Anda mungkin juga menyukai

- Modul AKL 5 Penyusunan Lap Keu Kons Tahun Setelah Akuisisi Sudah Penataan UlangDokumen19 halamanModul AKL 5 Penyusunan Lap Keu Kons Tahun Setelah Akuisisi Sudah Penataan UlangPutri Diva ApsariBelum ada peringkat

- Keseimbangan Pendapatan NasionalDokumen30 halamanKeseimbangan Pendapatan NasionalFitrah nurul auliaBelum ada peringkat

- Capital BudgetingDokumen50 halamanCapital Budgetingneneng yosanaBelum ada peringkat

- Aktiva Tetap Tidak BerwujudDokumen2 halamanAktiva Tetap Tidak Berwujudnova anita sekarwatiBelum ada peringkat

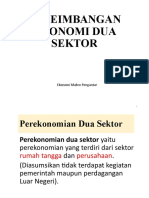

- Keseimbangan Ekonomi 2 SektorDokumen19 halamanKeseimbangan Ekonomi 2 Sektorferiz danisyaBelum ada peringkat

- Contoh Soal Cash FlowDokumen3 halamanContoh Soal Cash FlowHeaven NamjoonBelum ada peringkat

- Business Plan. M.E GRP - Final Indon TranslationDokumen18 halamanBusiness Plan. M.E GRP - Final Indon Translationksbsi nttBelum ada peringkat

- Soal Baldwin, Modern Financial ManagementDokumen6 halamanSoal Baldwin, Modern Financial ManagementEndah DipoyantiBelum ada peringkat

- 9 Investasi Dan Kriteria InvestasiDokumen18 halaman9 Investasi Dan Kriteria InvestasipolindianBelum ada peringkat

- Modul Pertemuan 10 - Intercompany Profit Transaction - Plant Asset (Upstream)Dokumen9 halamanModul Pertemuan 10 - Intercompany Profit Transaction - Plant Asset (Upstream)Muhammad IlhamBelum ada peringkat

- Ekotek 3 (NPV)Dokumen18 halamanEkotek 3 (NPV)skaca7242Belum ada peringkat

- Lampiran PMK 93Dokumen3 halamanLampiran PMK 93Pandu MahardhikaBelum ada peringkat

- Kewirausahaan Resume Bab 10-11Dokumen12 halamanKewirausahaan Resume Bab 10-11vicapriyantoBelum ada peringkat

- Jawaban Ujian PPH Badan - Fauzan AkbarDokumen20 halamanJawaban Ujian PPH Badan - Fauzan AkbarFauzan AkbarBelum ada peringkat

- Post Test 9 Asistensi Grup C Materi "Segmen"Dokumen19 halamanPost Test 9 Asistensi Grup C Materi "Segmen"alvin doang098Belum ada peringkat

- Analisa KeputusanDokumen14 halamanAnalisa KeputusanBayan DzuqiBelum ada peringkat

- Soal UAS Genap 2020-2021 Teori PortofolioDokumen5 halamanSoal UAS Genap 2020-2021 Teori Portofolioagusni prayogaBelum ada peringkat

- Maria Dewi DerosariDokumen5 halamanMaria Dewi Derosariyohand egheBelum ada peringkat

- 3 - Teori InvestasiDokumen31 halaman3 - Teori InvestasiYoana KartikaBelum ada peringkat

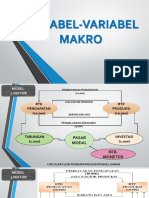

- Variabel MakroDokumen32 halamanVariabel MakroRusnawati Nur AminahBelum ada peringkat

- PPT8 Keseimbangan - Ekonomi - 2 - SektorDokumen22 halamanPPT8 Keseimbangan - Ekonomi - 2 - SektorAlvina28 YantiBelum ada peringkat

- Kharisma Nanda PP - Akm Aset TetapDokumen11 halamanKharisma Nanda PP - Akm Aset TetapKharisma NandaBelum ada peringkat

- Penurunan Nilai AssetDokumen19 halamanPenurunan Nilai AssetWarnoyo AhmadBelum ada peringkat

- Naskah EKSI4311 The 1Dokumen4 halamanNaskah EKSI4311 The 1mahmudah ning sugestiBelum ada peringkat

- Keseimbangan Ekonomi 2 SektorDokumen28 halamanKeseimbangan Ekonomi 2 Sektormuhammad alfariziBelum ada peringkat

- Tugas 6 Aikb Maya Gustina C1a019083Dokumen16 halamanTugas 6 Aikb Maya Gustina C1a019083Maya GustinaBelum ada peringkat

- Akl Bab 3Dokumen6 halamanAkl Bab 3Nila Novita WardaniBelum ada peringkat

- Bab 9 (OBLIGASI DOWNSTREAM)Dokumen3 halamanBab 9 (OBLIGASI DOWNSTREAM)tati rohaetiBelum ada peringkat

- PETA - KLP 4Dokumen157 halamanPETA - KLP 4AdiBelum ada peringkat

- Pertemuan Gabungan PN Dan Peran PemerintahDokumen24 halamanPertemuan Gabungan PN Dan Peran Pemerintahdani habibiBelum ada peringkat

- Tugas BCR - Ridhwan Abdul Wahid - 21010117140085Dokumen9 halamanTugas BCR - Ridhwan Abdul Wahid - 21010117140085Ridhwan Abdul WahidBelum ada peringkat

- 19feb22 - Literasi Keuangan - NUDokumen57 halaman19feb22 - Literasi Keuangan - NUwulanBelum ada peringkat

- Akl 2Dokumen4 halamanAkl 2m habiburrahman55Belum ada peringkat

- Isu - Isu Lain Dalam Pelaporan KonsolidasiDokumen50 halamanIsu - Isu Lain Dalam Pelaporan KonsolidasiArnoldus ApriyanoBelum ada peringkat

- Keseimbangan Ekonomi 2 SektorDokumen23 halamanKeseimbangan Ekonomi 2 SektorDimas WahyuBelum ada peringkat

- Tugas 4Dokumen7 halamanTugas 4khairaameraaBelum ada peringkat

- Pertemuan 4 InvestasiDokumen29 halamanPertemuan 4 InvestasiRadiah AriyaniBelum ada peringkat

- Laporan Keuangan DPLK Per 31 Desember 2022 67Dokumen1 halamanLaporan Keuangan DPLK Per 31 Desember 2022 67agusatun9028Belum ada peringkat

- Modul - 14Dokumen8 halamanModul - 14Anonymous 4Kj9uk6xQBelum ada peringkat

- Keseimbangan Ekonomi 2 SektorZAFDokumen28 halamanKeseimbangan Ekonomi 2 SektorZAFHikmah azizah NBelum ada peringkat

- Tugas 3 - M.Wyth - 041382017 - TAPDokumen8 halamanTugas 3 - M.Wyth - 041382017 - TAPmaddenwyth75% (4)

- Soal Latihan PPH Badan Sabtu MingguDokumen5 halamanSoal Latihan PPH Badan Sabtu MingguNova DiaBelum ada peringkat

- Bedah Soal Des2022Dokumen17 halamanBedah Soal Des2022Luluk Giras UmugaidaBelum ada peringkat

- PDF Kriteria Investasi - Compress 1Dokumen5 halamanPDF Kriteria Investasi - Compress 1fariz furrahmanBelum ada peringkat

- Kasus Iklan Andalan PDFDokumen4 halamanKasus Iklan Andalan PDFSaviraBelum ada peringkat

- Format Laporan KeuanganDokumen10 halamanFormat Laporan KeuanganfajarBelum ada peringkat

- Latihan Audit Kas 6A1 - Alya A.RDokumen13 halamanLatihan Audit Kas 6A1 - Alya A.RAlya RoufBelum ada peringkat

- Contoh Rapb Bumdes 2021Dokumen11 halamanContoh Rapb Bumdes 2021Bucik ErnaBelum ada peringkat

- Analisis Titik Impas Usaha Planet SportsDokumen8 halamanAnalisis Titik Impas Usaha Planet SportsNugrahainimahardikaBelum ada peringkat

- TUGAS MAKRO REG 301 - Wahyu Gabe Mulia SianturiDokumen5 halamanTUGAS MAKRO REG 301 - Wahyu Gabe Mulia SianturiWahyuBelum ada peringkat

- Bahan Paparan DJP MakassarDokumen35 halamanBahan Paparan DJP MakassarArjunansyah LakidendeBelum ada peringkat

- Uas - M1Dokumen4 halamanUas - M1vinkaBelum ada peringkat

- Soal Syie TaiDokumen9 halamanSoal Syie TaiDillahBelum ada peringkat

- Akuntansi Keuangan Menengah Arus KasDokumen9 halamanAkuntansi Keuangan Menengah Arus Kas30Zahrotul Devi AmaliaBelum ada peringkat

- Akuntansi Kelompok 5Dokumen24 halamanAkuntansi Kelompok 5Difa A.ZBelum ada peringkat

- TUGAS 11 - B200180283 - Syuhada Dwi Setiaji - KELAS FDokumen3 halamanTUGAS 11 - B200180283 - Syuhada Dwi Setiaji - KELAS Fsyuhada ajiBelum ada peringkat

- 01 PPH Op 20222Dokumen6 halaman01 PPH Op 20222ApryllyBelum ada peringkat