Anda mungkin juga menyukai

- CONTOH DRAFT PKWT PT - IBB (JNE - DEPOK)Dokumen3 halamanCONTOH DRAFT PKWT PT - IBB (JNE - DEPOK)Muhammad ArdyBelum ada peringkat

- Perencanaan TagihanDokumen13 halamanPerencanaan TagihanMuhammad Faris AbdillahBelum ada peringkat

- 1673249635soal Latihan Akuntansi Pajak Angkt 84Dokumen10 halaman1673249635soal Latihan Akuntansi Pajak Angkt 84emi mamamaBelum ada peringkat

- Besaran Manfaat Dan Batasan Upah Tertinggi Jaminan Pensiun Tahun 2023Dokumen2 halamanBesaran Manfaat Dan Batasan Upah Tertinggi Jaminan Pensiun Tahun 2023sanata personalia100% (1)

- Ujian Tax Center Unpad KUPDokumen3 halamanUjian Tax Center Unpad KUPRasqi ArfakhsyadzBelum ada peringkat

- Bni Wirausaha FixDokumen8 halamanBni Wirausaha FixJuly Dwijayanti DaeliBelum ada peringkat

- Daftar Inventaris Yang Tersedia Dalam RumahDokumen3 halamanDaftar Inventaris Yang Tersedia Dalam RumahsemuhennaBelum ada peringkat

- Akuntansi Imbalan KerjaDokumen30 halamanAkuntansi Imbalan KerjadinahBelum ada peringkat

- Contoh Voucher Kas MasukDokumen1 halamanContoh Voucher Kas MasukanisaBelum ada peringkat

- Contoh Likuidasi PerseoranDokumen9 halamanContoh Likuidasi PerseorandarmayantiBelum ada peringkat

- PKS PT TokopediaDokumen12 halamanPKS PT TokopediaAmat EnjjoyBelum ada peringkat

- Surat Perjanjian KerjaDokumen4 halamanSurat Perjanjian KerjaHafiza Eka putriBelum ada peringkat

- Surat Kuasa Potong Gaji PegawaiDokumen2 halamanSurat Kuasa Potong Gaji PegawaiPribadi KurniawanBelum ada peringkat

- S-160-PJ.42-2003 - Premi JPK - DEDokumen2 halamanS-160-PJ.42-2003 - Premi JPK - DESiti ChoirunnisaBelum ada peringkat

- Surat EdaranDokumen7 halamanSurat EdaranArmiya YMBelum ada peringkat

- SPTPD RestaurantDokumen3 halamanSPTPD RestaurantJasmine ZahraBelum ada peringkat

- Surat KuasaDokumen1 halamanSurat KuasaWidya Widia AstutiBelum ada peringkat

- Format Berita Acara Penyisihan PiutangDokumen1 halamanFormat Berita Acara Penyisihan PiutangShenna Dea Ananda PutriBelum ada peringkat

- PerjanjianDokumen16 halamanPerjanjianryan anggerekaBelum ada peringkat

- Sistem Mysap To TaxDokumen15 halamanSistem Mysap To TaxrizkyBelum ada peringkat

- User Manual - Dumtk SippDokumen49 halamanUser Manual - Dumtk SippernasukseskaryahutaniBelum ada peringkat

- Memo Pembagian Tugas KaryawanDokumen3 halamanMemo Pembagian Tugas KaryawanBening SkincareBelum ada peringkat

- Summary Perbedaan Perjanjian Kemitraan Dengan Perjanjian KerjaDokumen1 halamanSummary Perbedaan Perjanjian Kemitraan Dengan Perjanjian Kerjaandreas sipayungBelum ada peringkat

- PPN Faktur 040Dokumen2 halamanPPN Faktur 040Rangga Soeandhika100% (1)

- Contoh Surat Pernyataan Blokir DepositoDokumen1 halamanContoh Surat Pernyataan Blokir DepositodiniratnakBelum ada peringkat

- PT Minera BhaktiDokumen3 halamanPT Minera BhaktiAida Juliyani RahmaBelum ada peringkat

- Surat Tugas-Audit TemplateDokumen1 halamanSurat Tugas-Audit Templatetri_sumardionoBelum ada peringkat

- Peraturan PerusahaanDokumen25 halamanPeraturan PerusahaanFahmi HamsyahBelum ada peringkat

- PDF Contoh Kontrak Konsultan Dengan PerusahaanDokumen6 halamanPDF Contoh Kontrak Konsultan Dengan PerusahaanAgung BachtiarBelum ada peringkat

- Surat Jual BeliDokumen4 halamanSurat Jual BeliCicik Sriwulan50% (2)

- Format Surat Tanggapan Atas Surat PemberitahuanDokumen6 halamanFormat Surat Tanggapan Atas Surat PemberitahuanAjen Yoga PradhanaBelum ada peringkat

- Contoh Surat Berita Acara ITDokumen1 halamanContoh Surat Berita Acara ITIchsan PratamaBelum ada peringkat

- MCM Lite Syarat Dan Ketentuan Umum Mandiri Cash Management LiteDokumen3 halamanMCM Lite Syarat Dan Ketentuan Umum Mandiri Cash Management Liteisan100% (1)

- Format Surat Permohonan RekananDokumen2 halamanFormat Surat Permohonan RekananAl Maliki Abu RifatkhaBelum ada peringkat

- Ank GaransiDokumen145 halamanAnk GaransiRoy Flo100% (1)

- Surat Pernyataan Tidak Pernah Diberhentikan Dengan Tidak Hormat SebagaiDokumen1 halamanSurat Pernyataan Tidak Pernah Diberhentikan Dengan Tidak Hormat SebagaiEki AfrilianBelum ada peringkat

- Tax Dispute and LitigationDokumen15 halamanTax Dispute and LitigationOktavio Reza Putra100% (1)

- Surat Permohonan Koreksi - Amend MT 199 SIMODISDokumen1 halamanSurat Permohonan Koreksi - Amend MT 199 SIMODISWellyBelum ada peringkat

- B 70 022023 Batasan Upah Dan Manfaat JP 2023Dokumen2 halamanB 70 022023 Batasan Upah Dan Manfaat JP 2023mimbo brahmantikoBelum ada peringkat

- Pedoman Perilaku AFPI 2020Dokumen19 halamanPedoman Perilaku AFPI 2020Hana Sungkar50% (2)

- Notulen Dekom Triwulan IVDokumen10 halamanNotulen Dekom Triwulan IVRuly PangajouwBelum ada peringkat

- Surat Pernyataan Pemberian Informasi Kepada Pelanggan (Change Card Request)Dokumen1 halamanSurat Pernyataan Pemberian Informasi Kepada Pelanggan (Change Card Request)Rico SeptianBelum ada peringkat

- 8 Ruang Lingkup Dan Skema AuditDokumen1 halaman8 Ruang Lingkup Dan Skema AuditDwiki Muhammad GifaryBelum ada peringkat

- Tes Excel BCADokumen5 halamanTes Excel BCAAndre SantosBelum ada peringkat

- SE DJP 22-1990 - Penulisan RupiahDokumen1 halamanSE DJP 22-1990 - Penulisan RupiahHutapea_apynBelum ada peringkat

- Kontrak Kerjasama SinarmasDokumen8 halamanKontrak Kerjasama SinarmasAlam NugrahaBelum ada peringkat

- Bab III Coba2Dokumen42 halamanBab III Coba2Fais Al RahmanBelum ada peringkat

- Modul 5 Pajak InternasionalDokumen11 halamanModul 5 Pajak Internasionalfajri saniBelum ada peringkat

- Surat Penyitaan BarangDokumen1 halamanSurat Penyitaan BarangPangihutan HutaurukBelum ada peringkat

- Tax PlanningDokumen10 halamanTax PlanningAli PurnomoBelum ada peringkat

- Pembayaran Iuran Jamsostek Melalui Virtual AccountDokumen22 halamanPembayaran Iuran Jamsostek Melalui Virtual Accountsigitp88Belum ada peringkat

- Tata Cara Restitusi PPNDokumen9 halamanTata Cara Restitusi PPNNurafniBiyantari100% (1)

- Rekening PerantaraDokumen3 halamanRekening PerantarayuliaBelum ada peringkat

- SPK Padma Lalita NewDokumen8 halamanSPK Padma Lalita New2017013030 AndikaBelum ada peringkat

- Monitoring SP2D ReturDokumen1 halamanMonitoring SP2D ReturayikkuBelum ada peringkat

- SOP PenggajianDokumen1 halamanSOP PenggajianIhsan AnandaBelum ada peringkat

- MSDM Etraining Kelas Siap Jadi HR Staff - Dasar Pengupahan 2022Dokumen51 halamanMSDM Etraining Kelas Siap Jadi HR Staff - Dasar Pengupahan 2022Rizky Dwi PriyandokoBelum ada peringkat

- Kisi Kisi Uas Perpajakan Kelas GDokumen3 halamanKisi Kisi Uas Perpajakan Kelas GREG.A/41921100002/DESI INDRIYANTIBelum ada peringkat

- TBS - Laporan Keuangan 30 September 2022 PDFDokumen204 halamanTBS - Laporan Keuangan 30 September 2022 PDFaspihaniBelum ada peringkat

- Cara Instal Aplikasi SIBAKU DAN PENGGUNAANNYADokumen38 halamanCara Instal Aplikasi SIBAKU DAN PENGGUNAANNYASastro CahyoBelum ada peringkat

- Songs of BatakDokumen1 halamanSongs of Batakabdiel welmavenBelum ada peringkat

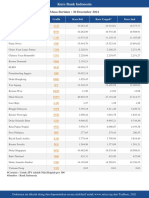

- Masa Berlaku: 30 Desember 2021: Mata Uang Grafik Kurs Beli Kurs Tengah Kurs JualDokumen2 halamanMasa Berlaku: 30 Desember 2021: Mata Uang Grafik Kurs Beli Kurs Tengah Kurs JualTirany Aprilia StephanieBelum ada peringkat

- Kementerian Keuangan Republik IndonesiaDokumen1 halamanKementerian Keuangan Republik Indonesiaabdiel welmavenBelum ada peringkat

- Masa Berlaku: 30 Desember 2021: Mata Uang Grafik Kurs Beli Kurs Tengah Kurs JualDokumen2 halamanMasa Berlaku: 30 Desember 2021: Mata Uang Grafik Kurs Beli Kurs Tengah Kurs JualTirany Aprilia StephanieBelum ada peringkat

- SOP Pre Delivery InspectionDokumen7 halamanSOP Pre Delivery Inspectionabdiel welmaven100% (1)