Anda mungkin juga menyukai

- Neraca Pempek DoommDokumen39 halamanNeraca Pempek Doommira deriantyBelum ada peringkat

- Bab 08Dokumen59 halamanBab 08salman aryanaBelum ada peringkat

- (Template) Tugas Praktikum Pertemuan 9Dokumen4 halaman(Template) Tugas Praktikum Pertemuan 9Eny Markgrasilita Situmorang50% (2)

- Flowchart Penjualan Tunai PT Maharani PDFDokumen3 halamanFlowchart Penjualan Tunai PT Maharani PDFIchsan ArifinBelum ada peringkat

- Kasus I Perusahaan JasaDokumen6 halamanKasus I Perusahaan JasaIis IndardaBelum ada peringkat

- AKMENDokumen2 halamanAKMENAzzah Nur IstiqomahBelum ada peringkat

- Bab 3 Penentuan Biaya PesananDokumen20 halamanBab 3 Penentuan Biaya PesananMella HandayaniBelum ada peringkat

- Latihan Soal EkuitasDokumen2 halamanLatihan Soal EkuitasSeptia DewiyaniBelum ada peringkat

- Form Tugas Akhir - Myob Fix DianismawDokumen13 halamanForm Tugas Akhir - Myob Fix DianismawManchunian100% (1)

- Kelompok 1 PajakDokumen17 halamanKelompok 1 PajakAnnisa Septia HarahapBelum ada peringkat

- Contoh Soal Salon AyuDokumen2 halamanContoh Soal Salon Ayufajar100% (1)

- Analisis Penilaian Persediaan Mengggunakan Metode TaksiranDokumen28 halamanAnalisis Penilaian Persediaan Mengggunakan Metode Taksirandony lenggaBelum ada peringkat

- Akuntansi Biaya Kelompok 3Dokumen32 halamanAkuntansi Biaya Kelompok 3Khrisna AnggunBelum ada peringkat

- Sia m5 Konsep File, Database, Persyaratan Dasar Dari Sistem Basis Data RelasionalDokumen15 halamanSia m5 Konsep File, Database, Persyaratan Dasar Dari Sistem Basis Data RelasionalAlif RonanBelum ada peringkat

- Materi 8 Process Costing Lanjutan PDFDokumen8 halamanMateri 8 Process Costing Lanjutan PDFakmalBelum ada peringkat

- PIUTANG RikisDokumen47 halamanPIUTANG Rikismayesti puspaBelum ada peringkat

- AKM 2 Bab-15-Ak3-Ekuitas-Edisi-IfrsDokumen60 halamanAKM 2 Bab-15-Ak3-Ekuitas-Edisi-Ifrsdina maryanaBelum ada peringkat

- Bagan Alir Dokumen Prosedur Pencatatan Beban Overhead Pabrik SengguhnyaDokumen9 halamanBagan Alir Dokumen Prosedur Pencatatan Beban Overhead Pabrik SengguhnyaIvanda Kumala SariBelum ada peringkat

- Ringkasan Bab 7Dokumen9 halamanRingkasan Bab 7Riyanda EfritaniaBelum ada peringkat

- SOAL LATIHAN 1 Siklus Perusahaan Jasa 2015Dokumen2 halamanSOAL LATIHAN 1 Siklus Perusahaan Jasa 2015Retno KumalasariBelum ada peringkat

- Bab 06 - Akuntansi Untuk Perusahaan DagangDokumen82 halamanBab 06 - Akuntansi Untuk Perusahaan DagangCaigi 0107Belum ada peringkat

- Soal Latihan Perusahaan ManufakturDokumen23 halamanSoal Latihan Perusahaan ManufakturAnnisa RanatsabitahBelum ada peringkat

- KonsinyasiDokumen6 halamanKonsinyasiOktaBelum ada peringkat

- SOAL Akuntansi ManufakturDokumen6 halamanSOAL Akuntansi ManufakturM Rafi PriyambudiBelum ada peringkat

- I Kadek Angga Ardiantna - 2017051124Dokumen8 halamanI Kadek Angga Ardiantna - 2017051124OrionBelum ada peringkat

- 3-PA Ak Perusahaan ManufakturDokumen13 halaman3-PA Ak Perusahaan ManufakturRobertoSymBelum ada peringkat

- Soal Dan Jawaban Bab 2 Sistem Informasi AkuntansiDokumen2 halamanSoal Dan Jawaban Bab 2 Sistem Informasi Akuntansilinda kusuma50% (2)

- Tugas Kelompok 1 w3 s4 Team 5 DmeaDokumen9 halamanTugas Kelompok 1 w3 s4 Team 5 Dmearahmat achmadiBelum ada peringkat

- SOAL LATIHAN DAN TUGAS AK2 Pertemuan 1 Liabilitas Jangka PendekDokumen7 halamanSOAL LATIHAN DAN TUGAS AK2 Pertemuan 1 Liabilitas Jangka PendekDila HajikuBelum ada peringkat

- Latihan 2Dokumen2 halamanLatihan 2Novra Yu Nanda100% (1)

- Persediaan Non Cost MhsDokumen29 halamanPersediaan Non Cost MhsAnonymous f6E30BDBelum ada peringkat

- Proses Costing Bab 17Dokumen9 halamanProses Costing Bab 17Rika KartikaBelum ada peringkat

- Depreciation, Impairments, DepletionDokumen31 halamanDepreciation, Impairments, DepletionirsaBelum ada peringkat

- Biaya Tenaga Kerja 4Dokumen18 halamanBiaya Tenaga Kerja 4ꓰꓡꓡꓰꓠ. ꓓꓖꓰꓠꓰꓣꓰꓢꓢ'Belum ada peringkat

- 11 KonsinyasiDokumen29 halaman11 KonsinyasiChristy PranawatyBelum ada peringkat

- Siklus-Akuntansi DIKTAT (DAGANG)Dokumen120 halamanSiklus-Akuntansi DIKTAT (DAGANG)SUPRIANDI NYENGKABelum ada peringkat

- SOAL UAS Manajemen Keuangan Desember 2021Dokumen4 halamanSOAL UAS Manajemen Keuangan Desember 2021eja asBelum ada peringkat

- Jawaban Essay Latihan SoalDokumen2 halamanJawaban Essay Latihan SoalHendriMaulanaBelum ada peringkat

- D3 Akuntansi A-25 - 25 Mei 2020Dokumen21 halamanD3 Akuntansi A-25 - 25 Mei 2020Faiz PrajaBelum ada peringkat

- Akbi - S1 - A2 - 4 - PT IndopaintDokumen5 halamanAkbi - S1 - A2 - 4 - PT IndopaintYang LeksBelum ada peringkat

- Rekapitulasi Kasus Praktik Akuntansi BiayaDokumen32 halamanRekapitulasi Kasus Praktik Akuntansi BiayaRiris AndrianiBelum ada peringkat

- Modul 9Dokumen3 halamanModul 9Dwi Cahyo AbimanyuBelum ada peringkat

- Soal RekonsiliasiDokumen4 halamanSoal RekonsiliasiRomaida SitumorangBelum ada peringkat

- Whitni CorporationDokumen1 halamanWhitni CorporationQueen0% (1)

- Soal Arus KasDokumen5 halamanSoal Arus Kaszainal rusdiBelum ada peringkat

- AK2 Pertemuan 8 Laporan Arus KasDokumen61 halamanAK2 Pertemuan 8 Laporan Arus KasWinda Fitria NtuBelum ada peringkat

- PT Adi JayaDokumen25 halamanPT Adi JayaAnisaBelum ada peringkat

- Tugas 1 Sistem Informasi AkuntansiDokumen6 halamanTugas 1 Sistem Informasi Akuntansiiit gusti sri murniBelum ada peringkat

- Jawaban Jurnal HPPDokumen5 halamanJawaban Jurnal HPPAdib MurfidBelum ada peringkat

- Resume HPP LanjutanDokumen4 halamanResume HPP LanjutanEssa PuspitaBelum ada peringkat

- Investasi Jangka Pendek (Sementara)Dokumen8 halamanInvestasi Jangka Pendek (Sementara)Anggraini Novitawati100% (1)

- Tugas 1 (Gambaran Umum Akuntansi Biaya, Unsur-Unsur Harga Pokok Produksi Dan Biaya Bahan)Dokumen2 halamanTugas 1 (Gambaran Umum Akuntansi Biaya, Unsur-Unsur Harga Pokok Produksi Dan Biaya Bahan)R. Fauziah AnitaBelum ada peringkat

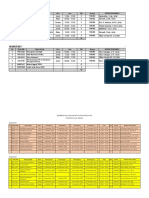

- Kelompok 5 - Pengumpulan Biaya Berdasarkan Process Costing (WACM & FIFO)Dokumen21 halamanKelompok 5 - Pengumpulan Biaya Berdasarkan Process Costing (WACM & FIFO)straightkijBelum ada peringkat

- Anggaran Salad HAHAIN FixDokumen4 halamanAnggaran Salad HAHAIN FixNanda RatnaBelum ada peringkat

- Sistem Akuntansi Perusahaan Jasa 2Dokumen63 halamanSistem Akuntansi Perusahaan Jasa 2Ade FatmawatiSE.,MPdBelum ada peringkat

- Soal FOTO COPY SINTA. MYOBDokumen12 halamanSoal FOTO COPY SINTA. MYOBmuhammad widodoBelum ada peringkat

- Akuntansi Aset TetapDokumen8 halamanAkuntansi Aset TetapTita AndrianiBelum ada peringkat

- Project Process Costing Umkm "Ten-Z" Chips: Untuk Memenuhi Tugas Matakuliah Akuntansi BiayaDokumen4 halamanProject Process Costing Umkm "Ten-Z" Chips: Untuk Memenuhi Tugas Matakuliah Akuntansi Biayamuhammad yodhya suwasonoBelum ada peringkat

- Chapter 5 Kieso Terjemahan PPTDokumen59 halamanChapter 5 Kieso Terjemahan PPTZulfa PuspitaBelum ada peringkat

- Chapter 5 Kieso TerjemahanDokumen59 halamanChapter 5 Kieso TerjemahanAhmad Maulana Yusuf100% (1)

- Handout SIM KI 2021Dokumen127 halamanHandout SIM KI 2021Asih SetyaningsihBelum ada peringkat

- Pertemuan 1Dokumen13 halamanPertemuan 1Asih SetyaningsihBelum ada peringkat

- Tugas 3Dokumen1 halamanTugas 3Asih SetyaningsihBelum ada peringkat

- Handout SIM KI 2021Dokumen127 halamanHandout SIM KI 2021Asih SetyaningsihBelum ada peringkat

- Bab 1 - Pelaporan Keuangan Dan Standar Akuntansi - MartaniDokumen30 halamanBab 1 - Pelaporan Keuangan Dan Standar Akuntansi - MartaniAsih SetyaningsihBelum ada peringkat

- Konsolidasi Pada Anak Perusahaan Yang Dimiliki Kurang Dari Kepemilikan PenuhDokumen27 halamanKonsolidasi Pada Anak Perusahaan Yang Dimiliki Kurang Dari Kepemilikan Penuhbaiq atinBelum ada peringkat

- HUKUM BISNIS PPTDokumen260 halamanHUKUM BISNIS PPTPembisnisBelum ada peringkat

- AKM Hal 62-73-1Dokumen12 halamanAKM Hal 62-73-1Asih SetyaningsihBelum ada peringkat

- Distribusi Mata Kuliah Akuntansi 2020Dokumen2 halamanDistribusi Mata Kuliah Akuntansi 2020Asih SetyaningsihBelum ada peringkat

- Akuntansi Biaya Bahan BakuDokumen10 halamanAkuntansi Biaya Bahan BakuAsih SetyaningsihBelum ada peringkat

- (3 Inflasi Pengangguran Pertumbuhan Ekonomi) Ekonomi MakroDokumen17 halaman(3 Inflasi Pengangguran Pertumbuhan Ekonomi) Ekonomi MakroAsih SetyaningsihBelum ada peringkat

- (2 Pendapatan Nasional) Ekonomi MakroDokumen26 halaman(2 Pendapatan Nasional) Ekonomi MakroAsih SetyaningsihBelum ada peringkat

- STATISTIKA (Konsep Dasar Statistika)Dokumen60 halamanSTATISTIKA (Konsep Dasar Statistika)Asih SetyaningsihBelum ada peringkat

- AKM Hal 62-73-1Dokumen12 halamanAKM Hal 62-73-1Asih SetyaningsihBelum ada peringkat

- (1 Pendahuluan) Ekonomi MakroDokumen26 halaman(1 Pendahuluan) Ekonomi MakroAsih StyaningBelum ada peringkat

- (2 Pendapatan Nasional) Ekonomi MakroDokumen26 halaman(2 Pendapatan Nasional) Ekonomi MakroAsih SetyaningsihBelum ada peringkat

- HUKUM BISNIS PPTDokumen260 halamanHUKUM BISNIS PPTPembisnisBelum ada peringkat

- ACFrOgBqejkZLiRof7Ax79I2uAf5ebX6GB71LlBjTjIGq549079hmIlyhplM6OWqpTW8gaaQyMB5Smq5M7GLorr7aaTEASwmPG3kEkfmifRCt5AK9kfNmI 4tNX9RssXSIBgqbMfUaH1yxDZX4l5Dokumen1 halamanACFrOgBqejkZLiRof7Ax79I2uAf5ebX6GB71LlBjTjIGq549079hmIlyhplM6OWqpTW8gaaQyMB5Smq5M7GLorr7aaTEASwmPG3kEkfmifRCt5AK9kfNmI 4tNX9RssXSIBgqbMfUaH1yxDZX4l5Asih SetyaningsihBelum ada peringkat

- STATISTIKA (Konsep Dasar Statistika)Dokumen60 halamanSTATISTIKA (Konsep Dasar Statistika)Asih SetyaningsihBelum ada peringkat

- Geostrategi-Indonesia 13Dokumen23 halamanGeostrategi-Indonesia 13Asih SetyaningsihBelum ada peringkat

- SPT PPH Pasal 21Dokumen64 halamanSPT PPH Pasal 21Asih SetyaningsihBelum ada peringkat

- (3 Inflasi Pengangguran Pertumbuhan Ekonomi) Ekonomi MakroDokumen17 halaman(3 Inflasi Pengangguran Pertumbuhan Ekonomi) Ekonomi MakroAsih SetyaningsihBelum ada peringkat

- Pendidikan Agama Islam IiDokumen1 halamanPendidikan Agama Islam IiAsih SetyaningsihBelum ada peringkat

- Tugas JurnalDokumen1 halamanTugas JurnalAsih SetyaningsihBelum ada peringkat

- Geostrategi-Indonesia 13Dokumen23 halamanGeostrategi-Indonesia 13Asih SetyaningsihBelum ada peringkat

- STATISTIKA (Konsep Dasar Statistika)Dokumen60 halamanSTATISTIKA (Konsep Dasar Statistika)Asih SetyaningsihBelum ada peringkat

- Roundown AcaraDokumen1 halamanRoundown AcaraAsih SetyaningsihBelum ada peringkat

- 5 OKT 2020 RUU Cipta Kerja - ParipurnaDokumen905 halaman5 OKT 2020 RUU Cipta Kerja - ParipurnaJabbar Ramdhani85% (13)

- Aspek Hukum Dalam Bisnis REGULER-dikonversiDokumen2 halamanAspek Hukum Dalam Bisnis REGULER-dikonversiAsih SetyaningsihBelum ada peringkat