Anda mungkin juga menyukai

- DATA Update 070821Dokumen5 halamanDATA Update 070821Registrasi MesinBelum ada peringkat

- Morning - Update 20220801Dokumen4 halamanMorning - Update 20220801Kharisma Al Qua RisbiBelum ada peringkat

- Morning - Update 20220728Dokumen5 halamanMorning - Update 20220728Dini FadhilahBelum ada peringkat

- Kertas Kerja Unit Kompetensi Menganalisis Efek UpdatedDokumen4 halamanKertas Kerja Unit Kompetensi Menganalisis Efek UpdatedelvinlaurenziaBelum ada peringkat

- BRSbrsInd 20230206114637 15Dokumen1 halamanBRSbrsInd 20230206114637 15HananBelum ada peringkat

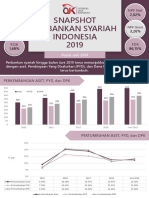

- Snapshot Perbankan Syariah Indonesia Maret 2020 PDFDokumen6 halamanSnapshot Perbankan Syariah Indonesia Maret 2020 PDFWindi AtrianiBelum ada peringkat

- Morning - Update 20230616Dokumen4 halamanMorning - Update 20230616Flx gadgetinBelum ada peringkat

- Progres YPI S8 Sep21 Capaian Dan ProgramDokumen33 halamanProgres YPI S8 Sep21 Capaian Dan ProgramYuyun YuniBelum ada peringkat

- ACTFSTS - Factsheet Trimegah Dana Tetap SyariahDokumen2 halamanACTFSTS - Factsheet Trimegah Dana Tetap SyariahRobertCallaghanBelum ada peringkat

- Grafik (Repaired)Dokumen12 halamanGrafik (Repaired)ratna suminarBelum ada peringkat

- Snapshot Perbankan Syariah 2017Dokumen8 halamanSnapshot Perbankan Syariah 2017Farizal HammiBelum ada peringkat

- Masa Depan Ekonomi SyariahDokumen19 halamanMasa Depan Ekonomi SyariahRafe AlryadiBelum ada peringkat

- ANALISA MOM Dan YOYDokumen15 halamanANALISA MOM Dan YOYFahrudin SuhadakBelum ada peringkat

- Kontan Harian Edisi 17-06-2019Dokumen20 halamanKontan Harian Edisi 17-06-2019Vita OktaviaBelum ada peringkat

- IDN - Financial - BBNI - 2Q23 - In-Line, Better 2H23 OutlookDokumen3 halamanIDN - Financial - BBNI - 2Q23 - In-Line, Better 2H23 OutlookBilclinton SaragihBelum ada peringkat

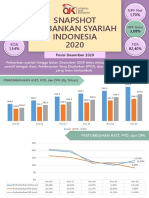

- Snapshot Perbankan Syariah Desember 2020Dokumen6 halamanSnapshot Perbankan Syariah Desember 2020Ina NofrianaBelum ada peringkat

- Rakerwil BRI BRINS Lampung TayangDokumen8 halamanRakerwil BRI BRINS Lampung TayangDafit YohendraBelum ada peringkat

- 2 Materi Ibu Indah IramadhiniDokumen36 halaman2 Materi Ibu Indah IramadhiniAbd RahmanBelum ada peringkat

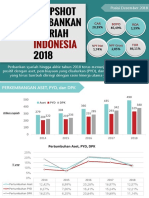

- Snapshot Perbankan Syariah Posisi Desember 2018 - 2Dokumen8 halamanSnapshot Perbankan Syariah Posisi Desember 2018 - 2Cici Aprilia KartiniBelum ada peringkat

- SAHAMDokumen13 halamanSAHAMRatna NisaaBelum ada peringkat

- Lampiran BAB V PerbaikanDokumen14 halamanLampiran BAB V PerbaikanFitBelum ada peringkat

- Analisis Vertikal Dan HorizontalDokumen15 halamanAnalisis Vertikal Dan HorizontalRick BastianBelum ada peringkat

- Analisis Vertikal Dan HorizontalDokumen15 halamanAnalisis Vertikal Dan HorizontalRick BastianBelum ada peringkat

- Proyeksi Ekonomi Pemilu INDEFDokumen23 halamanProyeksi Ekonomi Pemilu INDEFAbimanyu LearingBelum ada peringkat

- Snapshot Juni 2018 (Final)Dokumen9 halamanSnapshot Juni 2018 (Final)Andra SomodungBelum ada peringkat

- Senin, 7 Agustus 2023Dokumen21 halamanSenin, 7 Agustus 2023belajar lagiBelum ada peringkat

- I-Daily 21 November 2023Dokumen2 halamanI-Daily 21 November 2023Muhammad Rajib RakatirtaBelum ada peringkat

- 2.2.b. Risiko Pasar IRRDokumen14 halaman2.2.b. Risiko Pasar IRRantonhpmBelum ada peringkat

- Berita Resmi Statistik BPS Jateng September 2022Dokumen42 halamanBerita Resmi Statistik BPS Jateng September 2022Dzaky MuhammadBelum ada peringkat

- 14.erna Pitria Sari - 213403416064Dokumen5 halaman14.erna Pitria Sari - 213403416064ernapitria261Belum ada peringkat

- Bank Indonesia - FESDokumen21 halamanBank Indonesia - FESsitti marhamahBelum ada peringkat

- Laporan DistribusiDokumen11 halamanLaporan DistribusiXDFunINDOBelum ada peringkat

- UTS SazaliaQN B133200125Dokumen3 halamanUTS SazaliaQN B133200125Andre DwixBelum ada peringkat

- Tugas 1 Manajemen Keuangan Tri Margono 868Dokumen9 halamanTugas 1 Manajemen Keuangan Tri Margono 868fitria.dwipurnomoBelum ada peringkat

- REALISASIDokumen6 halamanREALISASILikBelum ada peringkat

- Snapshot Perbankan Syariah Juni 2019Dokumen8 halamanSnapshot Perbankan Syariah Juni 2019Rifki Maulana100% (1)

- CAPMDokumen9 halamanCAPMRestyka PuspitaBelum ada peringkat

- Materi Disbudpar Jatim 230223 - DodikDokumen26 halamanMateri Disbudpar Jatim 230223 - DodikAndre WibisonoBelum ada peringkat

- Daily Insight 16162023Dokumen8 halamanDaily Insight 16162023Muhamad Lukman HakimBelum ada peringkat

- Capaian Program Lansia 2023-2024Dokumen8 halamanCapaian Program Lansia 2023-2024meisyah winandaBelum ada peringkat

- Morning - Update 20220708Dokumen4 halamanMorning - Update 20220708ShenShen WidartoBelum ada peringkat

- Bahan Rapat Sept 2022 - Pengajuan SMKN 51 - PenguranganDokumen1 halamanBahan Rapat Sept 2022 - Pengajuan SMKN 51 - PenguranganGuru CreativeBelum ada peringkat

- Reksa Dana Cipta Saham Unggulan: Laporan Kinerja Bulanan Reksa Dana Haji Syariah (I-Hajj)Dokumen1 halamanReksa Dana Cipta Saham Unggulan: Laporan Kinerja Bulanan Reksa Dana Haji Syariah (I-Hajj)muhammad arroyanBelum ada peringkat

- Pernikahan CampuranDokumen4 halamanPernikahan CampuranAbcde FghijkBelum ada peringkat

- Analisis Clinical PathwayDokumen2 halamanAnalisis Clinical PathwayupiBelum ada peringkat

- Economic Outlook - BCI ASIA-FinalDokumen22 halamanEconomic Outlook - BCI ASIA-FinalasanBelum ada peringkat

- Pt. Perusahaan Gas Negara TBK (Kelompok 3)Dokumen18 halamanPt. Perusahaan Gas Negara TBK (Kelompok 3)Teddy RendraBelum ada peringkat

- Tinjauan KeuanganDokumen18 halamanTinjauan KeuanganYustiadi WahyudiBelum ada peringkat

- 09 Permintaan Dan Penawaran AgregatDokumen20 halaman09 Permintaan Dan Penawaran Agregatpatma asyatariBelum ada peringkat

- Victorianovember 2022Dokumen1 halamanVictorianovember 2022Dhanik JayantiBelum ada peringkat

- X Tra Fixed Rate MLD Periodic Performance Report 1Dokumen12 halamanX Tra Fixed Rate MLD Periodic Performance Report 1zetroxriddleBelum ada peringkat

- DATA Update 090321Dokumen9 halamanDATA Update 090321Registrasi MesinBelum ada peringkat

- Simas Saham Unggulan Factsheet PDFDokumen1 halamanSimas Saham Unggulan Factsheet PDFgreen beeBelum ada peringkat

- Pagu JKNDokumen3 halamanPagu JKNpuskesmas loloBelum ada peringkat

- Infografis Umum RDGB FEBRUARI 2023Dokumen1 halamanInfografis Umum RDGB FEBRUARI 2023faradhinaaaBelum ada peringkat

- BAB VIII Indikator Kinerja Penyelenggaraan Pemerintahan Daerah - KLARIFIKASI 1 FEB 2018Dokumen5 halamanBAB VIII Indikator Kinerja Penyelenggaraan Pemerintahan Daerah - KLARIFIKASI 1 FEB 2018taufik kasimBelum ada peringkat