Anda mungkin juga menyukai

- Corporate Financial Analysis with Microsoft ExcelDari EverandCorporate Financial Analysis with Microsoft ExcelPenilaian: 5 dari 5 bintang5/5 (1)

- Investment Analysis - Chapter 3Dokumen34 halamanInvestment Analysis - Chapter 3Linh MaiBelum ada peringkat

- AmalagamationDokumen3 halamanAmalagamationPavan ReddyBelum ada peringkat

- Chapter 6 - Portfolio Evaluation and RevisionDokumen26 halamanChapter 6 - Portfolio Evaluation and RevisionShahrukh ShahjahanBelum ada peringkat

- Chapter Four StockDokumen16 halamanChapter Four Stockሔርሞን ይድነቃቸው100% (1)

- Calculate Terminal Cash FlowDokumen9 halamanCalculate Terminal Cash FlowKazzandraEngallaPaduaBelum ada peringkat

- Fundamental Analysis GuideDokumen12 halamanFundamental Analysis GuidezaryBelum ada peringkat

- Capital Budgeting MethodsDokumen3 halamanCapital Budgeting MethodsRobert RamirezBelum ada peringkat

- Capital Budgeting 1 - 1Dokumen103 halamanCapital Budgeting 1 - 1Subhadeep BasuBelum ada peringkat

- Analyze Capital Structure Using EBIT-EPS AnalysisDokumen3 halamanAnalyze Capital Structure Using EBIT-EPS AnalysisJann KerkyBelum ada peringkat

- Finance Chapter 18Dokumen35 halamanFinance Chapter 18courtdubs100% (1)

- Relative Valuations FINALDokumen44 halamanRelative Valuations FINALChinmay ShirsatBelum ada peringkat

- Homework Chapter 18 and 19Dokumen7 halamanHomework Chapter 18 and 19doejohn150Belum ada peringkat

- Leverage PPTDokumen13 halamanLeverage PPTamdBelum ada peringkat

- Revaluating partnership assets upon dissolutionDokumen32 halamanRevaluating partnership assets upon dissolutionERICK MLINGWABelum ada peringkat

- Financial Evaluation of LEASINGDokumen7 halamanFinancial Evaluation of LEASINGmba departmentBelum ada peringkat

- 05 Fixed Income SecuritiesDokumen55 halaman05 Fixed Income SecuritiessukeshBelum ada peringkat

- Receivable Management KanchanDokumen12 halamanReceivable Management KanchanSanchita NaikBelum ada peringkat

- Principles of Working Capital Management-1Dokumen29 halamanPrinciples of Working Capital Management-1margetBelum ada peringkat

- Chap 5Dokumen52 halamanChap 5jacks ocBelum ada peringkat

- FINMATHS Assignment2Dokumen15 halamanFINMATHS Assignment2Wei Wen100% (1)

- Cost of Capital Lecture Slides in PDF FormatDokumen18 halamanCost of Capital Lecture Slides in PDF FormatLucy UnBelum ada peringkat

- Portfolio Construction Models Risk ReturnDokumen40 halamanPortfolio Construction Models Risk ReturnjitendraBelum ada peringkat

- Formula For Calculation of NET OPERATING CYCLEDokumen9 halamanFormula For Calculation of NET OPERATING CYCLEDevashree GautamBelum ada peringkat

- Cost of Capital PDFDokumen34 halamanCost of Capital PDFMathilda UllyBelum ada peringkat

- Accounting For Specialized Institution Set 2 Scheme of ValuationDokumen19 halamanAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Stock ExchangeDokumen8 halamanStock ExchangeNayan kakiBelum ada peringkat

- Capital Market Clearing and Settlement ProcessDokumen9 halamanCapital Market Clearing and Settlement ProcessTushali TrivediBelum ada peringkat

- Topic 8 - AS 20Dokumen10 halamanTopic 8 - AS 20love chawlaBelum ada peringkat

- Cost of Capital: Concept, Components, Importance, Example, Formula and SignificanceDokumen72 halamanCost of Capital: Concept, Components, Importance, Example, Formula and SignificanceRamya GowdaBelum ada peringkat

- Capital StructureDokumen41 halamanCapital StructuremobinsaiBelum ada peringkat

- Chapter 21 - Insurance Companies and Pension FundsDokumen46 halamanChapter 21 - Insurance Companies and Pension FundsKareen Wellington100% (1)

- IFRS 4 Insurance ContractsDokumen5 halamanIFRS 4 Insurance Contractstikki0219Belum ada peringkat

- Derivatives Markets: Futures, Options & SwapsDokumen20 halamanDerivatives Markets: Futures, Options & SwapsPatrick Earl T. PintacBelum ada peringkat

- LectureDokumen34 halamanLectureSummayya IslamBelum ada peringkat

- H P I S T: IRE Urchase and Nstallment ALE RansactionsDokumen46 halamanH P I S T: IRE Urchase and Nstallment ALE RansactionsJayant MittalBelum ada peringkat

- Introduction To Branch Lecture NotesDokumen3 halamanIntroduction To Branch Lecture Notespladop100% (1)

- Lecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelDokumen34 halamanLecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelL SBelum ada peringkat

- Accounting For LeasesDokumen9 halamanAccounting For LeasesNelson Musili100% (3)

- CH 12. Risk Evaluation in Capital BudgetingDokumen29 halamanCH 12. Risk Evaluation in Capital BudgetingN-aineel DesaiBelum ada peringkat

- Module 3 - Capital BudgetingDokumen1 halamanModule 3 - Capital BudgetingPrincess Frean VillegasBelum ada peringkat

- Chapter 08-Risk and Rates of Return: Cengage Learning Testing, Powered by CogneroDokumen7 halamanChapter 08-Risk and Rates of Return: Cengage Learning Testing, Powered by CogneroqueenbeeastBelum ada peringkat

- Factors Affecting Cost of CapitalDokumen40 halamanFactors Affecting Cost of CapitalKartik AroraBelum ada peringkat

- Likert Scale: Itemized Rating Scale - in The Itemized Rating Scale, The Respondents Are Provided WithDokumen1 halamanLikert Scale: Itemized Rating Scale - in The Itemized Rating Scale, The Respondents Are Provided WithDisha groverBelum ada peringkat

- Chapter Five Inventory Management - Chapter 4Dokumen10 halamanChapter Five Inventory Management - Chapter 4eferemBelum ada peringkat

- FM CH 3Dokumen18 halamanFM CH 3samuel kebedeBelum ada peringkat

- Financial Analyst Interview Questions and AnswersDokumen18 halamanFinancial Analyst Interview Questions and AnswersfitriafiperBelum ada peringkat

- Presentation 2. Understanding The Interest Rates. The Yield To MaturityDokumen30 halamanPresentation 2. Understanding The Interest Rates. The Yield To MaturitySadia SaeedBelum ada peringkat

- Problems SAPMDokumen4 halamanProblems SAPMSneha Swamy100% (1)

- Equity Settled Share Options True/False QuizDokumen4 halamanEquity Settled Share Options True/False QuizCamila AlduezaBelum ada peringkat

- Baumol Miller Orr Cash MGMT Models QDokumen4 halamanBaumol Miller Orr Cash MGMT Models QPrecious Diamond DeeBelum ada peringkat

- Unit 2 Capital StructureDokumen27 halamanUnit 2 Capital StructureNeha RastogiBelum ada peringkat

- Financial Statement Analysis PPT 3427Dokumen25 halamanFinancial Statement Analysis PPT 3427imroz_alamBelum ada peringkat

- Insurance IntermediariesDokumen9 halamanInsurance IntermediariesarmailgmBelum ada peringkat

- Chapter 6 - Time Value of MoneyDokumen7 halamanChapter 6 - Time Value of MoneyJean EliaBelum ada peringkat

- Investment Analysis & Portfolio Management: Equity ValuationDokumen5 halamanInvestment Analysis & Portfolio Management: Equity ValuationNitesh Kirar100% (1)

- FM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Dokumen129 halamanFM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Rohit PanpatilBelum ada peringkat

- 18415compsuggans PCC FM Chapter7Dokumen13 halaman18415compsuggans PCC FM Chapter7Mukunthan RBBelum ada peringkat

- Working Capital ManagementDokumen32 halamanWorking Capital ManagementrutikaBelum ada peringkat

- CH 2 Concept of Return and RiskDokumen48 halamanCH 2 Concept of Return and RiskRanjeet sawBelum ada peringkat

- Project of Amit SinghDokumen80 halamanProject of Amit SinghAmit RoyBelum ada peringkat

- Research Report of Amit SinghDokumen6 halamanResearch Report of Amit SinghAmit RoyBelum ada peringkat

- International RetailingDokumen17 halamanInternational RetailingAmit RoyBelum ada peringkat

- Women EntrepreneurshipDokumen13 halamanWomen EntrepreneurshipAwesh BhornyaBelum ada peringkat

- My Research Report For MBA CompletionDokumen70 halamanMy Research Report For MBA CompletionAmit RoyBelum ada peringkat

- RetailDokumen25 halamanRetailjayesh78149062100% (2)

- Plastic Money: By: Sunaina Verma Shashikant Mohd. Zeeshan Shashank TripathiDokumen25 halamanPlastic Money: By: Sunaina Verma Shashikant Mohd. Zeeshan Shashank Tripathitarunavasyani100% (3)

- Bank ManagementDokumen112 halamanBank Managementsat237Belum ada peringkat

- Some Important Notes About Indian NBFCsDokumen9 halamanSome Important Notes About Indian NBFCsysrlahariBelum ada peringkat

- Mutual FundsDokumen17 halamanMutual FundsAmit RoyBelum ada peringkat

- Policy Support To Small ScaleDokumen19 halamanPolicy Support To Small ScalePrasad YadavBelum ada peringkat

- Woman Enteprship Promotion in IndiaDokumen38 halamanWoman Enteprship Promotion in IndiaAmit RoyBelum ada peringkat

- International RetailingDokumen49 halamanInternational RetailingAmit RoyBelum ada peringkat

- International RetailingDokumen17 halamanInternational RetailingAmit RoyBelum ada peringkat

- Section 80 CDokumen5 halamanSection 80 CAmit RoyBelum ada peringkat

- Income From SalaryDokumen14 halamanIncome From SalaryAmit RoyBelum ada peringkat

- Basic Definitions of TaxationDokumen4 halamanBasic Definitions of TaxationAmit RoyBelum ada peringkat

- Section 10aDokumen4 halamanSection 10aAmit RoyBelum ada peringkat

- Basics of TaxationDokumen7 halamanBasics of TaxationAmit RoyBelum ada peringkat

- Set Off and Carry ForwardDokumen4 halamanSet Off and Carry ForwardAmit Roy100% (1)

- Assets Liabilities ManagmentDokumen15 halamanAssets Liabilities Managmentpriyank shah100% (1)

- 4 - Capital Gain IDokumen16 halaman4 - Capital Gain IAmit RoyBelum ada peringkat

- ForecastingDokumen48 halamanForecastingAmit RoyBelum ada peringkat

- Residential StatusDokumen4 halamanResidential StatusAmit RoyBelum ada peringkat

- International RetailingDokumen17 halamanInternational RetailingAmit RoyBelum ada peringkat

- Unit I Supplementary Info Investment AvenuesDokumen17 halamanUnit I Supplementary Info Investment AvenuesAmit RoyBelum ada peringkat

- Income From House Property TaxationDokumen3 halamanIncome From House Property TaxationAmit Roy100% (1)

- Job Analysis-Based Performance Appraisals: Dale J. Dwyer, PH.DDokumen13 halamanJob Analysis-Based Performance Appraisals: Dale J. Dwyer, PH.DAmit RoyBelum ada peringkat

- IHRM-Labour & IRDokumen20 halamanIHRM-Labour & IRapi-3771917100% (4)

- Fdi in IndiaDokumen19 halamanFdi in IndiaSatish AddaBelum ada peringkat

- AC3202 WK2 Exercises SolutionsDokumen11 halamanAC3202 WK2 Exercises SolutionsLong LongBelum ada peringkat

- What It Takes To Make 1 Million Dollars A YearDokumen5 halamanWhat It Takes To Make 1 Million Dollars A YearBary SheenBelum ada peringkat

- Comparative Study On Ulips in The Indian Insurance Market For Tata Aig Life by Delnaaz ParvezDokumen71 halamanComparative Study On Ulips in The Indian Insurance Market For Tata Aig Life by Delnaaz Parveznarayanamohan0% (2)

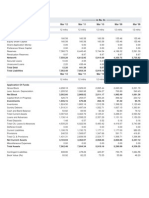

- Balance Sheet and P&L of CiplaDokumen2 halamanBalance Sheet and P&L of CiplaPratik AhluwaliaBelum ada peringkat

- NBL NewDokumen110 halamanNBL NewDeepak JhaBelum ada peringkat

- Project Report On Hardware Shop For Riyaz Hardware: ConfidentialDokumen5 halamanProject Report On Hardware Shop For Riyaz Hardware: ConfidentialRafikul IslamBelum ada peringkat

- Far - First Preboard QuestionnaireDokumen14 halamanFar - First Preboard QuestionnairewithyouidkBelum ada peringkat

- Nvs Brokerage Pvt. LTD.: 702, Embassy Centre, Nariman Point, Mumbai - 400 021. Tel.: 61539100 Fax: 61539134 E MailDokumen3 halamanNvs Brokerage Pvt. LTD.: 702, Embassy Centre, Nariman Point, Mumbai - 400 021. Tel.: 61539100 Fax: 61539134 E MailMLastTryBelum ada peringkat

- Money Banking MGT 411 LecturesDokumen148 halamanMoney Banking MGT 411 LecturesshazadBelum ada peringkat

- ESENECO (5) Capital FinancingDokumen23 halamanESENECO (5) Capital FinancingTobias FateBelum ada peringkat

- IFRS 9 Part IV Hedging November 2015Dokumen28 halamanIFRS 9 Part IV Hedging November 2015Nicolaus CopernicusBelum ada peringkat

- Banyan Tree Holdings RestructuringDokumen18 halamanBanyan Tree Holdings RestructuringdfghfiBelum ada peringkat

- Math 118 - Supplement Problems (Rev 2017F) PDFDokumen43 halamanMath 118 - Supplement Problems (Rev 2017F) PDFMaitri BarotBelum ada peringkat

- Problem Set 2 Term StructureDokumen3 halamanProblem Set 2 Term StructureIsyBelum ada peringkat

- Assignment - 2 Cash Flow Analysis: Submitted by Group - 8Dokumen13 halamanAssignment - 2 Cash Flow Analysis: Submitted by Group - 8dheeraj_rai005Belum ada peringkat

- WSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0Dokumen2 halamanWSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0jason.sevin02Belum ada peringkat

- Solution To AssignmentDokumen29 halamanSolution To AssignmentMai Lan AnhBelum ada peringkat

- G. Mannarino - Ultimate Guide To Money and The MarketsDokumen197 halamanG. Mannarino - Ultimate Guide To Money and The MarketsD.C.75% (4)

- Bu SyllabusDokumen5 halamanBu Syllabuswaleed20_20Belum ada peringkat

- Profile On The Production of Synthetic Marble EthiopiaDokumen29 halamanProfile On The Production of Synthetic Marble EthiopiaNasra HusseinBelum ada peringkat

- WEF Alternative Investments 2020 FutureDokumen59 halamanWEF Alternative Investments 2020 FutureOwenBelum ada peringkat

- Indiabulls ThesisDokumen5 halamanIndiabulls Thesisdivyanshu kumarBelum ada peringkat

- High Probability Trading Setups For The Currency Market PDFDokumen100 halamanHigh Probability Trading Setups For The Currency Market PDFDavid VenancioBelum ada peringkat

- Managerial Economics Financial Analysis June July 2022Dokumen8 halamanManagerial Economics Financial Analysis June July 2022Ashwik YadavBelum ada peringkat

- Comparative Analysis of Broking FirmsDokumen12 halamanComparative Analysis of Broking FirmsJames RamirezBelum ada peringkat

- Mechanics of Futures Markets ExplainedDokumen23 halamanMechanics of Futures Markets ExplainedaliBelum ada peringkat

- Financial InstitutionDokumen3 halamanFinancial InstitutionMuhammad Saleem Sattar100% (1)

- 10 Years of Growth and InnovationDokumen194 halaman10 Years of Growth and Innovationram binod yadavBelum ada peringkat

- MSCI All Country World Investable Market Index (ACWI IMI)Dokumen2 halamanMSCI All Country World Investable Market Index (ACWI IMI)Alex LinBelum ada peringkat

- Cfa Level III Errata PDFDokumen7 halamanCfa Level III Errata PDFTran HongBelum ada peringkat