Anda mungkin juga menyukai

- Jurnal Dalam Kombinasi BisnisDokumen6 halamanJurnal Dalam Kombinasi BisnisDelastri ParddBelum ada peringkat

- Akuntansi Sektor Publik Tidak Dapat Dikatakan Sebagai Akuntansi PemerintahanDokumen9 halamanAkuntansi Sektor Publik Tidak Dapat Dikatakan Sebagai Akuntansi PemerintahanAnisatul Fitri100% (1)

- L4 8,9,10,12,14Dokumen9 halamanL4 8,9,10,12,14Susi LowatiBelum ada peringkat

- Tugas 1 AK FIXDokumen4 halamanTugas 1 AK FIXabdul ridho100% (1)

- Tugas Akl2 (L-3-8-L3-10)Dokumen3 halamanTugas Akl2 (L-3-8-L3-10)Susi Lowati100% (1)

- Akl Bab 3 4Dokumen3 halamanAkl Bab 3 4Tydac100% (4)

- Soal Arus Kas (LSG+TDK LSG)Dokumen3 halamanSoal Arus Kas (LSG+TDK LSG)Yoyo SupraptoBelum ada peringkat

- Akuntansi Keuangan Lanjutan D3 Soal-Soal PDFDokumen6 halamanAkuntansi Keuangan Lanjutan D3 Soal-Soal PDFSafira PutriBelum ada peringkat

- Soal UAS AKL2Dokumen2 halamanSoal UAS AKL2lia indahBelum ada peringkat

- 132818280620soal UAS AKL 2Dokumen2 halaman132818280620soal UAS AKL 2Novi Satria DewiBelum ada peringkat

- Soal Latihan AKL Kls 5.2Dokumen1 halamanSoal Latihan AKL Kls 5.2Violet RistaBelum ada peringkat

- AKT Lanjutan 2Dokumen4 halamanAKT Lanjutan 2Habib Al AzizBelum ada peringkat

- Praktikum SMT 6 (Kombinasi Bisnis)Dokumen2 halamanPraktikum SMT 6 (Kombinasi Bisnis)YanBelum ada peringkat

- Latihan Soal Bab 1&2Dokumen3 halamanLatihan Soal Bab 1&2Yuni Annisah AriefBelum ada peringkat

- Akl 2 - Arindah Failisa Putri PDFDokumen2 halamanAkl 2 - Arindah Failisa Putri PDFMrdyna DynBelum ada peringkat

- Soal Presentasi Dan PR Individu AKL1Dokumen6 halamanSoal Presentasi Dan PR Individu AKL1Yusuf MaBelum ada peringkat

- Tugas Aklan Pert.15 - Muhammad Fauzan Amru (205020050)Dokumen10 halamanTugas Aklan Pert.15 - Muhammad Fauzan Amru (205020050)Muhammad FauzanBelum ada peringkat

- Pert15 Ulasan Materi AKLAN - Frida Bilqis (205020065)Dokumen10 halamanPert15 Ulasan Materi AKLAN - Frida Bilqis (205020065)Juned KamalBelum ada peringkat

- Latian Soal Kelompok 10Dokumen6 halamanLatian Soal Kelompok 10Devi Yulia PangestutiBelum ada peringkat

- Post Test Pertemuan 3Dokumen1 halamanPost Test Pertemuan 3SnoopyJackBelum ada peringkat

- AKL - KLP 4 - Kls DDokumen15 halamanAKL - KLP 4 - Kls DDwi RaraBelum ada peringkat

- Soal Latihan Business Combination Consolidation (A+b C)Dokumen2 halamanSoal Latihan Business Combination Consolidation (A+b C)dian artha intanBelum ada peringkat

- Latihan Soal Bab 1 Penggabungan Usaha AKL 1Dokumen6 halamanLatihan Soal Bab 1 Penggabungan Usaha AKL 1Baskoro ayeBelum ada peringkat

- Muhammad Bayu Aji 1805046011 Tugas AKLDokumen7 halamanMuhammad Bayu Aji 1805046011 Tugas AKLjaka sarwanaBelum ada peringkat

- LSP 5 - Laporan Keuangan Konsolidasi - Bagian 2Dokumen24 halamanLSP 5 - Laporan Keuangan Konsolidasi - Bagian 2Adel AdelBelum ada peringkat

- Tugas Akl 1.1 (Hal 26)Dokumen4 halamanTugas Akl 1.1 (Hal 26)mohamadirgi897Belum ada peringkat

- Contoh Kasus Entitas Konsolidasi Dan Laporan Keuangan KonsolidasiDokumen9 halamanContoh Kasus Entitas Konsolidasi Dan Laporan Keuangan KonsolidasiRike AgustinaBelum ada peringkat

- Investasi Di Perusahaan Anak Dan AsosiasiDokumen8 halamanInvestasi Di Perusahaan Anak Dan AsosiasiwarsidiBelum ada peringkat

- UTS Akt Keuangan Lanjutan - 2 - (Reza - Fransiska - 1834030139)Dokumen5 halamanUTS Akt Keuangan Lanjutan - 2 - (Reza - Fransiska - 1834030139)Reska SafitriBelum ada peringkat

- Tugas Akuntansi Lanjutan Pert Terakhir Mayang MutiaraDokumen10 halamanTugas Akuntansi Lanjutan Pert Terakhir Mayang Mutiaramayang mutiaraBelum ada peringkat

- Konsolidasi Pada Anak Perusahaan Yang Dimiliki Kurang Dari Kepemilikan PenuhDokumen13 halamanKonsolidasi Pada Anak Perusahaan Yang Dimiliki Kurang Dari Kepemilikan PenuhFarida Yunia LestariBelum ada peringkat

- Laporan Keuangan Konsolidasi Dengan Tingkat Kepemilikan Kurang Dari 100 % ( (Acquired at More Than Book Value) )Dokumen24 halamanLaporan Keuangan Konsolidasi Dengan Tingkat Kepemilikan Kurang Dari 100 % ( (Acquired at More Than Book Value) )Rima Amelia PutriBelum ada peringkat

- Tugas 1 Akuntansi Keuangan Lanjutan 2Dokumen7 halamanTugas 1 Akuntansi Keuangan Lanjutan 2arif100% (1)

- Bab 4 L4-8, L4-9Dokumen4 halamanBab 4 L4-8, L4-9Lawren RajagukgukBelum ada peringkat

- Soal Mid Keuangan 1 22-23 PagiDokumen2 halamanSoal Mid Keuangan 1 22-23 PagiArjuna PutraBelum ada peringkat

- Soal UasDokumen2 halamanSoal Uasyori masyitahBelum ada peringkat

- Tugas EA4138 13 065832Dokumen19 halamanTugas EA4138 13 065832Serin Febiyantari50% (2)

- Ega Aprilia Nugroho - Kuis Akl 2 - 18133100123Dokumen3 halamanEga Aprilia Nugroho - Kuis Akl 2 - 18133100123EgaapBelum ada peringkat

- Tugas TerroosssssDokumen4 halamanTugas TerroosssssGoftha Gene HernandeztBelum ada peringkat

- Wisnu Haji, 1701035098Dokumen3 halamanWisnu Haji, 1701035098WisnuhajiBelum ada peringkat

- Soal Latihan Laporan SPDDokumen3 halamanSoal Latihan Laporan SPDWinda SuciningsihBelum ada peringkat

- 751 - Latihan Soal Uas Akuntansi Keuangan 2Dokumen3 halaman751 - Latihan Soal Uas Akuntansi Keuangan 2SelvianaBelum ada peringkat

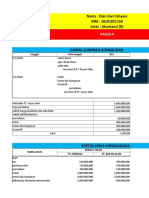

- Kasus 4 - Dian Dwi Cahyani - 18101021150Dokumen4 halamanKasus 4 - Dian Dwi Cahyani - 18101021150Dian DchBelum ada peringkat

- Advance Accounting - Business CombinationDokumen3 halamanAdvance Accounting - Business Combinationricky Ok100% (1)

- Quiz Pra Uts Akeu-1Dokumen3 halamanQuiz Pra Uts Akeu-1Anisa Siti WahyuniBelum ada peringkat

- Bagi SOAL UAS AKL 2 (6 Juli 2021)Dokumen6 halamanBagi SOAL UAS AKL 2 (6 Juli 2021)Lili TahraBelum ada peringkat

- Akuntansi Keuangan Lanjutan 1 Materi 5Dokumen15 halamanAkuntansi Keuangan Lanjutan 1 Materi 5RiskaNovitasariBelum ada peringkat

- Soal Uas AklDokumen3 halamanSoal Uas AklardaBelum ada peringkat

- Quiz Pra UtsDokumen2 halamanQuiz Pra UtsEmmanuella GrachiaBelum ada peringkat

- Naskah Eksi4204 Tugas2Dokumen3 halamanNaskah Eksi4204 Tugas2Alfredo Victor SimanungkalitBelum ada peringkat

- UahajajajwDokumen3 halamanUahajajajwMeyling NatasiaBelum ada peringkat

- Laporan Laba Rugi KonsolidasiDokumen4 halamanLaporan Laba Rugi Konsolidasiakmi ruskanBelum ada peringkat

- Abet Alfarizi - 21901082117-AKL II - A2 - Tugas Laporan KonsolidasiDokumen3 halamanAbet Alfarizi - 21901082117-AKL II - A2 - Tugas Laporan KonsolidasiDian WiddyastutikBelum ada peringkat

- AKL Bab04Dokumen24 halamanAKL Bab04syarah lutfa aliyaBelum ada peringkat

- SoalDokumen6 halamanSoalAfandyBelum ada peringkat

- 25 .9.22 Soal TUGAS 1 Akuntansi Keuangan Lanjuatan 1Dokumen2 halaman25 .9.22 Soal TUGAS 1 Akuntansi Keuangan Lanjuatan 1Najmi LailiBelum ada peringkat

- Tugas 1Dokumen5 halamanTugas 1ega suastanaBelum ada peringkat

- 4Dokumen2 halaman4Anisatul FitriBelum ada peringkat

- A. Definisi Kebijakan MoneterDokumen2 halamanA. Definisi Kebijakan MoneterAnisatul FitriBelum ada peringkat

- 5Dokumen2 halaman5Anisatul FitriBelum ada peringkat

- Pembagian Sistem PerekonomianDokumen3 halamanPembagian Sistem PerekonomianAnisatul FitriBelum ada peringkat

- ASP UAS II 1920 ExtDokumen2 halamanASP UAS II 1920 ExtAnisatul FitriBelum ada peringkat

- Anisatul - Fitri (190522076)Dokumen5 halamanAnisatul - Fitri (190522076)Anisatul FitriBelum ada peringkat

- ANISATUL FITRI Tugas AKL IIDokumen3 halamanANISATUL FITRI Tugas AKL IIAnisatul FitriBelum ada peringkat

- Silabus Lab. Aplikasi Komputer Akuntansi IDokumen1 halamanSilabus Lab. Aplikasi Komputer Akuntansi IAnisatul FitriBelum ada peringkat

- Anisatul FitriDokumen1 halamanAnisatul FitriAnisatul FitriBelum ada peringkat

- Materi 08 AKS DikonversiDokumen26 halamanMateri 08 AKS DikonversiAnisatul FitriBelum ada peringkat