October 15-16,2022NAZIRBelum ada peringkat

- FAQ-Employee Provident Fund.311162455Dokumen5 halamanFAQ-Employee Provident Fund.311162455penusilaBelum ada peringkat

- PF & ESI Compliance GuideDokumen15 halamanPF & ESI Compliance GuideAbdul KhadhirBelum ada peringkat

- Statutory ComplianceDokumen16 halamanStatutory ComplianceGovindBelum ada peringkat

- Anirudh Kumar JainDokumen4 halamanAnirudh Kumar JainAnirudh JainBelum ada peringkat

- Aparajitha - HR Compliance ServicesDokumen6 halamanAparajitha - HR Compliance ServicessunilboyalaBelum ada peringkat

- Salary Break UpDokumen17 halamanSalary Break UpRam Surya Prakash DommetiBelum ada peringkat

- Statutory Compliance ChecklistDokumen5 halamanStatutory Compliance ChecklistMuthu ManikandanBelum ada peringkat

- Form No. 9: (See Rule 107)Dokumen1 halamanForm No. 9: (See Rule 107)13sandipBelum ada peringkat

- RegistrationDokumen15 halamanRegistrationpratikdhond100% (3)

- India Employee HandbookDokumen54 halamanIndia Employee Handbooksunil.puppalaBelum ada peringkat

- Employee Pension SchemeDokumen6 halamanEmployee Pension SchemeAarthi PadmanabhanBelum ada peringkat

- Registers and reports required under Factories ActDokumen2 halamanRegisters and reports required under Factories ActSanjay SinghBelum ada peringkat

- Contract Labour RegisterDokumen34 halamanContract Labour Registerravinder.singh19853857Belum ada peringkat

- Relevant Dates: 15-Apr QuarterlyDokumen6 halamanRelevant Dates: 15-Apr Quarterlysanyu1208Belum ada peringkat

- Check List of All Labour LawsDokumen16 halamanCheck List of All Labour LawsGoutham ShettyBelum ada peringkat

- Industrial Employment - Standing Orders Act, 1946Dokumen11 halamanIndustrial Employment - Standing Orders Act, 1946rashmi_shantikumar100% (1)

- Recognition of Trade UnionsDokumen15 halamanRecognition of Trade UnionsHarsh Raj GuptaBelum ada peringkat

- Checklist-Various Statutory Compliances SR - No. Statue DescriptionDokumen3 halamanChecklist-Various Statutory Compliances SR - No. Statue Descriptionmanan3466Belum ada peringkat

- Payment of Bonus Act 1965Dokumen39 halamanPayment of Bonus Act 1965Manojkumar MohanasundramBelum ada peringkat

- Monthwise Statutory Compliance ChecklistDokumen9 halamanMonthwise Statutory Compliance ChecklistGaurav2192Belum ada peringkat

- Basics of Employee Provident Fund: EPF EPS EDLISDokumen11 halamanBasics of Employee Provident Fund: EPF EPS EDLISrajlumarBelum ada peringkat

- Provident Fund (PF)Dokumen13 halamanProvident Fund (PF)chandub6Belum ada peringkat

- Statutory Compliance TrackerDokumen6 halamanStatutory Compliance TrackerHemanth KanakamedalaBelum ada peringkat

- Labour Law Compliance Due DatesDokumen4 halamanLabour Law Compliance Due DatesAchuthan RamanBelum ada peringkat

- Employee Provident Fund ComplianceDokumen3 halamanEmployee Provident Fund ComplianceAswanth GokaBelum ada peringkat

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFDokumen52 halamanCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGBelum ada peringkat

- Updates On Buyback Offer (Company Update)Dokumen56 halamanUpdates On Buyback Offer (Company Update)Shyam SunderBelum ada peringkat

- Family Pension SchemeDokumen15 halamanFamily Pension SchemeJitu Choudhary100% (1)

- Contract Labour (Regulation & Abolition) ActDokumen19 halamanContract Labour (Regulation & Abolition) Acthcm770fhBelum ada peringkat

- Maternity Benefit Act 1961Dokumen21 halamanMaternity Benefit Act 1961shravaniBelum ada peringkat

- Salary Taxation and Related Concepts: Malik Faisal Mehmood, ACADokumen25 halamanSalary Taxation and Related Concepts: Malik Faisal Mehmood, ACAMalik FaisalBelum ada peringkat

- Job Offer LetterDokumen6 halamanJob Offer Letteranuplakade930Belum ada peringkat

- Shops and Establishment ActDokumen4 halamanShops and Establishment ActYoddhri DikshitBelum ada peringkat

- Esop Process & Faq'sDokumen10 halamanEsop Process & Faq'ssaurabhsarafBelum ada peringkat

- Exit PolicyDokumen8 halamanExit PolicyjaiminwfpBelum ada peringkat

- Statutory CompliancesDokumen4 halamanStatutory CompliancesPratibha ChopraBelum ada peringkat

- Kar Shops Commercial Forms FormatDokumen16 halamanKar Shops Commercial Forms FormatbelvaisudheerBelum ada peringkat

- Statutory ComplianceDokumen2 halamanStatutory Compliancemax997Belum ada peringkat

- Ind As 2 PDFDokumen26 halamanInd As 2 PDFmanan3466Belum ada peringkat

- Abstract of Minimum Wages ActDokumen7 halamanAbstract of Minimum Wages ActManikanta SatishBelum ada peringkat

- Daksh Leave Policy (India)Dokumen12 halamanDaksh Leave Policy (India)ajithk75733Belum ada peringkat

- EPF Provident Fund CalculatorDokumen6 halamanEPF Provident Fund CalculatorUtkal SolankiBelum ada peringkat

- Statutory ComplianceDokumen37 halamanStatutory ComplianceNitin SaxenaBelum ada peringkat

- Certificates / Registrations / Licences / NOC's / Approvals / SanctionsDokumen18 halamanCertificates / Registrations / Licences / NOC's / Approvals / Sanctionsgovinds_2100% (1)

- The List of Components Which You Can Use For Salary BreakupDokumen8 halamanThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXBelum ada peringkat

- EPFO's role under EPF Act 1952Dokumen6 halamanEPFO's role under EPF Act 1952Ajay TiwariBelum ada peringkat

- Compliance PDFDokumen20 halamanCompliance PDFSUBHANKAR PALBelum ada peringkat

- Whichever Is Lower Is Exempt From Tax. For ExampleDokumen13 halamanWhichever Is Lower Is Exempt From Tax. For ExampleNasir AhmedBelum ada peringkat

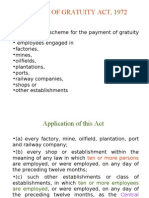

- Gratuity ActDokumen34 halamanGratuity Actapi-369848680% (5)

- Local Conveyance PolicyDokumen4 halamanLocal Conveyance PolicyNazneen KhanBelum ada peringkat

- DGM Annexure B Know Your Pay ComponentsDokumen3 halamanDGM Annexure B Know Your Pay ComponentsaakritishellBelum ada peringkat

- What Is A Flexible Benefit Plan in A Salary Breakup? - QuoraDokumen8 halamanWhat Is A Flexible Benefit Plan in A Salary Breakup? - QuoraSiBelum ada peringkat

- Contract Employees in IndiaDokumen21 halamanContract Employees in IndiaShyamali SaxenaBelum ada peringkat

- The Maternity Benefit Act 2017 - A Reveiw NoteDokumen11 halamanThe Maternity Benefit Act 2017 - A Reveiw NoteDharmeshBelum ada peringkat

- Compliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Dokumen57 halamanCompliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Himanshu ShahBelum ada peringkat

- Compliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Dokumen57 halamanCompliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Pradee Srinivas GowdaBelum ada peringkat

- Provident Fund Act SummaryDokumen10 halamanProvident Fund Act SummaryhemlatauBelum ada peringkat

- QuestionnaireDokumen3 halamanQuestionnaireUzma KhanamBelum ada peringkat

- Benefit Summary IndiaDokumen5 halamanBenefit Summary IndiaMohd Asim AftabBelum ada peringkat

- Annexure 630430Dokumen3 halamanAnnexure 630430mohammadBelum ada peringkat

- T4032-NL, Payroll Deductions Tables - CPP, EI, and Income Tax Deductions - Newfoundland and LabradorDokumen12 halamanT4032-NL, Payroll Deductions Tables - CPP, EI, and Income Tax Deductions - Newfoundland and LabradorclaokerBelum ada peringkat

- Fringe Benefit FSLGDokumen92 halamanFringe Benefit FSLGkashfrBelum ada peringkat

- Women Factory Employees Facilities As Per Factory ActDokumen25 halamanWomen Factory Employees Facilities As Per Factory ActNaveen Kumar SharmaBelum ada peringkat

- Synise HandbookDokumen60 halamanSynise HandbookrajeshBelum ada peringkat

- Payroll Accounting - Principles of AccountingDokumen7 halamanPayroll Accounting - Principles of AccountingAbdulla MaseehBelum ada peringkat

- Human Resource Management - Critical Review of InterContinental Hotels GroupDokumen7 halamanHuman Resource Management - Critical Review of InterContinental Hotels GroupMaanParrenoVillarBelum ada peringkat

- Manual of Compensation - DBM Chapter 3Dokumen113 halamanManual of Compensation - DBM Chapter 3Aris Solis100% (2)

- AL-QAIRAWAN Chart of AccountsDokumen4 halamanAL-QAIRAWAN Chart of AccountsMohammed Aslam100% (2)

- Letter To Bank On ESOP or ESPPDokumen5 halamanLetter To Bank On ESOP or ESPPAnonymous 3pTM9WCY100% (2)

- The Fringe Benefits Are Categorized As Follows: A) Payment For Time Not Worked: Benefits Under This Category Include: Sick Leave WithDokumen4 halamanThe Fringe Benefits Are Categorized As Follows: A) Payment For Time Not Worked: Benefits Under This Category Include: Sick Leave WithAishwarya NagarathinamBelum ada peringkat

- PC Pindi HRDokumen14 halamanPC Pindi HRAnonymous wam0XGBelum ada peringkat

- Types of EmployeeDokumen2 halamanTypes of EmployeeAlyssa PaularBelum ada peringkat

- Pay Scales For Executives and Non-Executives at RINLDokumen1 halamanPay Scales For Executives and Non-Executives at RINLbanchodaBelum ada peringkat

- Berger ReportDokumen35 halamanBerger ReportShaurav Barua67% (3)

- Employee Benefits India PDFDokumen2 halamanEmployee Benefits India PDFshahidki31100% (1)

- Walsh v. Schlecht, 429 U.S. 401 (1977)Dokumen10 halamanWalsh v. Schlecht, 429 U.S. 401 (1977)Scribd Government DocsBelum ada peringkat

- A Correlational Study Between Benefits Gained and Work Attitude of Espiritu Santo Parochial School TeachersDokumen108 halamanA Correlational Study Between Benefits Gained and Work Attitude of Espiritu Santo Parochial School Teachersathrun zalaBelum ada peringkat

- Howard L. Zimmerman Architects, P.C. 2013 Employee Benefit SummaryDokumen1 halamanHoward L. Zimmerman Architects, P.C. 2013 Employee Benefit SummarynmahanguBelum ada peringkat

- Pueblo County Personnel Manual 2016Dokumen82 halamanPueblo County Personnel Manual 2016Colorado Ethics Watch100% (1)

- Director HR Employee Benefits in Richmond VA Resume Karen SumnerDokumen2 halamanDirector HR Employee Benefits in Richmond VA Resume Karen SumnerKarenSumnerBelum ada peringkat

- BvfomDokumen9 halamanBvfomDhanush KumarBelum ada peringkat