Anda mungkin juga menyukai

- MNCN - Laporan Informasi Dan Fakta Material - 31285159 - Lamp2 PDFDokumen5 halamanMNCN - Laporan Informasi Dan Fakta Material - 31285159 - Lamp2 PDFlegivethBelum ada peringkat

- AT Company UpdateDokumen5 halamanAT Company UpdatePrayogi KramyBelum ada peringkat

- IDN - Financial - BBNI - 2Q23 - In-Line, Better 2H23 OutlookDokumen3 halamanIDN - Financial - BBNI - 2Q23 - In-Line, Better 2H23 OutlookBilclinton SaragihBelum ada peringkat

- NHKSI FinalDokumen4 halamanNHKSI FinalMade JayaBelum ada peringkat

- 363e67f9-7f5d-4acb-a4f7-ed10b331a9c0Dokumen12 halaman363e67f9-7f5d-4acb-a4f7-ed10b331a9c0Toni SaputroBelum ada peringkat

- Company Flash Update - INDY, SCMA, SMRA, RAJADokumen6 halamanCompany Flash Update - INDY, SCMA, SMRA, RAJAOnggo iMamBelum ada peringkat

- Kajian Asuransi Kredit Consumer - White Paper 27012021Dokumen77 halamanKajian Asuransi Kredit Consumer - White Paper 27012021Dede AndriBelum ada peringkat

- GOTO - MNCS Retail Flashnote - 17032023Dokumen2 halamanGOTO - MNCS Retail Flashnote - 17032023mirzasahputraBelum ada peringkat

- Yurika Fadilla R - 142200178 - UAS ALKDokumen82 halamanYurika Fadilla R - 142200178 - UAS ALKyurika ramadhaniBelum ada peringkat

- Dana Pendapatan Tetap KorporasiDokumen1 halamanDana Pendapatan Tetap KorporasiLydia IndahBelum ada peringkat

- Grup GoTo Terus Tumbuh Pada Kinerja Kuartal III 2023Dokumen12 halamanGrup GoTo Terus Tumbuh Pada Kinerja Kuartal III 2023Chandra ChandraBelum ada peringkat

- Isat 2022Dokumen5 halamanIsat 2022kezia yulinaBelum ada peringkat

- Analisis Informasi Keuangan PT Indosat Dan Indonesia Prima TBKDokumen43 halamanAnalisis Informasi Keuangan PT Indosat Dan Indonesia Prima TBK220Dias Ivoni DwijayantiBelum ada peringkat

- Uts Bank Dan Lembaga KeuanganDokumen5 halamanUts Bank Dan Lembaga KeuanganQotrun NadaBelum ada peringkat

- Sektor TeknologiDokumen44 halamanSektor TeknologiErwin HermawanBelum ada peringkat

- Annual Report PT Bank UOB Indonesia 2022 BahasaDokumen507 halamanAnnual Report PT Bank UOB Indonesia 2022 BahasaLeviathanBelum ada peringkat

- Bagas Investasi Syariah-1Dokumen9 halamanBagas Investasi Syariah-1Bagas JBelum ada peringkat

- 293 575 1 SMDokumen11 halaman293 575 1 SMTrivena LosungBelum ada peringkat

- Info Memo 1Q18 Ind Final PDFDokumen8 halamanInfo Memo 1Q18 Ind Final PDFHaniefBelum ada peringkat

- Cashlez FY20 Results Mencapai Pertumbuhan Kinerja Yang Kuat 050421Dokumen7 halamanCashlez FY20 Results Mencapai Pertumbuhan Kinerja Yang Kuat 050421DMT IPOBelum ada peringkat

- SKRIPSI - RISNAWATI - 17101155310555 - BAB I.pdf - CrdownloadDokumen15 halamanSKRIPSI - RISNAWATI - 17101155310555 - BAB I.pdf - CrdownloadMuhammad ZidanFEBBelum ada peringkat

- Fundamental Analysis - Kotambunan, TesalonikaDokumen3 halamanFundamental Analysis - Kotambunan, TesalonikaTesalonika KotambunanBelum ada peringkat

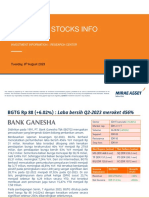

- Small Cap Stocks Info - 8 August 2023Dokumen5 halamanSmall Cap Stocks Info - 8 August 2023nopaBelum ada peringkat

- UTS Manajemen Perbankan Kel 4 - Bank BTN AzharrDokumen4 halamanUTS Manajemen Perbankan Kel 4 - Bank BTN AzharrFaaaadhBelum ada peringkat

- TO CA - Manajemen Keuangan Lanjutan Essay KasusDokumen3 halamanTO CA - Manajemen Keuangan Lanjutan Essay KasusDestia PentianaBelum ada peringkat

- Bab 4 TADokumen15 halamanBab 4 TAnadiadinianggrainiBelum ada peringkat

- Elin Waty - AAJIDokumen11 halamanElin Waty - AAJIWelin KusumaBelum ada peringkat

- Tugas Keuangan SukmawatiDokumen5 halamanTugas Keuangan SukmawatiLevin LombanBelum ada peringkat

- Tugas Uas Pasar ModalDokumen13 halamanTugas Uas Pasar ModalAngga Dwi PutraBelum ada peringkat

- Analisis Keuangan Kelompok 2Dokumen40 halamanAnalisis Keuangan Kelompok 2anna theresiaBelum ada peringkat

- ANALISIS KEUANGAN (Fix)Dokumen40 halamanANALISIS KEUANGAN (Fix)anna theresiaBelum ada peringkat

- PDF Manajemen StrategiDokumen55 halamanPDF Manajemen StrategiMochamad Jihan fikriBelum ada peringkat

- Tugas Uas Pasar ModalDokumen14 halamanTugas Uas Pasar ModalAngga Dwi PutraBelum ada peringkat

- Laporan Keuangan Astra Tahun 2021Dokumen7 halamanLaporan Keuangan Astra Tahun 2021SendriFebriyansyahBelum ada peringkat

- Analisi Laporan Keuanagan Time Series Terhadap Saham PTDokumen6 halamanAnalisi Laporan Keuanagan Time Series Terhadap Saham PTTrhee’ ChanelsBelum ada peringkat

- Tugas MNJ Keuangan Densi 24Dokumen14 halamanTugas MNJ Keuangan Densi 24Rio BenjaBelum ada peringkat

- Small Cap Stocks Info - 9 February 2023Dokumen5 halamanSmall Cap Stocks Info - 9 February 2023minnie storeBelum ada peringkat

- UTS Manajemen Perbankan Kel 4 - Bank BTN Kurang GiliDokumen3 halamanUTS Manajemen Perbankan Kel 4 - Bank BTN Kurang GiliFaaaadhBelum ada peringkat

- MNC Dana Syariah FactsheetDokumen1 halamanMNC Dana Syariah FactsheetVincent TjoeBelum ada peringkat

- Info Memo 1H18 Ind FinalDokumen9 halamanInfo Memo 1H18 Ind FinalHaniefBelum ada peringkat

- Analisis Rasio SolvabilitasDokumen8 halamanAnalisis Rasio Solvabilitasjosephine elviraBelum ada peringkat

- Praktik Treding SahamDokumen11 halamanPraktik Treding SahamChisa AgustynBelum ada peringkat

- Analisis Bisnis - Kelompok 3 - Kelas DDokumen8 halamanAnalisis Bisnis - Kelompok 3 - Kelas DAbi PascalBelum ada peringkat

- EP 22 - Hilman Dwi Saputro - 5C - TugasMandiri1Dokumen6 halamanEP 22 - Hilman Dwi Saputro - 5C - TugasMandiri1hilman dwiiBelum ada peringkat

- Proposal New RimaDokumen36 halamanProposal New RimaRima MelatiBelum ada peringkat

- 6251 6261Dokumen11 halaman6251 6261Abah JufriBelum ada peringkat

- Edgar Rekitana 2261141-Analisis-Laporan-Keuangan-Keuangan-Pt-Cisarua-Mountain-Dairy-TbkDokumen13 halamanEdgar Rekitana 2261141-Analisis-Laporan-Keuangan-Keuangan-Pt-Cisarua-Mountain-Dairy-TbkEdgar RekitanaBelum ada peringkat

- Analisis Laporan Keuangan MomonDokumen8 halamanAnalisis Laporan Keuangan MomonAhwal Syakhsiyyah 20Belum ada peringkat

- Icon SR-2016 PDFDokumen186 halamanIcon SR-2016 PDFbagas tiansyahBelum ada peringkat

- Pembahas ApindoDokumen14 halamanPembahas ApindoCarlos MangunsongBelum ada peringkat

- Bab 4 (Asep) Update N AccDokumen23 halamanBab 4 (Asep) Update N AccAlberson ManurungBelum ada peringkat

- Bab IvDokumen22 halamanBab IvSallimahikaputri MalauBelum ada peringkat

- Pendahuluan 8Dokumen8 halamanPendahuluan 8Andi Fahriza33Belum ada peringkat

- Bni SR 2013 TH PDFDokumen88 halamanBni SR 2013 TH PDFRiko Susetia YudaBelum ada peringkat

- Small Cap Stocks Info - 25 October 2022Dokumen5 halamanSmall Cap Stocks Info - 25 October 2022mario heskiaBelum ada peringkat

- Report BBRI1Dokumen5 halamanReport BBRI1vr beautysBelum ada peringkat

- Investor Newsletter 9M22 IDfDokumen8 halamanInvestor Newsletter 9M22 IDfDevina Ratna DewiBelum ada peringkat

- Unboxing Sektor Tech Update PDFDokumen44 halamanUnboxing Sektor Tech Update PDFMuhammad Niqobul LubabBelum ada peringkat

- Panduan Iklan Berbayar Modern untuk Pemilik Bisnis: Pengantar Cepat ke Iklan Google, Facebook, Instagram, YouTube, dan TikTokDari EverandPanduan Iklan Berbayar Modern untuk Pemilik Bisnis: Pengantar Cepat ke Iklan Google, Facebook, Instagram, YouTube, dan TikTokBelum ada peringkat